- 190 pages

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

Strategy for Real Estate Companies

About this book

Explaining how to take a company to the next level and stay a step ahead of the competition in any market cycle, this book reveals how to fully use tools to target and develop for lifestyles, take advantage of available sites, and apply best practices from other countries. It covers small and large companies, those working in a single local market, as well as those national in scope.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

CHAPTER 1

The Need for a Strategy

Every company has a strategy. The question is whether the strategy is explicit—the result of careful planning, born out of a consensus among the company’s top leadership—or implicit—an unconscious decision to keep on doing what the company has been doing and simply muddle through. Many real estate firms follow the latter course.

This book is an introduction to strategic planning for all types of real estate companies—large and small, private and public, those that are focused on a narrow set of geographies or products and those that are fully diversified, multi-disciplined concerns. It is a primer on the most important issues managers face: how to set the direction of the firm and implement an action plan to ensure that the strategy is pursued.

Strategic planning is an intellectual-sounding name for a deceptively simple process: determining where a business is going and how it plans to get there. Especially at a time when the real estate industry is rapidly changing and consolidating, it is important to define company goals in both absolute and relative terms and to tie goals to specific strategies. Without this important step, strategic planning becomes only an empty exercise that does not achieve any goal.

It is important to demystify strategic planning. It is not a black box or a magic bullet. It involves determining what senior managers want a company to be when It grows to the next level—and then figuring out how to get there. Asking where the company wants to go and how to get there every few years is a healthy exercise, one that is essential when times are uncertain but equally important as conditions improve. The most successful companies regularly monitor economic and real estate market cycles, and revisit and adjust their strategies accordingly.

Companies with well-defined strategic plans and a well-defined business strategy are at a distinct advantage: they have a common direction that is clear to all. For publicly traded companies, the market has spoken; those with a clear focus and a well-articulated strategy tend to garner a premium from analysts and shareholders. For all real estate companies, a strategic plan and the planning process itself offer a competitive edge, enabling the company to focus its talents and energies and to measure achievements against expectations.

Some examples:

- In the early 1990s, the northeast and mid-Atlantic partners of a national multifamily company were having a difficult time raising capital to fund their development activities, a frustrating experience in the face of seemingly favorable market fundamentals. They decided to turn to Wall Street for capital and formed a real estate investment trust (REIT) in 1993. Later, as they discovered that the company was not able to grow organically as quickly as they had hoped, the firm’s leaders decided that the best path to growth lay in a merger with a California-based multifamily REIT that had similar strategies and complementary strengths. During the recession of the early part of the first decade of the 21st century, the merged firm remained true to its market strategy (Class A, high barriers to entry), repurchased stock, slowed its development pipeline, and sold assets to keep its balance sheet strong and position itself for growth during the next upturn. The company emerged from the recession as an industry leader with a robust development pipeline.

- A private, regional residential real estate firm noted that its competitors seemed to be more successful in generating wealth for their principals despite operating at a scale similar to its own but without the same high level of market awareness and risk. Why, the company’s leaders wondered, were others taking fewer risks and making more money while they seemed to be paying what they felt was too much for capital while still providing loan guarantees personally? After evaluating what their firm did best, they recognized that they had been unnecessarily “giving away” their valuable presence in the market and their recognizable brand, which was able to generate premium pricing and occupancy for their equity partners. They also realized that by broadening their joint venture strategy, they could become an equity partner in deals in return for their sweat equity, and that they needed to work harder to find the right equity sources and partners. In 2007, the company formed a joint venture with an institutional investor that has enabled it to grow and expand into new markets, increasing the partners’ equity stake in a much larger portfolio while reducing their financial exposure.

- A Texas-based development firm that built 5 million square feet of office and industrial space in Austin, Dallas, and Houston found itself in crisis as the state’s energy-dominated economy cratered in the early 1980s. Faced with a hemorrhaging balance sheet and no prospects for development in its core markets for some time, the company embarked upon a transition into a third-party management, leasing, transaction, and investment sales business. The firm experienced tremendous growth during the 1980s and 1990s, merging with and acquiring other companies to become a national provider of real estate services, including research and tenant advisory services. Having successfully transformed the company into one of the nation’s preeminent service companies, the principals felt they were missing out on development opportunities and that they could effectively leverage the company’s service platform, parlaying it into development deals, and vice versa. In 2007, the firm had a $500 million development pipeline, and its principals are wrestling with how to best integrate development capabilities into a large service-based organization in order to continue the firm’s legacy as an evergreen company.

