![]()

Chapter 1

Corporate Valuation

In essence, there are three generally accepted methods of valuation: the discounted cash flow approach, the market approach, and the net asset approach. This book deals with the market approach. However, a common misconception is that these three concepts represent three fundamentally disparate or independent methodologies that, applied to the same subject of interest by the same analyst under the same valuation purpose, should or may generate three fundamentally different outcomes. This is not the case. Carried out correctly, a business valuation (under an assumption of continued pursuit of activities, i.e. under a going concern assumption), given a single well-defined subject and valuation purpose, shall in theory as well as in practice produce exactly the same output (i.e. value) irrespective of the model(s) utilized. To put it another way, company value is driven by company fundamentals, not by the choice of valuation model(s).

From a strictly theoretical perspective, the value of a company (or any other cash flow generating asset for that matter) will equal its projected future returns discounted to a present value by a risk-adjusted rate of return. This relationship will hold regardless of the methodology or methodologies used to derive that value. Hence the three methodologies presented above express exactly the same thing, but in three totally different ways. In order to fully appreciate the concept and structure of the market approach it is vital to recognize the fundamentals of the other two methodologies in isolation as well as in conjunction with each other. Set out below is a brief introduction to these three methodologies.

1.1 THE DISCOUNTED CASH FLOW APPROACH

The discounted cash flow approach (DCF) aims to establish the net present value of a cash flow generating asset (e.g. a company) by discounting its future expected returns with an appropriate required rate of return.

Performing business valuations, the cash flow which forms the basis of the net present value calculation is usually the “free cash flow to firm” (FCFF), explicitly the expected cash flow of the business independent of its financing (i.e. cash flow accruing to the company’s shareholders and lenders). Consequently, the cash flow in question should not be affected by such things as interest or dividends; however, it will be burdened by tax. Hence, the discount rate must reflect a weighted cost of capital for debt and equity financing after tax. A discounting (i.e. a net present value calculation) of the expected cash flow at the appropriate weighted average cost of capital will give the value of the business enterprise (i.e. the market value of operating capital or, alternatively, the market value of invested capital).

To obtain the value of the shares, i.e. the value of the equity, the business enterprise value needs to be adjusted by the net debt position at the valuation date, i.e. subtracting financial liabilities, and including excess cash and non-operating assets.

It is also possible to compute the equity value, i.e. the market value of all shares, via a direct approach, that is, by projecting future cash flow specifically attributable to the shareholders of the company, free cash flow to equity (FCFE). Such cash flow has already been charged with financial items (interest and suchlike) and should accordingly be discounted by a matching rate of return (specifically a required return on equity). Hence, discounting this cash flow at the appropriate capital cost of equity therefore gives the equity value directly.

1.2 THE MARKET APPROACH

The market approach aims to derive the value of a company based on how similar firms are priced on the stock exchange or through company transactions.

Using the market approach, price-related indicators such as price in relation to sales, earnings, number of employees, etc. are utilized. Consequently, the pricing of the valuation subject will implicitly be dependent upon other actors’ assessment of future growth potential, profitability, risk profile (cost of capital), etc. for the valuation subject in question, which may or may not be appropriate.

The task is therefore to find comparables with as similar a structure and operations as possible to the company in question. Differences between the comparator group of companies and the valuation subject at issue as regards the size and nature of their operations, among other things, will justify correspondingly different levels of business risk, growth potential, margins, etc. These differences must therefore be considered when justifying different levels of value, i.e. when justifying the relevant or appropriate value multiple to be applied to the subject company.

1.3 THE NET ASSET APPROACH

The net asset approach implies an adjustment of the balance sheet with regard to the market value of assets and liabilities. The net asset approach is often cited as an independent valuation method, but given an assumption of ongoing business operations, i.e. a going concern assumption, a proper implementation will, in order to properly capture the value of the subject company’s intangible assets, and synergies among assets, normally require the use of several DCF calculations. Consequently, fully executed, the concluding value derived from the net asset approach under a going concern assumption will, to the dollar, match that derived by the DCF approach.

