In The Hypocritical Hegemon, Lukas Hakelberg takes a close look at how US domestic politics affects and determines the course of global tax policy. Through an examination of recent international efforts to crack down on offshore tax havens and the role the United States has played, Hakelberg uncovers how a seemingly innocuous technical addition to US law has had enormous impact around the world, particularly for individuals and corporations aiming to avoid and evade taxation.

Through bullying and using its overwhelming political power, writes Hakelberg, the United States has imposed rules on the rest of the world while exempting domestic banks for the same reporting requirements. It can do so because no other government wields control over such huge financial and consumer markets. This power imbalance is at the heart of The Hypocritical Hegemon.

Thanks to generous funding from COFFERS EU, the ebook editions of this book are available as Open Access volumes from Cornell Open (cornellpress.cornell.edu/cornell-open) and other repositories.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

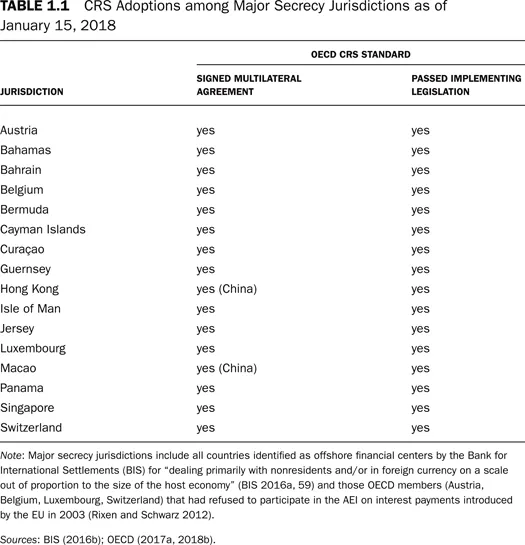

On October 29, 2014, fifty-one governments gathered in Berlin to abolish bank secrecy. At the seventh meeting of the Global Forum on Transparency and Exchange of Information for Tax Purposes (Global Forum), they signed a multilateral agreement committing signatories to automatically inform one another of bank accounts held by their respective citizens and other local residents. Since then, an additional fifty governments have joined the agreement, including all jurisdictions that have traditionally figured on tax haven blacklists for refusing to grant administrative assistance to foreign tax authorities (see table 1.1). Since 2018, these governments have been bound by contract to implement a common reporting standard (CRS) developed by the Organisation for Economic Co-operation and Development (OECD). The CRS obliges governments to adopt rules requiring financial institutions to regularly report all capital income held by nonresident individuals and entities, as well as their account balances. In addition, domestic banks need to look through interposed trusts or shell companies when determining the beneficial owner of a new account, and also have to review ownership data for existing accounts containing more than $250,000. Global Forum members will monitor every signatory’s CRS implementation in regular peer reviews and publish corresponding country reports (OECD 2014e, 2014g).

For countries formally known for their financial secrecy, the adoption of the CRS was a fundamental regulatory change. In order to comply, they had to dismantle secrecy laws, which had previously prevented the automatic reporting of client information from banks to tax authorities. The affected countries had defended such legal provisions for decades, and some had even given these provisions constitutional status. Switzerland, for instance, upgraded the breach of bank secrecy from civil to criminal offense when the French government raided the Paris offices of several Swiss banks in 1932 and refused any judicial cooperation on that basis (Guex 2000). Likewise, Austria added a provision to its constitution according to which parliament could change the bank secrecy law only with a two-thirds majority shortly before the country submitted its application for European Union (EU) membership in 1989. This should protect the secrecy provisions against requests for cooperation in tax matters (Bundesministerium für Finanzen 1988). Indeed, when the EU introduced the automatic exchange of information (AEI) on interest payments, Austria and Luxembourg were granted a temporary opt-out because of their bank secrecy laws. When the remaining member states attempted to end the opt-out, the two countries exploited the unanimity requirement for EU decisions on taxation to veto a corresponding directive six times in a row between 2009 and 2012 (Hakelberg 2015a).

