Named the 2019 Investment and Retirement Planning "Book of the Year" by the Institute for Financial Literacy

It's never too late to start planning for retirement

You Don't Have to Drive an Uber in Retirement is a survival guide for your golden years, and a lifeline for those entering the Retirement Crisis unprepared. Roughly 45 percent of Americans have zero dollars saved for retirement—but the average retiree will spend $154,000 in out-of-pocket health care costs alone. We need to figure out how to generate more income, even in retirement, and spend less. How do we boost our retirement income? Is investing the way to go? How much do we need, anyway? This book does more than just answer the important questions—it gives you real-world tips to help you reach your financial goals. Yes, it is possible to increase your income in or as you approach retirement. These guidelines will help you optimize your assets and put away more money for the years you'll need it most.

Planning for retirement does not mean holding off on fun today; there are many ways the average American can reduce everyday costs of living without living like a pauper. This book will help you take stock of what you have and what you'll need, and show you how to bridge the gap.

Maximize your savings while minimizing the lifestyle impact

Unique ways for generating a meaningful amount of income, that don't require you to get a job

Learn just how much you'll need for a comfortable retirement

Adopt new everyday strategies that will help you bolster your funds

Add new income streams, optimize your portfolio, and learn to spend less without living less—these are the key factors in making your golden years truly golden. You Don't Have to Drive an Uber in Retirement is an important resource and insightful guide for those hoping to one day leave the workforce—in comfort.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

This first section of You Don't Have to Drive an Uber in Retirement will show you different ways of creating new income streams.

Several will require some work but are lucrative. And you may have fun doing them.

But none require you to change your lifestyle or to put in hours when you don't want to. I'm not recommending that you get a job where you're expected to show up at a certain time on a certain day.

If any of the ideas in this section appeal to you, do them when you feel like it. If you'd rather play golf or take a snooze, no worries. These opportunities will be there tomorrow.

Of course, the more you put into these ideas, the more you'll get out of them. And I expect that you'll find these moneymaking recommendations enjoyable enough that you'll want to do several of them, especially once the register starts ringing.

But again, this book is all about maintaining your lifestyle, not drastically changing it (unless you want to).

By taking some of the actions in this section, you'll regain control over your retirement and not be as dependent on a government or corporate promise.

Having some income will relieve stress and ensure that you have enough money both to cover your bills and pay for some extras.

Let's start making money.

CHAPTER 1 Give Yourself a Raise

“The two most powerful warriors are patience and time.”

– Leo Tolstoy

There are few feelings as satisfying as getting a raise. It's great to know that you're going to make more money this year than you did last year.

My first job out of college, I was paid the princely figure of $22,500 a year. I performed well in my position and when I met with my boss for my review, I was given a 5% raise to $23,625. The maximum I could have received was 6%, but I was told nobody ever gets that. (I never understood that line of thinking, but that's another issue.)

I was living in Manhattan with two roommates and barely getting by. I had a girlfriend who had expensive tastes and little income. Now, that extra $21.62 (before taxes) per week wasn't going to keep her in the lifestyle she expected to become accustomed to, but it was a little more breathing room. Not much, but a little more.

Importantly, it gave me a feeling of pride in not just knowing that my company felt I was valuable (although apparently not 6% more valuable), but that I was progressing financially.

Now that I'm older and wiser, I have set up my portfolio so that I get a big fat raise every year – bigger than the 6% that eluded me when I was just starting out.

The way I do that is with Perpetual Dividend Raisers. This is my favorite strategy for income and wealth creation whether you're in retirement already or are still working.

I not only want to see the portfolio balance moving higher, but the amount of income that is generated each year should climb too.

In retirement, that's not just a matter of convenience or pride. It may be the difference between going to a restaurant once or twice a week and eating ramen noodles.

As I outlined in the introduction, Social Security may not be there, so income from your investments will be a critical part of keeping you afloat. Even if you receive Social Security, the average monthly Social Security check of $1,3411 doesn't exactly enable you to take the grandkids to Disney or play too many rounds of golf.

And don't think just because you have a nest egg, you're all set. One medical emergency can drain that pretty quickly.

Medical emergencies are just that, sudden, unexpected and frequently ill-timed. Shortly after he retired, my friend's father came down with a serious but treatable illness. However, his medication costs $52,260 per year out of pocket.

As I mentioned in the introduction, if you're 65 or under, you'll likely spend somewhere between a quarter of a million and half a million dollars on healthcare in the next several decades.

And those costs rise sharply every year. Until the Great Recession in 2008, healthcare costs consistently increased at least 6% per year. Since 2008, those numbers have slowed a bit, though they are still well above the inflation rate.

In 2014, healthcare costs climbed 3.4% while the consumer price index inched up 0.8%. But, by the time you read this book. the growth in cost is expected to get back to the historical 6% average.2

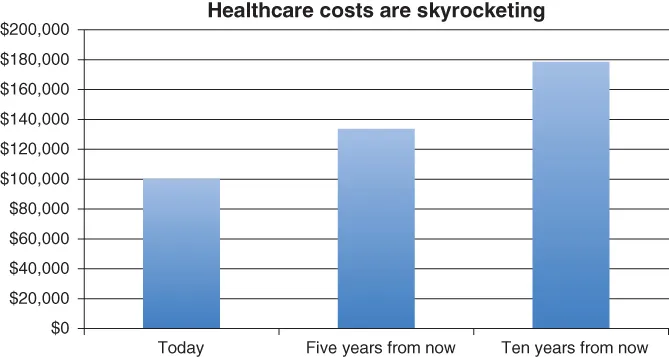

That means whatever you have stashed away in the bank or in an annuity is going to be worth less five years from now than it is today. Ten years from now you'll hardly recognize the buying power of your retirement accounts.

If healthcare returns to its 6% inflation rate, your nest egg will be worth one-third less in five years than it is today in healthcare dollars. In other words, what costs $100,000 today will cost $133,822 five years from now.

In ten years, you'll need nearly double what you have today to buy the same healthcare goods and services. What costs $100,000 today will run you $179,084 a decade from now.

And that's just healthcare costs. That doesn't include fun things like nursing homes. It is expected that at least 40% of seniors will require nursing home care. And many others will have live-in help. Those things aren't cheap.

So it's not enough to just have a nice stash of cash. That money or, better yet, the income it spins off need to grow each year so you're dipping as little as possible into the nest egg.

Keep in mind, the less money you have, the less income it will likely generate.

It's critically important that you not only have a solid base, but that the money generates income that goes up every year. If your income grows enough, you'll actually increase your buying power, rather than just making sure you can keep up with the rising doctors' bills.

There a...

Table of contents

Cover

Title Page

Table of Contents

Foreword

Introduction

PART I: Generating Income

PART II: Cutting Costs

PART III: Small Ideas That Add Up

PART IV: Ideas I Don't Like

Conclusion

About the Author

Acknowledgments

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access You Don't Have to Drive an Uber in Retirement by Marc Lichtenfeld in PDF and/or ePUB format, as well as other popular books in Negocios y empresa & Finanzas. We have over 1.5 million books available in our catalogue for you to explore.