![]()

1 A Review of the Current Situation

Introduction and Definition of Sovereign Risk Analysis

Sovereign risk analysis concerns itself with the identification of countries which will be unable to meet their commitments on sovereign external debt, defined as all cross-border loans granted by a private bank in one country directly to a foreign government or publicly guaranteed loans made to a foreign firm. Necessary prerequisites to a study of this subject are an examination of the determinants of sovereign borrowing and lending and a review of the current international debt problems. These are the objectives of this chapter. First, we analyse the economic determinants of capital flows between countries. Sovereign borrowing and lending represents one type of international capital flow. Secondly, we review the current situation (see p. 9) followed by reference to historical precedents (p. 23); a thorough examination of these two subjects establishes the framework for the forthcoming chapters.

The Economic Determinants of International Capital Flows

Prior to any review of the current international debt problem or discussion of how to analyse sovereign risk, it is necessary to examine the reasons for international capital flows, especially those that are in the form of sovereign loans. Like any economic phenomenon the question is best answered by identifying the economic determinants of these flows. For the sovereign risk analyst the exercise will be useful because it places the sovereign debt problems in a more general framework than is normally the case.

Basic principles of economics explain why cross-border lending has become an integral part of the international economy. Begin by dividing the world into two groups of economies, the ‘First’ World and the ‘Third’ World. The First World economies have a supply of capital that exceeds their domestic requirements. These are ‘surplus’ capital countries, often with well-developed capital markets that can provide capital at lower cost than elsewhere in the world. The theory of comparative advantage explains why the First World will want to export this capital. A country has a comparative advantage in the production of goods or services if it makes the goods or provides the services more efficiently than the rest of the world. The potential economic welfare of a country will improve if it exports goods in which it has a comparative advantage, and imports goods and services from countries that are relatively more efficient in their production. Capital is normally considered to be a factor input in the production process, but this does not exclude us from applying the principle of comparative advantage to the international trade of capital. Just as resource-rich countries export their raw materials, so efficient producers of capital will export capital. The First World consists of those countries which are efficient producers of capital and, therefore, exploit their comparative advantage by exporting the surplus capital. Third World countries are net importers of capital because their own capital base is not sufficiently well developed to meet their domestic demand requirements. The rate of return will differ in the two worlds: it will be relatively lower in the capital-abundant First World and relatively higher in the capital-deficient Third World. Trade in capital between the two groups gives rise to international flows of capital until the rates of return on capital in the two groups are equalized.

Most students of international finance will readily acknowledge that Western economic development during the past century has been responsible for the rapid expansion of the West's capital base, which in turn has created a supply of capital in excess of domestic capital requirements. The development of efficient capital markets in the West has made this First World the most efficient supplier of capital, and the rapid emergence of the oil-based economies, during the last decade, has added to this surplus capital base. Several oil-exporting nations found they had large and growing balance of payments surpluses. The revenue earned from oil was far in excess of what could be reinvested in the domestic economies of these countries. The remainder was deposited in the Western banking system, which could invest this capital in the international capital markets and earn the highest going rate of return for their customers. This ‘recycling’ of petrodollars reached its height in the mid-1970s and added considerably to the surplus capital base of the First World.

While the supply side of international capital markets is fairly straightforward, the demand side may be less clear-cut for those readers unfamiliar with theories of economic growth and development. Readers may be asking why Third World countries always demand capital in excess of their own domestic capital base. This is best explained by appealing to a development cycle’ hypothesis of economic growth. According to this, countries demand capital based on expectations of higher future income streams. By borrowing capital, the country can finance higher domestic growth rates and, also, smooth its investment and consumption paths over time. This hypothesis of economic development is a broader concept than the Friedman (1957) permanent income hypothesis of consumption1 which refers to household consumption patterns. The Friedman theory explains household borrowing and lending patterns in terms of the need to smooth consumption paths over time in the face of income disturbances, whereas in the development cycle hypothesis of economic growth the smoothing function is secondary to the main reason for borrowing: to finance a more rapid rate of growth (and therefore development) in the country than would be possible in the absence of borrowed capital.