Their governments’ success in defending bank secrecy at the international level enabled Austrian, Luxembourgian, and Swiss banks to boost their business with foreign clients. During the first decade of the twenty-first century, Swiss financial institutions managed almost half of the world’s households’ offshore financial wealth, amounting to $2 trillion or 9 percent of global gross domestic product (GDP) (Zucman 2013, 33). At the same time, Austrian and Luxembourgian banks were the largest recipients of cross-border deposits from households residing in other Eurozone countries. In 2010, Luxembourg reported €20 billion, Austria €9 billion, and Germany—the EU’s largest economy—merely €8 billion in bank deposits from the remaining member states of the currency union (Hakelberg 2015b, 411). This influx of foreign capital led to impressive growth rates in the financial sectors of the recipient countries but also made them highly dependent on investment from nonresidents. For instance, foreign financial wealth managed by Swiss banks equaled three times the amount of domestic wealth in 2007 (Zucman 2013, online appendix). Yet this influx was essentially driven by the promise of confidentiality, which foreign investors could exploit for tax evasion purposes among other things.1 The latest research suggests that 80 percent of the portfolios held by Scandinavian clients with the Swiss branch of HSBC had not been declared to tax authorities by their owners during the 2000s (Alstadsæter, Johannesen, and Zucman 2017b). Likewise, US Senate investigations revealed that 90 percent of the accounts held by US clients with Union Bank of Switzerland (UBS) and Credit Suisse over the same time period had not been declared to the Internal Revenue Service (IRS) (Levin and Coleman 2008; Levin and McCain 2014). Still, the Austrian, Luxembourgian, and Swiss governments ended up conceding their financial sectors’ key competitive advantage by adopting the CRS.

In addition to the economic costs, this decision also came with important political costs. For citizens in financially discreet countries, bank secrecy and its defense had often become part of their national identity. Many Austrians, for instance, believed in a narrative according to which bank secrecy had been introduced to restore trust in the country’s financial system and regularize black market activity after World War II. A high level of privacy, so the story goes, should motivate Austrians to entrust their savings to local banks instead of hiding money in their mattresses.2 As citizens became increasingly accustomed to the inability of the state to gather information on their accounts, bank secrecy attained the status of a “holy cow” in Austrian politics. No party dared to touch it for fear of the electoral consequences.3 Likewise, many Swiss were proud of their bank secrecy law, which they wrongly believed was introduced to protect the assets of German Jews persecuted by the Nazis.4 Policymakers exploited these narratives, despite their shaky empirical foundations, to raise popular support for bank secrecy. In policymakers’ view, bank secrecy was a legitimate particularity rooted in historical circumstances that had nothing to do with the poaching of tax base from neighboring countries. In domestic politics, defending bank secrecy against outside pressure thus meant to preserve a national characteristic (Blocher 2006; Strache 2013). Nonetheless, the Austrian and Swiss governments expended considerable political capital to overcome domestic opposition to the CRS.

Given their previous defense of bank secrecy and the important economic and political costs linked to its abolition, why did tax havens eventually agree to automatically exchange account information with foreign governments? In this book, I argue that the end of bank secrecy in traditional secrecy jurisdictions is the result of coercion by the United States. On March 18, 2010, the US Congress passed the Obama administration’s second stimulus package after the financial crisis. Attached to this package was a little-noticed law that contained a credible threat of sanctions against secrecy jurisdictions: the Foreign Account Tax Compliance Act (FATCA). The act obliges foreign financial institutions to automatically report US clients and their capital income to the IRS. If a bank fails to comply, the agency is granted authority to withhold 30 percent of the payments this institution receives from US sources (Mollohan 2010). Since the United States controls the world’s largest financial market as well as central financial infrastructure like clearing houses and other interbank settlement systems, no foreign bank was willing to divest from the United States to circumvent the new reporting requirements. Instead, foreign banks began to lobby their home governments to abolish bank secrecy and other provisions preventing their compliance with FATCA (Emmenegger 2017; Grinberg 2012).

By dismantling the legal barriers to the dissemination of bank account information, however, secrecy jurisdictions also became vulnerable to information requests from third countries. Because of a most-favored-nation clause contained in an EU directive, Austria and Luxembourg were, for instance, legally obliged to exchange information with other EU member states after signing FATCA agreements with the US Treasury. Likewise, Switzerland could no longer fend off the EU’s request to participate in its AEI system after it had agreed to automatically report information on bank accounts held by US residents to the IRS. By making this concession, the Swiss government had ended its principled defense of bank secrecy. Hence, Switzerland’s traditional legal argument against the provision of administrative assistance to its European neighbors was no longer tenable. For financial institutions in Switzerland and other former secrecy jurisdictions, their governments’ decision to transmit account data to more than one foreign government created several challenges. If other secrecy jurisdictions did not accept the AEI, former secrecy jurisdictions could lose hidden capital to foreign competitors still providing secrecy benefits. If foreign governments requested different types of information, former secrecy jurisdictions’ compliance burden would increase. Therefore, traditional secrecy jurisdictions joined major developed economies in calling for a level regulatory playing field: that is, governments around the world should apply a single global AEI standard based on FATCA. Against this background, the OECD developed the CRS and the multilateral agreement for its implementation (see chapter 5).

