Explains U.S. QI and FATCA regulations in ways that allow financial institutions to understand their compliance obligations and take practical steps to meet them

Builds on the basic framework of the QI and FATCA and provides updates over the last 5 years

Includes two new chapters on AEoI/CRS and BEPS

?

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

In this chapter, I will look at the overarching principles of Code Chapter 3. Later chapters will deal with the granular aspects of meeting these regulatory obligations.

Part of the need to understand the principles first is that many of these principles have more than one way of being implemented in practice. While the system is very much ‘rules’ based, it cannot and does not take into account every possible permutation of entity type, account structure and so on. Regulators are also, by their very nature, always in catch-up mode to what happens ‘out on the street’. So, while the principle may say one thing, it’s often the case that the way in which the investment chain is structured either precludes that principle or provides several different ways for it to occur.

IRC Chapter 3 is essentially a way to codify a generalised relief at source taxation system so that US-sourced income (e.g. dividends or bond interest) paid to recipients outside the US can be distributed net of tax withheld at the correct rate.

There are several tax rates that apply to these kinds of income, including—0%, 10%, 15%, 20%, 25%, 30% and 39.4%. The ‘correct’ rate will depend on the nature of the paying instrument, the legal form and residence of the ultimate beneficial owner, the existence or otherwise of a double tax treaty, and to some extent the nature, location and status of any intervening financial intermediaries and the type of accounts they hold with upstream and downstream counterparties in the payment chain.

In order to achieve this relief at source, IRC Chapter 3 lays down rules by which non-US financial institutions, those usually closest to the beneficial owner recipient, can properly identify and communicate those tax entitlements to those who need to withhold the tax. As with any system of regulation, the IRC Chapter also includes both oversight mechanisms and enforcementpenalties to ensure that foreign financial firms are complying with the rules and not allowing those with no entitlements to gain them.

Key Principles

Relief at Source

Most tax jurisdictions fall into one or more of four categories:

1.

relief at source;

2.

quick refund;

3.

standard (post pay date) refund;

4.

a combination of (1), (2) and (3).

In a relief at source only jurisdiction, failure to provide adequate evidence of treatyentitlement or exemption prior to pay date leaves the beneficial owner with no ‘post pay date’ procedure to apply. There may be a quick refund process available on occasion, for example, France, where an appointed agent remits tax to its tax authority once a month—so claims for relief at source that failed the pay date deadlines can still be filed as long as the claim is received before the agent remits the tax to the tax authority.

Equally, in a standard refund-only jurisdiction, there is no pre-pay date procedure by which a beneficial owner can access the correct rate of tax on the pay date. Clearly combination jurisdictions offer the best solution with multiple processes—relief at source available to those who can provide the evidence prior to pay date, a quick refund process or, finally, a standard refund process for those who can’t.

There are many reasons why a beneficial owner may have a treatyentitlement but be unable to access tax relief processes. This establishes the important difference between having an entitlement and realising that entitlement.

Having an entitlement is based on certain known factors—owning securities on record date, tax residency, legal form and existence of a double tax treaty. While there may be some associated interpretive issues, generally, having an entitlement is a fixed thing. If you meet the criteria, you have an entitlement.

Realising an entitlement, on the other hand, requires that there be a process or mechanism acceptable to a tax authority and implemented usually by either the tax authority or a financial institution authorised by it. Some tax authorities make these processes very simple, while some make them very complex in terms of what documentation is required to substantiate an entitlement.

Of course, unless legally challenged, for example, under EU anti-discrimination laws, the final arbiter of whether any given beneficial owner is entitled to relief is the tax authority of the source country—the country where the income originated. However, given the very large numbers of beneficial owners involved, most tax authorities have moved from assessing these documents themselves to using the financial services infrastructure to perform this task for them. This allows them to reduce their workload and costs by pushing the assessment to the financial institutions, using regulation to generate the rules under which this happens. This raises important issues for the financial services industry, particularly where interpretation of the treaties is not clear, since, in most cases, tax authorities will hold the financial intermediary financially and strictly liable if it applies the wrong withholding tax on pay date.

Rules-Based Regulation

The US is technically a combination jurisdiction that permits both relief at source and standard (post pay date) refunds. That said, the Internal Revenue Service (IRS) requirements make it almost impossible for beneficial owners to successfully file standard refunds.

