NONE

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

System of Environmental-Economic Accounting 2012 : Central Framework

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

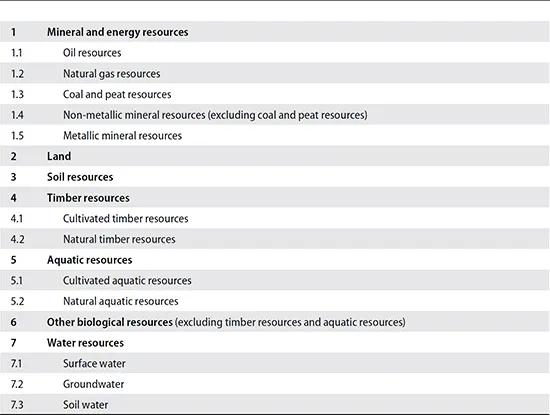

Publisher

INTERNATIONAL MONETARY FUNDeBook ISBN

9789211615630

Year

2017Chapter V: Asset accounts

5.1 Introduction

5.1 Assets are considered items of value to society. In economics, assets have long been defined as stores of value that, in many situations, also provide inputs to production processes. More recently, there has been consideration of the value inherent in the components of the environment and the inputs the environment provides to society in general and the economy in particular. The term “environmental asset” is used to denote the source of these inputs which may be measured in both physical and monetary terms.

5.2 One motivation for considering environmental assets is the concern that current patterns of economic activity are depleting and degrading the available environmental assets more quickly than those assets can be regenerated. Hence, there is also concern about their long-term availability. Current generations may thus be seen as “stewards” for the range of environmental assets on behalf of future generations. There is a general aim to improve the management of environmental assets, taking into account the sustainable use of resources and the capacity of environmental assets to continue to provide inputs to the economy and society.

5.3 This general aim is a key driver for the development of the SEEA and, in particular, for the measurement of assets and the compilation of asset accounts. In this context, the aim of asset accounting in the SEEA is to measure the quantity and value of environmental assets and to record and explain changes in those assets over time.

5.4 For environmental assets, the physical and monetary changes over the period include additions to the stock of environmental assets (due, e.g., to natural growth and discoveries) and reductions in the stock of environmental assets (due, e.g., to extraction and natural loss).

Chapter structure

5.5 The present chapter describes accounting for environmental assets. Section 5.2 provides a detailed discussion of the concept of environmental assets in the Central Framework, working from the general definition of environmental assets outlined in chapter II. Section 5.3 describes the structure of the accounts and the accounting entries that are required to compile asset accounts, including opening and closing stocks, additions to stock, reductions in stock and revaluations.

5.6 Section 5.4 examines two key dimensions of the compilation of asset accounts: the principles of defining depletion of environmental assets in physical terms, with particular focus on the depletion of renewable environmental assets, such as aquatic and timber resources; and, in relation to monetary asset accounts, approaches to the valuation of environmental assets and, in particular, the net present value (NPV) approach. The annex to the chapter discusses NPV in greater depth.

5.7 Sections 5.5-5.11 outline asset accounting for the range of individual environmental assets. Detail is provided on the measurement scope for each of these assets, the structure of the asset accounts and other relevant conceptual and measurement issues. While there are general principles that can be applied across all environmental assets, each environmental asset has specific characteristics that must be considered individually.

5.2 Environmental assets in the SEEA Central Framework

5.2.1 Introduction

5.8 As defined in chapter II, environmental assets are the naturally occurring living and non-living components of the Earth, together constituting the biophysical environment, which may provide benefits to humanity. In the Central Framework, environmental assets are viewed in terms of the individual components that make up the environment, with no direct account taken of the interactions between these components as part of ecosystems.

5.9 The present section explains the general measurement boundary for environmental assets in the Central Framework, including a description of the classification of environmental assets and an articulation of the relationship between environmental and economic assets.

5.2.2 Scope of environmental assets

5.10 The scope of environmental assets in the Central Framework is determined through a focus on the individual components that make up the environment. This scope comprises those types of individual components that may provide resources for use in economic activity. Generally, the resources may be harvested, extracted or otherwise moved for direct use in economic production, consumption or accumulation. The scope includes land and inland waters that provide space for undertaking economic activity.

5.11 There are seven individual components of the environment that are considered environmental assets in the Central Framework. They are mineral and energy resources, land, soil resources, timber resources, aquatic resources, other biological resources (excluding timber and aquatic resources), and water resources. These individual components have been the traditional focus for the measurement of environmental assets through the development of specific asset or resource accounts. This chapter discusses asset accounts for each of these environmental assets and the relevant measurement boundaries in physical and monetary terms.

5.12 The coverage of individual components in the Central Framework does not extend to the individual elements that are embodied in the various natural and biological resources listed above. For example, carbon and nitrogen are not considered individual environmental assets in the Central Framework.