Yet a fundamental limitation remains. After imposing the AEI on the rest of the world, the Obama administration eventually refused to reciprocate the reporting of account information under its bilateral FATCA treaties and did not sign the multilateral agreement binding governments to the CRS (cf. OECD 2018b; US Treasury 2012a). Consequently, US banks currently have to follow much weaker transparency standards than banks in other countries. For instance, US banks are still under no obligation to look through trusts when determining account ownership (cf. FinCEN 2016). Unlike in countries respecting the CRS, in the United States foreign account holders can thus remain anonymous when they put their financial wealth in trust. Accordingly, the number of corresponding contractual relationships registered in secretive US states such as Nevada or South Dakota has rapidly increased since the multilateral adoption of the CRS (Scannell and Houlder 2016). Likewise, the value of foreign deposits in US banks has grown substantially, whereas the traditional secrecy jurisdictions listed in table 1.1 have incurred important losses (Hakelberg and Schaub 2018). In fact, Casi, Spengel, and Stage (2018) show that deposits from the EU and other OECD countries in the United States grew by 9 percent between 2014—when traditional secrecy jurisdictions adopted the CRS—and 2017. Concomitantly, such deposits diminished by 14 percent on average in the group of formerly secretive countries they study, including Guernsey, Hong Kong, the Isle of Man, Jersey and Macau.

Although the United States may thus replace Switzerland as the most important secrecy jurisdiction for European investors, the EU, which matches US market power when acting in unison (see chapter 2), has not yet managed to wrestle full reciprocity from the Obama and Trump administrations. The reason is that member states, which found consensus on AEI within the EU, still disagree on including the United States in their blacklist of tax havens facing collective sanctions (cf. Council of the European Union 2017; European Commission 2016e). Because of the unanimity requirement in tax matters discussed earlier, the veto of a single government is enough to prevent this decision, and several export-dependent member states, including Germany, fear an inclusion of the United States could provoke retaliatory measures in the trade arena.5 Since internal division has prevented the EU from checking their hypocrisy, successive US governments have thus been able to uphold a highly redistributive international AEI regime, inviting committed foreign tax evaders to shift their hidden financial wealth from traditional secrecy jurisdictions into the United States. While Austrian tax advisers have, in response, deplored a loss of business to US competition,6 one of their American colleagues rebuffed European criticism of FATCA’s lack of reciprocity simply by stating that “fair is what you can get away with, and the United States has the power to defend this outcome.”7

Coercion Transcends Structural and Normative Constraints

The unexpected end of bank secrecy in traditional secrecy jurisdictions reflects the ability of a great power like the United States to unilaterally effect fundamental change in international tax policy through coercion. This interpretation stands in sharp contrast to the two established narratives to international tax policy: the contractualist and the constructivist perspective. From the contractualist perspective, an international agreement must be based on the common interest of the signatory states. Otherwise, disadvantaged governments will either refuse to cooperate or defect from the agreement (Dehejia and Genschel 1999; Rixen 2008). If this approach were still correct, tax havens would expect joint gains from the multilateral AEI and participate voluntarily. From the constructivist perspective, shared regulative norms, including the respect for national sovereignty, have traditionally prevented powerful governments from forcing tax havens to remove domestic legal hurdles to the dissemination of account information (Webb 2004; Sharman 2006b). If this reading continued to apply, the US sanctions threat contained in FATCA should have been preceded by normative change legitimizing the use of coercion against tax havens. To exclude the possibilities that tax havens’ participation in the multilateral AEI results from voluntary consent or normative change instead of coercion, I will thus show two things in this section. First, the structural constraints precluding a common interest in countermeasures to tax evasion were still in place when the US Congress passed FATCA. Second, there was no need for normative change, because regulative norms have never consistently prevented the US from interfering with the legal systems of tax havens.

