This book focuses on various types of crowdfunding and the lessons learned from academic research. Crowdfunding, a new and important source of financing for entrepreneurs, fills a funding gap that was traditionally difficult to close. Chapters from expert contributors define and carefully evaluate the various market segments: donation-based and reward-based crowdfunding, crowdinvesting and crowdlending. They further provide an assessment of startups, market structure, as well as backers and investors for each segment. Attention is given to the theoretical and empirical findings from the recent economics and finance literature. Furthermore, the authors evaluate relevant regulatory efforts in several jurisdictions. This book will appeal to finance, entrepreneurship and legal scholars as well as entrepreneurs and platform operators.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Douglas Cumming and Lars Hornuf (eds.)The Economics of Crowdfundinghttps://doi.org/10.1007/978-3-319-66119-3_1

Begin Abstract

1. Introduction

Douglas Cumming1 and Lars Hornuf2, 3, 4, 5

(1)

Schulich School of Business, York University, Toronto, ON, Canada

(2)

Business Studies & Economics, University of Bremen, Bremen, Germany

(3)

Max Planck Institute for Innovation and Competition, Munich, Germany

(4)

Center of Finance, University of Regensburg, Regensburg, Germany

(5)

CESifo, Munich, Germany

Lars Hornuf

Douglas Cumming

is Professor of Finance and Entrepreneurship and the Ontario Research Chair at the Schulich School of Business, York University. He has published over 150 articles in leading refereed academic journals in finance, management, and law and economics. He is the incoming editor-in-chief of the Journal of Corporate Finance (January 2018), and a co-editor of Annals of Corporate Governance, Finance Research Letters, and Entrepreneurship Theory and Practice. He is the author and editor of over a dozen books. Cumming’s work has been reviewed in numerous media outlets, including The Economist, the Wall Street Journal, The New York Times, and The New Yorker.

Lars Hornuf

is Professor of Finance at the University of Bremen. He was a visiting scholar at University of California, Berkeley; Stanford University; Duke University; and Georgetown University. From 2014 to 2017, Hornuf held a grant from the German Research Foundation on ‘Crowdinvesting in Germany, England and the USA: Regulatory Perspectives and Welfare Implications of a New Financing Scheme’. In 2016, he wrote two expert reports for the Federal Ministry of Finance on the German FinTech market and the Small Investor Protection Act. Hornuf’s work has been covered in newspapers like The Economist and Foreign Policy.

End Abstract

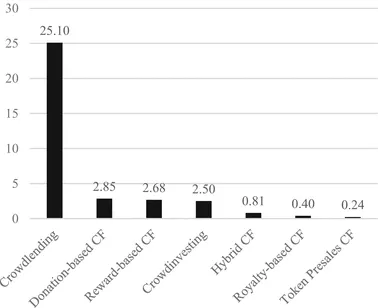

Crowdfunding has experienced tremendous growth and developed into a global multibillion-dollar business over the course of the last five years. The most successful segment of the nascent market is crowdlending, which is also referred to as peer-to-peer lending or marketplace lending, and had an estimated global market volume of USD 25 billion in 2015 (Massolution 2016). Although more recent figures on the overall market volume are not yet available, market growth has most likely continued during the years 2016 and 2017. The portal Lending Club alone reported to have funded loans worth USD 31 billion by the end of 2017. The other market segments are considerably smaller and are comparable in size. According to Massolution (2016), donation-based crowdfunding reached a global volume of USD 2.85 billion, reward-based crowdfunding USD 2.68 billion, and crowdinvesting USD 2.50 billion in 2015. New segments such as royalty-based crowdfunding, hybrid forms of crowdfunding, and token presales or Initial Coin Offerings exhibit relatively small market volumes (Fig. 1.1).

Fig. 1.1

Global crowdfunding market by segment volume, USD billions in 2015

Depending on the jurisdiction under which platforms are operating, their business models often cut out traditional financial intermediaries. On the upside, this might reduce transaction costs and make financial services more cost-efficient. Furthermore, crowdlending portals may be well equipped to develop credit risk models that are geared to high-risk loans. They may thus provide a better assessment of high-risk customers than traditional financial intermediaries that used to refuse certain individuals and businesses access to mainstream financial services. Put differently, crowdfunding portals have identified the inability of traditional banks to extend loans as a business opportunity and consequently seek to fill the existing funding gaps. At the same time, many crowdfunding markets lack financial intermediaries that screen and monitor borrowers. Portals have regularly no skin in the game and consequently have little incentives to consider the performance of their investors. Under the new US crowdinvesting rules, the funding portals and their directors are even prohibited to have any financial interest in the issuer. From a macroeconomic and systemic risk perspective, this might be a desirable setting, as no crowdfunding platform can become too big to fail.