- In the early 1980s, a second-generation, family-owned local homebuilding company found itself struggling in the midst of the housing downturn. It turned out that its profits came from its horizontal land development activities, while its core vertical homebuilding business was losing money. The solution was quite simple: sell the homebuilding business, along with a long-term contract to continue providing finished lots, to a large national builder that was interested in penetrating the market. The company then reinvested the proceeds, evolving into a regional, multidisciplined real estate company with commercial, retail, and industrial land and vertical building capabilities, rental apartments, general contracting, and—after its noncompetitive agreement burned off—a homebuilding business. By the late 1990s, with no obvious heir apparent, the family patriarch decided it was time to make a transition from family to professional management, with the objectives of continuing to grow the business and securing the company’s legacy. The firm’s new chief executive officer (CEO) examined the company business by business to determine their relative profitability. By 2007, the company had shed certain businesses, become more sophisticated in its use and redeployment of capital, partnered with other successful industry players in increasingly larger projects, and was actively acquiring, developing, and managing a diverse range of real estate products throughout the southeastern United States and beyond.

These are just four examples of real estate companies that have faced strategic challenges at crucial points in the economic and real estate market cycle. Each company needed to determine its future direction and how it planned to get there. All of them needed strategies to guide this process.

Planning Is Invaluable

As General Dwight D. Eisenhower once said, “Plans are useless, but planning is indispensable.” No matter how much effort and thought a company puts into a strategic planning process, the plan will never precisely forecast what will happen to that company. However, no matter how imperfect the plan, the planning process will define the upside potential and the downside risks that the company faces, enabling it to build capacity to deal with known external opportunities and threats as well as to keep the company flexible enough to handle unanticipated opportunities and threats, while forging a conscious consensus among top managers regarding the direction of the company. The conscious consensus among managers is the most important outcome of the strategic planning process.

Strategic planning should aim to define the company’s future direction, focusing on opportunities, considering its internal and external realities, its history, its people, and the realities of capital, the marketplace, and other factors. Even if top managers already have a fairly good idea of the direction in which the company should be headed, they can benefit from a strategic planning process that tests hypotheses, explores more specific potentialities, and provides input—and creates buy-in—from the key players in the organization who will be charged with implementing the strategy. The process should take a fresh look at the company, its products or services, and the market to define a new vision for the firm or potentially chart a new course.

The time frame encompassed by a strategic plan varies from company to company, depending on the financial condition of the organization, the economic outlook of the industry, and company executives’ experience with strategy. Typically, a strategic plan should look out over a three- to five-year horizon, because this typically has been the time frame in which the real estate market shifts from one phase of the cycle to another: from upturn to maturity, or downturn to recovery, and so forth. It is true that some real estate expansion periods last longer than others, but companies are well served if they revisit their strategy over each phase of the cycle. For some, this revisit simply confirms their plans, but for others it provides an opportunity to fine-tune, adjust, and question what they should do differently during the extended cycle, as well as when the real estate economy changes.

Forest City Enterprises, Inc., is a company that agrees planning is valuable. As its mission statement highlights, the company “operates with a consistent focus on its strategic plan. The strategy is clear: We focus on target markets with high growth potential and where we enjoy distinct competitive advantages.”

The Real Estate Cycle: Why Planning Is Particularly

Important for Real Estate Companies

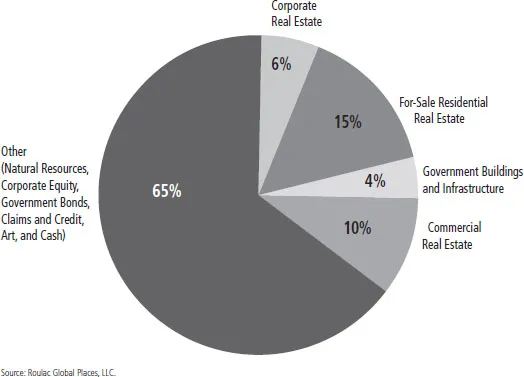

Real estate is one of the largest segments of the national economy. Recent work by Dr. Stephen Roulac estimates that the entire asset base in the United States is valued at $200 trillion; that is what it would take to buy the country. Real estate, broadly defined, represents 35 percent of that asset value and, at approximately $90 trillion, is the single largest asset class in the country (figure 1–1).

Real estate also is one of the most cyclical industries in the economy. Real estate experiences higher highs and lower lows than most other industries, including the automobile, aerospace, energy, and other highly cyclical industries. Even more important, a moderation of growth in the overall economy can cause a recession in real estate, particularly if there is a rapid erosion of consumer confidence or a change in capital market liquidity, the lifeblood of real estate. As the saying goes, “When the economy catches a cold, the real estate industry contracts pneumonia.”

