One of the most important challenges that people in senior management positions face is the responsibility of ensuring their organizations' effective practice of performance management. As this book reveals, performance management comprises an interdisciplinary field of study and practice that draws upon a wide set of business disciplines, including strategic management, organizational behaviour, organizational theory, and management accounting.

This book provides a contemporary examination of theories, issues, and practices related to performance management. An original performance management framework helps structure the book, and in particular the ordering and layout of the book's chapters. Unlike other performance management frameworks, the one used here is grounded in concrete organizational phenomena, therefore making it more accessible and meaningful to practitioners, scholars, and students.

Frequently asked questions

How do I cancel my subscription?

Simply head over to the account section in settings and click on “Cancel Subscription” - it’s as simple as that. After you cancel, your membership will stay active for the remainder of the time you’ve paid for. Learn more here.

Can/how do I download books?

At the moment all of our mobile-responsive ePub books are available to download via the app. Most of our PDFs are also available to download and we're working on making the final remaining ones downloadable now. Learn more here.

What is the difference between the pricing plans?

Both plans give you full access to the library and all of Perlego’s features. The only differences are the price and subscription period: With the annual plan you’ll save around 30% compared to 12 months on the monthly plan.

What is Perlego?

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 1000+ topics, we’ve got you covered! Learn more here.

Do you support text-to-speech?

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more here.

Is Strategic Performance Management an online PDF/ePUB?

Yes, you can access Strategic Performance Management by Ralph W. Adler in PDF and/or ePUB format, as well as other popular books in Business & Managerial Accounting. We have over one million books available in our catalogue for you to explore.

■Show how the study and practice of performance management is an interdisciplinary as opposed to a multidisciplinary endeavour.

■Identify and discuss the four disciplines that contribute to the study of performance management.

■Describe the plan of the book.

Performance management as an interdisciplinary field of study and practice

Performance management is often considered to be, or certainly such is the case for accountants, a subfield of management accounting. Although it is certainly the case that the major advancements in the field of performance management have been driven by management accountants, it is fairer and more accurate to view performance management as an interdisciplinary field of study involving the disciplines of strategic management, organizational behaviour, organizational theory, and management accounting. Performance management, which is broadly about how organizations design their organizational structures, systems, and cultures to encourage employees’ implementation of their respective organizations’ strategies, is informed and enriched by practitioners and scholars working across these four broad disciplines. Contributions to this interdisciplinary field of study have been ongoing for the past 50-plus years.

The description of performance management as an interdisciplinary science should not be confused with the word multidisciplinary. The latter term refers to studying a particular topic from various fields of speciality, while all the time remaining inside one’s speciality. In other words, an organizational behaviourist would study performance management with a purely organizational behaviour lens. This researcher or practitioner would not employ other lenses (e.g., organizational theory, management accounting, or strategic management), and most certainly would not adopt a unified lens that draws together the contributing business disciplines. In contrast, interdisciplinary research and practice requires scholars and practitioners to situate themselves at the intersection of the multiple contributing disciplines and employ a single, integrated lens.

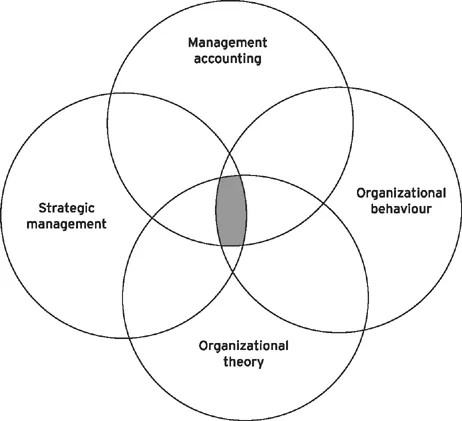

Figure 1.1 illustrates the multidisciplinary and interdisciplinary nature of performance management. Each of the diagram’s four circles represents a disciplinary perspective; and the intersection of the four circles, which appears as the shaded region, represents performance management’s interdisciplinary perspective.