Moreover, all crowdfunding platforms cater per definition to two-sided markets. This means that platforms need not only attract borrowers, start-ups, or charity beneficiaries but also individuals who are willing to donate or put their money into a risky investment. Thus, if platforms intend to operate in the market over a considerable period of time, they should, in line with Rochet and Tirole (2003), have good incentives to serve the interest of all market participants including the investors. Whether the owners and managers of a crowdfunding platform intend to operate a long-term business or rather engage in fly-by-night operations is ultimately an empirical question. However, some caution is warranted. Over the course of one and a half years, the Chinese crowdlending platform Ezubao, for example, had attracted a total of USD 7.6 billion from around 900,000 investors. In January 2016, it became obvious that the portal operated a Ponzi scheme and senior executives had spent considerable amounts of investors’ money on private expenses, making very little real investments.

Platforms are not the only market players that engage in fraud. Several project creators in reward-based crowdfunding have been identified as being scams (Cumming et al. 2016). For example, the Kobe beef jerky campaign was just about being completed, when Kickstarter stopped the USD 120,309 going to the fraudsters’ bank account. Whether the crowd is well positioned to identify scams is not clear. Mollick and Nanda (2015) find, for a sample of theater projects, that the financing decisions of the crowd and professional funders are quite consistent and that there is no difference in the quality of projects that receive funding by the crowd and those funded by professionals. On the other hand, crowdfunding platforms lack some of the features that Surowiecki (2004) identified as being important for the ‘wisdom of the crowd’ to emerge. Although the crowd might be a diversified enough group to distinguish valuable projects and scams, the decision-making process of backers and investors on the various Internet platforms is hardly independent and might also be driven be irrational herding. Some early contributions from the crowdlending realm indicate that investors can, however, also engage in strategic and rational herding (Herzenstein et al. 2011a).

If operations did not already fall under existing securities or banking laws, policy makers have so far taken a wait-and-see approach or implemented a light form of regulation that is to be adapted once regulators have learned more about the functioning of crowdfunding markets. The reason for the reluctant approach of many regulators is that they also understand the potential of serving underbanked individuals and small businesses that are at the core of economic growth. Large groups of the population might for the first time receive funding that was not available to them but should have been from an economic efficiency standpoint. Furthermore, crowdfunding also has a democratizing element in the sense that investors get access to a new asset class that was not available to them before.

In recent years, the academic literature has also shown a growing interest in crowdfunding. Some segments have received attention earlier than others, which was mostly due to data availability and the relevance of the respective crowdfunding segments. As noted in the Preface of this book, crowdfunding consists of four different business models. The funding of philanthropic and research projects is known as the donation-based crowdfunding model, where backers donate money to a project without subsequently receiving a monetary compensation. Still, backers may derive utility from the act of donation, for which Andreoni (1989) coined the term warm-glow effect. In an early study, Saxton and Wang (2014) analyzed data from Facebook Causes. They evidence that in the Internet traditional economic explanations are less important for charity-giving decisions than social network effect explanations are. Moreover, they revealed that health-related causes were most appealing to donors. Crowdfunding platforms that return donations in the event of not meeting capital goals tend to lead to larger contributions in total according to simulations (Wash and Solomon 2014) and empirical evidence (Cumming et al. 2015). Further, donors often invest very early or very late in crowdfunding and projects are more likely to be completely funded if donors invest early (Solomon et al. 2015).

Under the reward-based crowdfunding model, backers are promised a product or a perk. In a seminal article, Mollick (2014) examined the delivery rate in reward-based crowdfunding campaigns. Using data from Kickstarter, he found that most project creators intend delivering the product they promised, but many deliver it with a considerable delay. Crowdinvesting, which is also referred to as investment-based crowdfunding, securities crowdfunding, or equity crowdfunding, is an Internet-based form of external finance for firms. Solicitation of investors often takes place without or with a ‘light’ version of a securities prospectus. Investors participate in the uncertain future cash flows of a firm via equity, mezzanine, or debt finance. In one of the first articles on the topic, Ahlers et al. (2015) examine the effectiveness of signals that start-ups use to induce investors. They find that retaining equity and providing more detailed information about...

Table of contents

Cover

Front Matter

1. Introduction

Part I. Startups

Part II. Market Structure

Part III. Backers and Investors

Part IV. Recent Regulatory Efforts

Back Matter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Economics of Crowdfunding by Douglas Cumming, Lars Hornuf, Douglas Cumming,Lars Hornuf in PDF and/or ePUB format, as well as other popular books in Business & Corporate Finance. We have over 1.5 million books available in our catalogue for you to explore.