Often a simplified form of the net asset approach, where only book tangible and intangible assets and liabilities are adjusted to their market value equivalents, is applied. The net asset value thus calculated can then be used as a basis for comparison and reconciliation of the DCF value. The difference between the simplified net asset value above and the DCF value may then be deemed to represent the value of non-book intangible assets including goodwill.

![]()

Chapter 2

What Value?

A common misconception is that, in the world of business valuation, only one single universal value exists. Unfortunately that is not the case. There is a whole variety of different types of values available as well as definitions of value. For this reason, before even working on any spreadsheets, it is very important to clearly define what value we are looking for and why.

2.1 STANDARD OF VALUES

As indicated above, there is a vast number of generally accepted standards of value. The most common when working with unlisted companies are:

- fair value1

- fair market value2

- investment value.

Fair value and fair market value may, in a broad context, be categorized under the umbrella term “market value.”

The market value aims to define or describe the subject interest from a “neutral” value perspective; in other words, the value shall reflect a well-informed financial investor’s point of view. This implies a value equivalent to a transfer of the shares, or the business enterprise entity should that be the case, in an open and unregulated market between a rational seller and a prudent buyer with no coercion and when both parties have access to equivalent and relevant information. The value remains free from any type of extra or additional synergistic values or premiums (strategy, economies of scale, acquisition of market shares, etc.) which are likely to benefit only one, or a certain group of, specific investor(s).

Investment value represents the value for an explicit investor and therefore includes premiums that can be realized by only one, or maybe a small class of, specific investor(s) through various types of synergy. The values of synergies hence make the difference between the estimated market value as defined above and the investment value.

The market approach, based on quotes derived from publicly traded shares, is particularly handy when making use of the fair value or the fair market value standard of value.

On the other hand, should the valuation be based on multiples derived from transactions (listed as well as unlisted companies) rather than publicly traded shares as above, one should be aware that these multiples may include a variety of premiums and discounts of different nature and size (see the “Transactions” section for information on the factors that can give rise to these premiums and discounts).

The actual price paid for acquired companies may thus be based on factors and synergies that only those specific purchasers were able to identify and/or assimilate. Consequently, financial investors, who cannot assimilate these kinds of synergies, cannot pay such premiums either. The value of the subject interest as derived from a transaction-related multiple may thus run the risk of reflecting the value of (i.e. the prevailing conditions for) that particular peer during that particular transaction rather than the more “neutral” market value set by a well-informed financial investor (in other words, the valuation subject will be given the investment value of that particular peer as acquired by that particular purchaser at that specific point in time rather than the market value as defined above).

On the flip side of the coin, value multiples derived from normal stock trading in public companies are accordingly not appropriate for the valuation of synergy-fueled acquisitions. As these investors may be able to realize synergies that financial investors cannot take advantage of, they may also have the opportunity to realize values that a financial investor cannot take advantage of.

Logically, then, should not multiples derived from company transactions be appropriate for value derivation when considering an acquisition or disposal of a majority stake (in which it can be considered to be scope for synergies)? Although multiples derived from transactions often involve the value of synergies, these are unlikely to be identical to that of your specific position/acquisition. Hence caution needs to be exercised when using value multiples derived from company transactions data (more on this later).

Consequently, if one wants a valuation from a specific investor’s point of view (i.e. a valuation including various kinds of synergies), a DCF approach is recommended instead. In this case, the DCF valuation can be tailored to the specific circumstances and conditions of the specific company or acquisition.