Structural Constraints to Cooperation from Tax Havens

The contractualist narrative of international tax policy identifies two structural constraints preventing governments from reaching agreement on countermeasures to tax evasion: an asymmetric prisoner’s dilemma and a weakest-link problem. The asymmetric prisoner’s dilemma results from the uneven distribution of benefits from tax competition between small and large countries. Relative to their small domestic capital stock, small countries can attract a lot of foreign capital with a tax cut. Hence, they can compensate for tax revenue lost to a lower tax rate with tax revenue generated from a broader tax base. In contrast, large countries can—relative to their large domestic capital stock—only attract a small amount of foreign capital with a tax cut. As large countries find it more difficult to compensate for a lower tax rate with a broader tax base, they lose the tax competition for capital to small countries. Accordingly, large countries have an interest in international tax coordination, whereas small countries prefer tax competition (Genschel and Schwarz 2011; Wilson 1999). Since most governments assert a right to tax the worldwide income of individuals resident within the government’s territory, however, the crucial prerequisite for the competitiveness of small tax haven countries is secrecy. The low tax rates they offer apply only if the taxable capital income of a foreign account-holder remains hidden from the tax authorities in her country of residence.

Whereas the asymmetric prisoner’s dilemma results from interest heterogeneity between small and large countries, the weakest-link problem prevents large countries from changing the preferences of small countries through side payments. Since small countries gain less revenue from tax competition than large countries lose, because of the small countries’ lower rates, at first sight there seems to remain scope for a mutually beneficial agreement, in which large countries compensate small countries for refraining from tax competition. For the agreement to be effective, however, all of the world’s tax havens would have to participate. Otherwise, tax evaders seeking low rates and secrecy could simply transfer their financial wealth to the remaining uncooperative jurisdictions. If large countries offered a compensatory deal, tax havens would thus have an incentive to drag their feet. The longer they stay out of an expanding coalition of cooperating governments, the more they benefit from reduced competition in the tax haven market, and the more expensive their compensation becomes for large countries (Elsayyad and Konrad 2012). From the contractualist perspective, the expectation of an exponential rise in enforcement costs, sometimes created by cautionary tales of capital flight disseminated by the financial industry, causes otherwise powerful governments of large countries to shy away from initiatives against tax evasion (Dehejia and Genschel 1999; Rixen 2013).

If the asymmetric prisoner’s dilemma and weakest-link problem had somehow disappeared before the United States issued a credible threat of sanctions through FATCA, enabling secrecy jurisdictions to voluntarily agree to the AEI, we would thus have to observe at least one of three things: (1) a reduction in the benefit secrecy jurisdictions reap from abetting tax evasion reflected in an outflow of foreign financial wealth or a shrinking contribution of financial services to a tax haven’s overall economic performance; (2) a decrease in the importance foreign depositors in secrecy jurisdictions attach to financial secrecy, removing the link between information reporting and capital flight; or (3) an offer of side payments from large countries to secrecy jurisdictions despite the high expected cost of these payments.

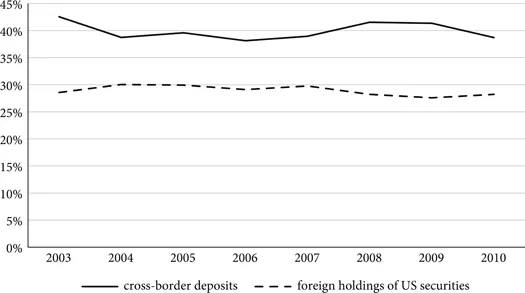

FIGURE 1.1.Foreign Financial Wealth in Secrecy Jurisdictions before FATCA (Percentage of Total)

Note: Cross-border deposits reflect deposit liabilities of banks in the respective reporting country to all foreign households and nonfinancial corporations. Foreign holdings of US securities include all forms of equity and all debt securities issued in the United States and held or manage...

Table of contents

List of Illustrations

Note on Terms

Preface

Acknowledgments

1. Change and Stability in Global Tax Policy

2. Power in International Tax Politics

3. Countering Harmful Tax Practices

4. The Swift Return of Tax Competition

5. The Emergence of Multilateral AEI

6. The BEPS Project

7. From Hegemony to Transatlantic Tax Battle?

Notes

References

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Hypocritical Hegemon by Lukas P. Hakelberg in PDF and/or ePUB format, as well as other popular books in Economics & Taxation. We have over 1.5 million books available in our catalogue for you to explore.