Figure 1–1: UNITED STATES ASSET BASE

More than any other factor, the reaction of industry players to the real estate cycle determines what the strategy of a real estate company should be. When formulating a strategy, a company therefore must start with an understanding of the effects of these extreme cycles. To ignore the extreme cyclical nature of the industry is to place a company in peril, dooming it to continuous crisis during every real estate depression. If companies do not plan adequately for deep downturns, they will never survive to enjoy the inevitable upturns.

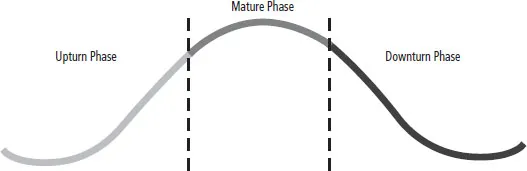

Most real estate veterans would say that they know that real estate is cyclical. But the unusually long run that real estate experienced in the 1990s and from 2000 through 2005 seems to have made many in the industry forget this reality—or at least not plan adequately for the cycle’s eventual turn, particularly in the residential sector. No one who was working for a homebuilding company in 2006 and 2007 is likely to forget for quite some time that real estate is a cyclical business. The real estate cycle comprises three general phases, as shown in figure 1–2 and described below.

Upturn Phase

This phase typically lasts one to two years. In its early stages, most sectors remain in a “buyer’s market,” as smart buyers recognize that this period—when many sellers still have a downturn mentality—is a good time to buy. Most buyers remain cautious; they are not even sure an upturn has begun. Once vacancies fall into a reasonable range in response to general economic recovery, however, the usual result is rising demand for space and apartments. Yet the lead time required for developers to respond to this demand is too long to produce the new space or units that are needed. Consequently, as the upturn continues, managers allow rents of existing space or units to rise while they reduce or eliminate concessions. Homebuilders are able to obtain higher—in some cases, much higher—prices for their products. The appetite for investment tends to be strong during this phase, further driving property values up.

Mature Phase

Although the real estate industry has just experienced a historically long period of expansion, the mature phase typically lasts for one to three years. The mature phase is a time of approximate equilibrium. Property owners must be willing to sell into the mature phase; those trying to catch the peak of the cycle may miss it. Toward the end of the mature phase, however, an increasing amount of new space and an excess inventory of rental apartments and for-sale homes typically come onto the market, causing a shift, virtually overnight, to a buyer’s market. The increased supply forces homebuilders to lower prices and owners to lower rents and increase concessions. Despite rising vacancies and falling rents, unduly optimistic projections about the future performance of new projects generally keeps the pipeline full of additional new inventory, unless financial institutions and investors demand increased preleasing and more conservative absorption and rental rate assumptions in the pro formas. Property values are the last to soften in the mature phase.

Figure 1–2: REAL ESTATE CYCLE

Downturn Phase

Usually lasting from two to four years—although some markets have experienced much longer downturns (witness Houston in the 1980s, Los Angeles in the 1990s, and, perhaps, Detroit in the first decade of the 21st century)—the downturn is a period of adjustment. Falling demand and excess capacity force drastic concessions, lower rents, lower home prices, and lower values. The result is the bankruptcy of marginal projects and companies and a serious decline in the financial performance of nearly every company and project in the market. Land prices are typically the last in the industry to get adjusted to new market realities, but these, too, eventually are brought down by sagging demand. The bankruptcy of developers, coupled with unduly pessimistic demand projections by financial institutions and investors hurt by the downturn, limits the development of any new product well beyond the period of the downturn, thus setting the foundation for the next upturn.

Historically, both undue optimism and undue pessimism have been major factors in the extremely cyclical nature of the real estate industry. In the early 1990s, for example, many industry observers and participants predicted a paralysis in the industry f...

Table of contents

- Cover

- Titlepage

- Copyright

- Authors

- Acknowledgment

- Contents

- Foreword

- Chapter 1: The Need for a Strategy

- Chapter 2: Mission, Vision, and Core Values

- Chapter 3: Industry Role Strategy

- Chapter 4: Customer Strategy and Brand

- Chapter 5: Core Competency Strategy

- Chapter 6: Growth and Geographic Deployment Strategy

- Chapter 7: Profitability Strategies

- Chapter 8: Organizational Strategies

- Chapter 9: Capital Strategies

- Chapter 10: Cycle Strategies

- Chapter 11: The Strategy Process

- Chapter 12: Case Studies

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Strategy for Real Estate Companies by Charlie A. Hewlett,Gadi Kaufmann in PDF and/or ePUB format, as well as other popular books in Business & Real Estate. We have over 1.5 million books available in our catalogue for you to explore.