If the country's domestic capital base is insufficient to meet its growth rate targets, it will borrow the capital from the international capital markets, that is, it will import capital. Provided the expected marginal productivity (i.e. the increase in the country's output brought about by a given unit increase in capital) of the domestic endowment of capital exceeds the rate of interest that the country pays for the employment of this external capital, the country will be a net importer of capital. This external capital will allow the country to develop its own industrial base and the foreign capital will be repatriated once the economy has reached a stage in development where the domestic resource base is sufficient to meet its own capital demands.

Before going any further it is necessary to be more precise about the meaning of a developing country’ which is a net importer of capital. The International Monetary Fund (IMF)2 divides developing nations into two groups. The first group consists of oil-exporting countries, where oil exports make up at least two-thirds of the country's total exports and the country exports at least 100 million barrels a year. Cline (1984) distinguishes between oil-exporting countries which are in capital surplus and those which are not. In the latter group are Algeria, Ecuador, Nigeria, Indonesia and Venezuela. By the IMF classification, all of these countries except Ecuador would be classified as oil-exporting countries. This is important to understand, because much of the work done by the IMF relates to sovereign debt problems of the second IMF group termed ‘non oil developing countries’ or ‘non oil less developed countries’ (NOLDCs). This second category of developing countries is in turn divided into four subgroups:

(1) The net oil-exporting countries: These countries are net exporters of oil, but do not meet the criteria cited above for oil-exporting developing country status. These include: Bahrain, Bolivia, People's Republic of the Congo, Ecuador, Egypt, Gabon, Malaysia, Mexico, Peru, Syrian Arab Republic, Trinidad and Tobago, Tunisia.

(2) Net oil-importing countries but major exporters of manufactures: Argentina, Brazil, Greece, Hong Kong, Israel, South Korea, Portugal, Singapore, South Africa, Yugoslavia. These countries tend to have a higher income per head than those in the other subgroups.

(3) Net oil-importing countries with low incomes: There are 43 countries in this group, characterised by a per capita GDP that did not exceed $350.00 in 1978. This includes countries such as the Sudan, Bangladesh, Chad, Ethiopia, India, Pakistan, Sri Lanka. A full listing can be found in Appendix B of the statistical tables in World Economic Outlook (IMF, 1983).

(4) Other net oil importers: these are middle-income oil-importing nations which, in general, rely on the export of primary commodities. Countries in this category include Ghana, Jamaica, the Cameroons, Uruguay.

It should be stressed that the IMF classification of developing countries relates to the industrial base of the country rather than to whether it is a net importer of capital. Indeed, there are some industrial countries in the IMF classification of developed nations which are net importers of capital, Ireland being a good example. The sub classifications of developing nations relate to their oil-importing/exporting status rather than to their capital import status. For the purposes of this book, which concentrates on the problems of sovereign debtor nations, the IMF classification is useful because those countries classified as ‘non oil’ developing countries are also net importers of capital. In addition there are the oil-exporting countries not in capital surplus, which were noted earlier (p. 3). Most of the statistics cited in the next section (see p. 9 ff.) relate to the non oil developing countries and therefore exclude some important debtor nations. Where possible, reference is made to the ‘25 major borrowers’, four of these being major exporters of oil. The list of these countries is given in Table 1.1 (p. 11).

Up to this point, the reason why developing nations are net importers of capital has been explained, but no mention has been made of the special type of capital import, sovereign loans. The issue of why developing nations gear themselves in the way they do needs further scrutiny. Like any firm, a country which wishes to import capital has two options: it can find a bank willing to lend it the funds or external capital can be raised through equity financing. The latter is usually accomplished by permitting foreign direct investment in the country. In this case foreign capital is injected into the developing country through the establishment of foreign-owned plants. Another method of equity financing would be through the international sale of shares by a domestic firm; however, this is really a form of direct portfolio investment because it increases the proportion of foreign shareholders in the company. Therefore, a country has a ‘foreign’ gearing ratio analogous to the gearing ratio of a firm. It is defined as the ratio of foreign debt to foreign equity in a country. The external debt will consist of sovereign debt and private, non publicly guaranteed foreign debt. As was noted in the introduction to this book, the sovereign risk analyst is not directly concerned with the private type of debt and for most developing countries (as illustrated by the figures cited below) this has been a decreasing proportion of total external debt. The numerator of the ratio will also include concessional loans made to developing countries by agencies such as the World Bank. Again, they are not the direct concern of the sovereign risk analyst.