5.13 The measurement scope of the environmental assets of a country is limited to those contained within the economic territory over which a country has control. This includes all land areas, including islands; coastal waters including waters and seabeds within a country’s exclusive economic zone (EEZ); and any other water or seabeds in international waters over which the country has a recognized claim. The extension of geographical scope beyond environmental assets on land is of particular relevance in the measurement of stocks of aquatic resources and mineral and energy resources.

5.14 In physical terms, the measurement scope for each individual component is broad, extending to include all of the resources that may provide benefits to humanity. However, in monetary terms, the scope is limited to those individual components that have an economic value based on the valuation principles of the SNA. For example, in physical terms, all land within a country is within scope of the SEEA so as to allow for a full analysis of changes in land use and land cover. However, in monetary terms, some land may have zero economic value and hence should be excluded. The broader scope applied in physical terms aims to account better for the environmental characteristics of the individual components. Issues concerning the valuation of environmental assets are described in more detail in section 5.2.3.

Classification of environmental assets in the Central Framework

5.15 The classification of environmental assets in the Central Framework presented in table 5.1 focuses on individual components. For each of these environmental assets, a measurement boundary in physical and monetary terms must be drawn for the purposes of asset accounting. These boundaries are described in sections 5.5–5.11.

Table 5.1 Classification of environmental assets in the SEEA Central Framework

5.16 The volume of water in the sea is not considered in scope of water resources in the Central Framework because the stock of water is too large to be meaningful for analytical purposes. The exclusion of the sea in terms of a volume of water resources does not in any way limit the measurement of sea-related individual components such as aquatic resources (including fish stocks on the high seas over which a country has harvesting rights) and mineral and energy resources on or under the seabed. The volume of air in the atmosphere is also not in scope of environmental assets in the Central Framework.

5.17 Although seas and the atmosphere are excluded, the measurement of exchanges and interactions with them is of interest. In this context, the interactions between the economy and the sea, and between the economy and the atmosphere, are recorded in the Central Framework in various ways. For example, measures of the abstraction of sea water are included in the physical flow accounts for water, and measures of emissions from the economy to the atmosphere and seas are recorded in physical flow emission accounts.

Natural resources

5.18 Natural resources are a subset of environmental assets. Natural resources include all natural biological resources (including timber and aquatic resources), mineral and energy resources, soil resources and water resources. All cultivated biological resources and land are excluded from scope.

Land and other areas

5.19 For most environmental assets in the Central Framework, conceptualizing the supply of materials to economic activity—for example, in the form of fish, timber and minerals—is straightforward. The exception in this regard is land.

5.20 The primary role of land in the SEEA is to provide space. Land and the space it represents define the locations within which economic and other activity is undertaken and within which assets are situated. Although not physical, this role of land is a fundamental input to economic activity and can have significant value, as is most commonly observed in the varying valuations given to similar dwellings in locations that have different characteristics in terms of landscape, access to services, etc. This conceptualization of land can also be applied to marine areas over which a country has a recognized claim, including its exclusive economic zone.

5.21 The term “land” as applied in the SEEA also encompasses areas of inland water such as rivers and lakes. For certain measurement purposes, variations in this boundary may be appropriate, for example, when considering the use of marine areas for aquaculture, conservation or other designated uses. These considerations are discussed in section 5.6.

5.22 A clear distinction is made between land and soil resources. The physical inputs of soil are reflected in the volume of soil and its composition in the form of nutrients, soil water and organic matter. This distinction is discussed further in sections 5.6 and 5.7.

5.23 In the valuation of land, both the location of an area and its physical attributes (e.g., topography, elevation and climate) are important considerations. The valuation of land is discussed in Section 5.6.

Timber, aquatic and other biological resources

5.24 Biological resources include timber and aquatic resources and a range of other animal and plant resources such as livestock, orchards, crops and wild animals. Like most environmental assets, they provide physical inputs to economic activity. However, for biological resources, a distinction is made between whether the resources are cultivated or natural, based on the extent to which there is active management over the growth of the resource.

5.25 Maintaining this distinction in the Central Framework is important for ensuring that clear linkages can be established to the treatment of these resources in the production accounts and asset accounts of the SNA.

5.26 The cultivation of biological resources can take a wide range of forms. In some cases, the management activity is highly involved, which is the case for battery farming of chickens and the use of greenhouses for horticultural production. In these situations, the unit undertaking the production creates a controlled environment, distinct from the broader biological and physical environment.

5.27 In other cases, there may be relatively little active management as is the case, for example, with broad-acre cattle farming and the growing of plantation timber. In these cases, the biol...

Table of contents

- Cover Page

- Title Page

- Copyright Page

- Contents

- Foreword

- Preface by the Secretary-General of the United Nations

- Preface

- Acknowledgements

- List of abbreviations and acronyms

- I Introduction to the SEEA Central Framework

- II Accounting structure

- III Physical flow accounts

- IV Environmental activity accounts and related flows

- V Asset accounts

- VI Integrating and presenting the accounts

- Annex I Classifications and lists

- Annex II Research agenda for the SEEA Central Framework

- Glossary

- References

- Index

- TABLES

- Footnotes