There is a kind of quick refund system in the US but it can only be operated by qualified intermediaries (QIs) via a refund, set-off or reimbursement process built into the QI Agreement.

The concepts that underpin relief at source are:

1.

‘Qualified Intermediary’ (QI) status by means of a contractual relationship with non-US financial intermediaries to undertake withholding obligations in return for less onerous reporting;

2.

Approval of a jurisdiction’s Know-Your-Customer (KYC) rules as a pre-requisite to enabling financial institutions to apply for Qualified Intermediary status;

3.

Documentation of account holders using US self-certifications or use of documentary evidence (KYC/Anti-Money Laundering [AML]), or both, to establish legal form, residency, eligibility for tax rate and any applicable penalties;

4.

Deposits of withheld tax to US Treasury;

5.

Full disclosure of all beneficial owners by non-qualified intermediaries (NQIs);

6.

Tax Information Reporting on an annual cascade basis including:

(a)

Limited disclosure and pooled reporting for QIs

(b)

Full disclosure and beneficial owner level reporting for NQIs

7.

Oversight through triennial Periodic Review and certification of effective internal controls by an appointed Responsible Officer;

8.

Enforcement through the application of penalties for compliance failures including late returns, inaccurate returns and under- or over-withholding.

The impact of each of these principles will be discussed in detail in the following chapters. However, in summary:

1.

Non-US financial institutions become unpaid tax collectors and report filers on behalf of the IRS;

2.

QIs sign up to a six-year, non-negotiable, unilaterally changeable (by IRS) contract under which they agree to:

(a)

Know the IRC Chapter 3 status of their account holders using documentary evidence (KYC/AML), documentation (forms W-8 or W-9), ‘reason to know’, ‘actual knowledge’ rules or, in the absence of these, ‘presumption rules’;

(b)

Appoint a Responsible Officer who must implement a written compliance programme, have sufficient authority to make changes in the business to meet the QI Agreement obligations;

(c)

Submit to two certifications within each six-year contract cycle unless they fall within the rules for waivers;

(d)

Make deposits of tax to US Treasury if they elect to be withholding QIs or instruct a US withholding agent (USWA) bank to make such deposits if they do not so elect;

(e)

Be liable for any under- and/or over-withholding plus penalties and interest.

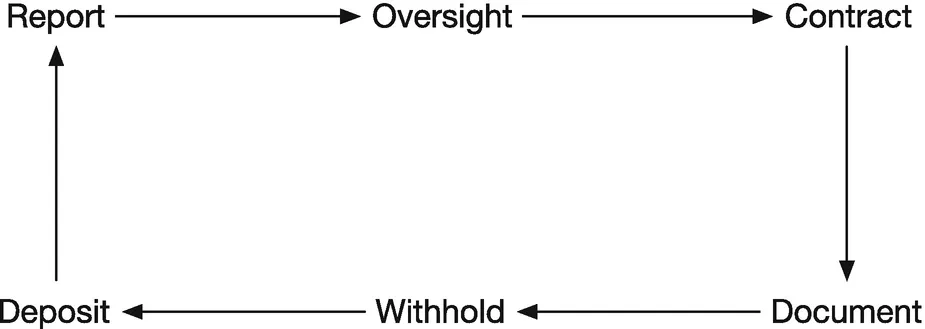

The overall process is described in Fig. 1.1.

Fig. 1.1

IRC Chapter 3 processes. Source: Author’s own

NQIs, who hold their status either by reason of being ineligible for QI status or by choosing not to, can still access tax relief at source on payments made to them, but only subject to full disclosure of their customers to another financial institution which is either a QI or a US withholding agent. NQIs are also subject to the reporting and enforcement elements of the regulations, but they don’t get the special treatment afforded to QIs. Hence their reporting to the IRS is at the beneficial owner level, not pooled. In other words, for NQIs receiving US-sourced income, all beneficial owners must be disclosed either to another intermediary (in order to get tax relief) or to the IRS (to meet reporting obligations).

As mentioned briefly in the introduction, the trigger for bei...

Table of contents

Cover

Front Matter

Part I. The QI Regulations

Part II. FATCA

Part III. Related Global Tax Initiatives

Back Matter

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access US Withholding Tax by Ross McGill in PDF and/or ePUB format, as well as other popular books in Business & Accounting. We have over 1.5 million books available in our catalogue for you to explore.