2.2 MARKETABILITY AND CONTROL

We move on to what is, within the framework of valuation, an extraordinarily complex issue that can have a significant impact in terms of value if handled incorrectly:

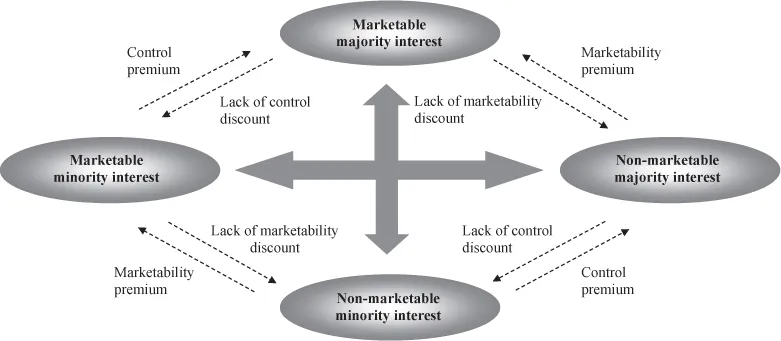

1. What level of marketability and ownership interest does the equity stake at issue embody? The identical share, in a given company, may hold different values depending on the ownership interest and level of marketability associated with just that particular share.

2. What adjustments are required to recalculate the resultant value, based on its present given ownership interest and marketability, to the level of ownership interest and marketability that one de facto wants it to represent?

2.2.1 Marketability (liquidity)

The value of an individual share, in the form of a minority interest stake, in a given unlisted company (i.e. a non-marketable minority interest) is lower than that of an equivalent single share of a publicly listed company (i.e. a marketable minority interest), all else being equal. This is because a minority stake in an unlisted company may be very difficult to divest – in many cases perhaps even unsaleable – as interest in the share among stakeholders other than the company’s current (often very limited) group of shareholders may be close to non-existent (i.e. there is no public market for the shares in question, and so the individual owner must himself find a buyer and negotiate an appropriate selling price for the share/equity stake in question). Equivalent listed shares can, on the other hand, normally be sold and transformed into cash more or less instantaneously (assuming, of course, that the shares in question trade fairly frequently).

2.2.2 Control

The lower value per share as indicated above applies only to a single share in the form of a non-marketable minority interest (i.e. a minority shareholding in an unlisted company) vis-à-vis an equivalent share in the form of a marketable minority interest (i.e. a minority shareholding in a listed company). The imaginary value of this individual unlisted share, in the form of a non-marketable minority interest, multiplied by the number of outstanding shares, does not, however, give the value of the company if you are that company’s sole proprietor (i.e. if you are sitting on a non-marketable majority interest).

Just as a rational investor is willing to pay more for a stock that is liquid, compared with a corresponding illiquid one, all else being equal, the same rational investor is willing to pay more for a stock that provides control vis-à-vis a corresponding one that does not, all else being equal. The right or option to influence the strategy, management policy, capital structure, salaries, and allowances of senior executives, dividend policy, listing policy, etc. of the company in question in general represents considerable value. This is evident if not in context with buy-out acquisitions where acquirers often pay a significant premium for the right of control.3 It is rare to find premiums being offered for listed minority interests (and should someone do that, it would most likely be a minority interest that, together with the bidder’s other possessions, would give rise to some form of controlling interest). Hence, the value of the one and the same type of share in a given unlisted company is therefore higher if it is part of a larger controlling stake as compared to that exact same share as part of a stake containing only one or a few shares.

In its most basic form there are four different combinations of ownership interest and marketability:

1. a marketable majority interest

2. a marketable minority interest

3. a non-marketable majority interest

4. a non-marketable minority interest.

The connection between these four positions is illustrated in Figure 2.1.

2.2.3 Adjusting for marketability and control

In addition to a strict classification of each position, in accordance with the description above, it is also important to emphasize that utilization of different valuation methods and models, and different assumptions regarding input data of these methods and models, can result in different characteristics in terms of ownership and marketability. This may in turn cause the exact same share to be assigned different values depending on no more than the choice of valuation methodology and/or input data. An analyst/appraiser under a well-defined assignment must therefore keep track of his or her actions when he or she derives the value of a company based on a mixture of methods and models.

That a 100 percent ownership of a company’s shares represents a majority or a controlling interest, and that a 1 percent ownership of a company’s shares represents a minority interest is, of course, obvious in the same way that an exchange-listed stock is more liquid than an equivalent unlisted one. However, should we face a situation in which adjustments would be considered necessary, i.e. if we are forced to adjust the given value(s) in order to move from a set to a desired...