Figure 1.1Multidisciplinary and interdisciplinary perspectives

Performance management’s four contributing academic disciplines

Let’s look at how each of the four separate disciplines contributes to practitioners’ and managers’ uses of performance management. Management accounting is a field of study and practice that involves the collection, analysis, and communication of information for internal decision-making. The ultimate aim of management accounting is to produce better decision-making and, in the process, generate better organizational performance. As performance management practitioners and scholars, our particular interest in management accounting lies in its ability to direct employee attention. Management accounting’s construction of budgets is a classic example. Budgets serve multiple purposes that are relevant from a performance management perspective. First, they serve to allocate resources. This allocation informs employees of the strategic priorities of the company. Organizations that allocate substantial parts of their budgets to research and development initiatives are communicating something very different from organizations that allocate small sums to their research and development efforts. Budgets can also reinforce organizational lines of authority and responsibility. Managers are typically assigned the task of overseeing a particular part of the organization. The budget communicates what this part is (including the employees and other assets that come under a manager’s control) and provides a general outline of what is expected (by virtue of the line items that constitute the budget). Furthermore, budgets serve to influence what employees do, and this influence can be further supported by attaching rewards and/or penalties to employee achievements. In particular, the targets management accountants help set when formulating budgets are highly likely to impact employee behaviour.

Strategic management comprises the formulation, implementation, and control of the unique set of activities an organization will undertake to achieve its major goals and initiatives. An organization’s senior managers, who are invariably tasked with this responsibility, will systematically seek to grow and leverage their respective organization’s core competencies to achieve a sustainable competitive advantage. While strategy formulation is not explicitly a part of performance management, the process of strategy implementation certainly is. Accordingly, strategic management is a central part of performance management.

Organizational behaviour (OB) involves the study of how people, as individuals and as part of a larger group, perform their work. OB is essentially social psychology applied to work settings. It examines human behaviour in a work environment and assesses how task structure, motivation, leadership, and communication affect organizational performance. OB practitioners and scholars aim to understand and predict worker behaviour in their similar quests to create more efficient and effective organizations.

Organizational theory (OT) comprises the study of entire organizational systems, as well as the groups of people and subparts that constitute these organizations. It is particularly concerned with how to best design and structure organizations. Part of the OT process involves matching the organization’s design and structure with key internal and external factors. The former includes influential managers and technocrats within an organization, and the latter includes competitors, regulators, lobbyists, etc. OT practitioners and scholars are interested in ensuring appropriate organizational and environmental alignment.

As the preceding paragraphs reveal, strategy formulation, and in particular the design of winning strategies, is a necessary but not a sufficient part of an organization’s attainment of superior performance. What is further needed is senior management’s effort to ensure the organization’s strategy is being implemented, which is by definition performance management.

Parallels can be drawn between an organization’s formulation and implementation of its strategy and a sports team’s development and implementation of a game plan. In particular, no matter how masterful a sports team’s game plan may be, it will have no effect and no relevance unless the players execute the plan. In a similar fashion, an organization’s strategy may look good on paper, but unless and until it is implemented it will be of no help or consequence. This idea of irrelevance is well captured by the Japanese proverb: “Strategy without action is a daydream.”

Ensuring the organization’s strategy is being implemented, and, some practitioners and scholars would further add, the strategy being amended as the situation may warrant, is the essence of performance management. How an organization goes about ensuring that employees implement its strategy is the focus of this book. This task, which is the responsibility of senior management, is highly challenging but eminently attainable. As this book reveals, senior managers need to possess clear understandings of their employees’ motivation if they, the senior managers, are to be successful practitioners of performance management.

