![]()

Part I

The Deterministic Environment

![]()

1

Prior to the yield curve: spot and forward rates

1.1 INTEREST RATES, PRESENT AND FUTURE VALUES, INTEREST COMPOUNDING

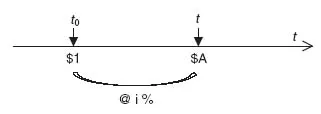

Consider a period of time, from t0 to t, in Figure 1.1.

$1 invested (or borrowed) @ i from t0 up to t gives $A. t is the maturity or tenor of the operation. $1 is called the present value (PV), and $A the corresponding future value (FV). i represents the interest rate or yield.

In this basic operation, no interest payment is made between t0 and t: in such a case, i is called a “0-coupon rate” or “zero” in short. Zeroes are also called “spot rates” as they refer to currently prevailing rates (at t0). Let us denote zt the current zero for a maturity t.

In the financial markets, the unit period of time is the year, and the interest rates, or yields, are expressed in percent per annum (% p.a.), that is, per year. In the US market, interest rates may also be expressed on a semi-annual basis (s.a.) with respect to the market of US bonds paying semi-annual coupons. Database providers, such as Bloomberg or Reuters, do well in always specifying whether the rates they mention are expressed on an annual or a semi-annual basis.

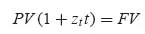

If the maturity t = 1 year, and z1 the corresponding zero rate expressed in % p.a., the relationship between PV and FV is

meaning that the future value FV is the sum of the present value PV plus the interest computed on PV @ z1, that is, PV × z1.

If the maturity t is shorter than 1 year, the interest is computed pro rata temporis, t being counted as a fraction of a year. Equation 1.1 becomes

The time unit period of 1 year is a natural compounding time unit, that is, above 1 year, interests must be compounded (see the following). On the US market, the compounding time unit is normally 0.5 years.

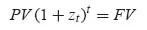

If t > 1 year for zeroes expressed on an annual basis, or >0.5 year for zeroes expressed on a semi-annual basis,

- either t is a round number of years (or of half-years in the case of semi-annual basis), Eq. 1.1 becomes

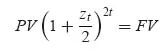

that is, zt is compounded t times. Indeed, suppose that t = 2 years. Since for a zero-coupon there are no cash flows (of interest) paid between t0 and year 2, the interest relating to the first year is compounded so that, for the second year, the present value at the beginning of year 2 becomes

and earns interest @ z2 during the second year so that

In the case of compounding of s.a. rates, Eq. 1.3 becomes

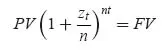

And, more generally, if the zero rates were to be compounded n times a year,

- or t is not a round number of years, for example t = n years + t′. In this case the market practice consists of combining both rules (Eq. 1.2 and Eq. 1.3):

1.1.1 Counting the number of days

The rules for expressing t differ from one market to another: fractions of a year may be counted as a number of days nd that can be based on the actual (ACT) number of days, or on full months of 30 days plus actual number of days for a fraction of a month, the year being counted as a 360-days or a 365-days year, to follow the most usual conventions.

The market practice uses the following day count conventions:

In USD:

- on the money market (cf. Section 2.1): ACT/360, that is, the actual number of days, divided by (a year of) 360 days;

- on longer maturities: USD swap rates 1: 30/360 (semi-annual), US government Treasury bonds: ACT/365 (semi-annual).

In EUR:

- on the money market: ACT/360;

- on longer maturities: EUR swap rates: 30/360, EUR sovereign bonds: ACT/ACT.

The set of zts, or {zt}, is called the term structure of interest rates, or the yield curve. Strictly speaking, this wording should apply only to spot or zero-coupon interest rates, and not to usual bond yields.

The set {zt} plays a key role in financial calculus, especially for pricing interest rate products, such as bonds, or instruments such as derivatives. Indeed, these instruments are anything but combinations of cash flows to be paid or received on some future dates, so that to value them at the current time, one needs to compute the present value of any future cash flows involved, by ...