A study of the figures on the demand for external finance by developing countries reveals some interesting trends.3 Before 1973, the principal source of external finance for developing countries was foreign direct investment. During the 1960s, it made up (on average) 39 per cent of the total of external finance for developing countries. The proportion of official finance and commercial bank loans was approximately 30 per cent for each. Between 1974 and 1983, the stock of long-term private external loans to NOLDCs increased at an annual average rate of 25.5 per cent compared with an average annual growth rate of 17.5 per cent for total external debt and 11 per cent for foreign direct investment (IMF, 1983, Table 27). As a result, in the period 1973 to 1978, we can see the proportion of external finance to NOLDCs provided by commercial banks rising to 60 per cent of the total, with foreign direct investment and official finance falling to 18 and 19 per cent respectively. This trend continued in the years 1978 to 1980, with net external debt from private commercial sources rising to 70 per cent of the total. Most of the increase in the latter period was in the form of short-term loans (loans with a maturity of less than a year); these increased fivefold between 1978 and 1980 compared with a rise in long-term credit by just over half of its 1978 figure. Since 1981, the share of external credit from private sources has been falling fairly quickly, with the use of Fund credit and foreign direct investment filling the gap.

For the non oil developing nations, sovereign loans as a percentage of total private external debt ranged from between 51 per cent in 1973 to 68 per cent in 1983 (IMF, 1983, Table 32). Among the major ‘problem’ debtor countries, the proportion of sovereign external debt was even higher.

Why have so many of the NOLDCs recently opted for such high foreign gearing ratios and, more specifically, why did sovereign borrowing become a popular means of external finance in the 1970s compared with earlier periods when foreign direct investment was more common? This question can only be answered satisfactorily through further analysis of the components of the demand and supply in the international credit markets.

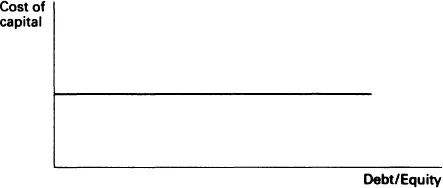

On the demand side, it is useful to begin the analysis by making a small diversion to explain the Modigliani–Miller (MM) theorem of investment.4 According to this theorem, if a firm's gearing ratio (debt finance/equity finance) is plotted on the horizontal axis and the firm's cost of capital on the vertical axis, then the line which is plotted will be horizontal. The point is illustrated in Figure 1.1. From the standpoint of capital costs, it is irrelevant whether the firm chooses a high or low gearing ratio. This is in contrast to the traditional view of the shape of the cost of capital curve, which was U-shaped. The reasoning behind the MM theorem was that, if individual investors carried out their own gearing, any change in the gearing ratio of the firm would be offset by the activities of investors, who are assumed to have the same access to capital markets and to pay the same rate of interest on loans as firms. For example, if the firm increased the percentage of debt finance through an increase in bond issues, then the effect of this on the cost of capital would be offset by an equal and opposite action on the part of individual investors, who would alter their ‘home-made’ gearing ratios. Therefore, the firm's cost of capital will be unchanged, no matter what its gearing ratio. To the practical financier, this may be counter-intuitive. The theorem appears to ignore the real world fact that the costs of capital are higher for highly geared firms because the markets perceive them to be a riskier investment. The results of the MM theorem stem from two rather special assumptions. First, that all agents have equal access to the capital markets and borrow at the same rate of interest and, secondly, that there is no possibility of default by firms. It is these assumptions, particularly the second, which rule out the usefulness of this theorem as anything but an abstract piece of theory. But although it has little practical use, it is valuable because it isolates the factors that will give rise to a U-shaped cost of capital curve.

Figure 1.1 The Modigliani–Miller theorem.

Source: Modigliani and Miller (1958); see also Hay and Morris (1979).

The MM theorem may have greater applicability in the international capital markets with respect to the foreign geari...