The motivation of employees requires more than simply energizing them. It also requires directing employee energy. A good example of where employees were energized but not effectively directed is well illustrated by a story about the UK’s Department for Social Development (DSW). A manager responsible for the various offices’ operations became highly concerned by one of the office’s persistently long lines that regularly stretched out of the office’s front door and around the block. The manager instructed the employees of this office to address the problem. The employees responded by moving the reception area deeper inside the building and erected extensive client queuing barriers to organize the clients into a maze of many channels. While the employees were certainly energized into action, the solutions they enacted essentially changed nothing about the situation. The amount of time clients spent standing in line did not change, for the employees failed to address the underlying reasons for the long lines.

The task of energizing employee enthusiasm draws on principles of leadership. Meanwhile, the task of directing employees’ energy so that it is congruent with the organization’s ambitions relies on developing organizational structures, systems, and cultures that encourage desirable employee behaviours and discourage undesirable ones. The remainder of the book examines the performance management practices organizational managers draw upon to ensure high levels of employee motivation, loyalty, and commitment to implementing the organization’s strategy.

Plan of the book

The book is divided into four main parts. The first part, “Performance management beginnings,” consisting of three chapters, explores the history and beginnings of performance management. Chapter 2 defines performance management and discusses how performance management is practised, including who is involved and their various roles and responsibilities. Chapter 3 discusses the rise of performance management, and in particular the influential historical milestones that enabled its emergence. This chapter also introduces a novel conceptual model that portrays the key elements of performance management and serves as a roadmap for the book’s subsequent chapters. Chapter 4 discusses the five main theories that underpin the study of performance management: contingency theory, agency theory, goal-setting theory, resource-based theory, and stakeholder theory. These theories derive from the academic disciplines of organizational sociology, organizational psychology, economics, and organizational strategy.

Part II, “Organizational strategy,” presents and discusses organizational strategy. Since the purpose of performance management is to ensure employees are implementing their respective organizations’ strategies, an understanding of the composition and operation of organizational strategy is essential to the study of performance management. Chapter 5 discusses how organizations determine their purposes and, in the process, develop enduring goals and objectives that are meant to motivate and guide employee behaviour. The next two chapters discuss the different paths organizations can follow when pursuing their respective goals and objectives. Chapter 6 defines organizational strategy and discusses its importance to an organization’s success. It then proceeds to identify two types of organizational strategy: corporate-level and business-unit-level. Chapter 7 examines the concept of business-unit-level strategy, or what is commonly referred to as competitive strategy. It includes a discussion and critique of the competitive strategy taxonomies of Miles and Snow, Porter, Cooper, and Kim and Mauborgne. The chapter concludes by discussing some basic associations between competitive strategy and performance management system design.

Part III, “Levers of employee influence,” discusses the three main levers of performance management: organizational structure; organizational systems, processes, and procedures; and organizational culture. Chapter 8 identifies the defining dimensions of organizational structure as complexity, formalization, and centralization. Following a discussion about the need for these dimensions to complement one another, the chapter proceeds to discuss the four main types of responsibility centres and how senior managers decide which one of them is best to use. Chapter 9 examines how an organization uses organizational systems, processes, and procedures to influence employees’ implementation of the organization’s strategy. The chapter explores organizations’ use of performance measurement systems, employee incentive systems, and human resource systems to exercise employee influence. Chapter 10 covers organizational culture. The chapter identifies the six dimensions of organizational culture. It further discusses how senior managers can identify gaps between their actual and ideal organizational cultures, as well as what an organization’s leaders can do to create better alignment between their organization’s culture and the organizational strategy it pursues.

The final part of the book, Part IV, “Contingent factors,” identifies and discusses important internal and external contingent factors that must be considered when designing performance management systems. These contingent factors must be incorporated into the construction and operation of the three main levers of performance management if the organization is to achieve good performance management fit. Chapter 11 examines internal contingent factors, while Chapter 12 considers external contingent factors.

Chapter 13 presents the book’s conclusion. This chapter revisits the conceptual model of performance management introduced in Chapter 3. Drawing on the work of Ferreira and Otley (2009) and Malmi and Brown (2008), the chapter discusses the need for senior managers to view their performance management systems as holistic. In particular, the chapter champions...