McKinsey & Company's #1 best-selling guide to corporate valuation, now in its sixth edition

Valuation is the single best guide of its kind, helping financial professionals worldwide excel at measuring, managing, and maximizing shareholder and company value. This new sixth edition provides insights on the strategic advantages of value-based management, complete detailed instruction, and nuances managers should know about valuation and valuation techniques as applied to different industries, emerging markets, and other special situations.

Valuation lies at the crossroads of corporate strategy and finance. In today's economy, it has become an essential role — and one that requires excellence at all points. This guide shows you everything you need to know, and gives you the understanding you need to be effective.

Estimate the value of business strategies to drive better decision making

Understand which business units a corporate parent is best positioned to own

Assess major transactions, including acquisitions, divestitures, and restructurings

Design a capital structure that supports strategy and minimizes risk

As the valuation function becomes ever more central to long- and short-term strategy, analysts and managers need an authoritative reference to turn to for answers to challenging situations. Valuation stands ahead of the field for its reputation, quality, and prestige, putting the solutions you need right at your fingertips.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

The guiding principle of business value creation is a refreshingly simple construct: companies that grow and earn a return on capital that exceeds their cost of capital create value. Articulated as early as 1890 by Alfred Marshall,1 the concept has stood the test of time. Indeed, when managers, boards of directors, and investors have forgotten it, the consequences have been disastrous. The financial crisis of 2007–2008 and the Great Recession that followed provide the most recent evidence of the point. But a host of other calamities, from the rise and fall of business conglomerates in the 1970s to the collapse of Japan's economy in the 1990s to the Internet bubble, can all to some extent be traced to a misunderstanding or misapplication of this guiding principle.

Today these accumulated crises have led many to call into question the foundations of shareholder-oriented capitalism. Confidence in business has tumbled.2 Politicians and commentators push for more regulation and fundamental changes in corporate governance. Academics and even some business leaders have called for companies to change their focus from increasing shareholder value to a broader focus on all stakeholders, including customers, employees, suppliers, and local communities. At the extremes, some have gone so far as to argue that companies should bear the responsibility of promoting healthier eating and other social issues.

Many of these impulses are naive. There is no question that the complexity of managing the coalescing and colliding interests of myriad owners and stakeholders in a modern corporation demands that any reform discussion begin with a large dose of humility and tolerance for ambiguity in defining the purpose of business. But we believe the current debate has muddied a fundamental truth: creating shareholder value is not the same as maximizing short-term profits. Companies that confuse the two often put both shareholder value and stakeholder interests at risk. Indeed, a system focused on creating shareholder value isn't the problem; short-termism is. Banks that confused the two at the end of the last decade precipitated a financial crisis that ultimately destroyed billions of dollars of shareholder value, as did Enron and WorldCom at the turn of this century. Companies whose short-term focus leads to environmental disasters also destroy shareholder value, not just directly through cleanup costs and fines, but via lingering reputational damage. The best managers don't skimp on safety, don't make value-destroying decisions just because their peers are doing so, and don't use accounting or financial gimmicks to boost short-term profits, because ultimately such moves undermine intrinsic value that is important to shareholders and stakeholders alike.

What Does It Mean to Create Shareholder Value?

At this time of reflection on the virtues and vices of capitalism, we believe that it's critical that managers and boards of directors have a new, precise definition of shareholder value creation to guide them, rather than having their focus blurred by a vague stakeholder agenda. For today's value-minded executives, creating shareholder value cannot be limited to simply maximizing today's share price for today's shareholders. Rather, the evidence points to a better objective: maximizing a company's collective value to current and future shareholders, not just today's.

If investors knew as much about a company as its managers do, maximizing its current share price might be equivalent to maximizing value over time. But in the real world, investors have only a company's published financial results and their own assessment of the quality and integrity of its management team. For large companies, it's difficult even for insiders to know how financial results are generated. Investors in most companies don't know what's really going on inside a company or what decisions managers are making. They can't know, for example, whether the company is improving its margins by finding more efficient ways to work or by simply skimping on product development, maintenance, or marketing.

Since investors don't have complete information, it's easy for companies to pump up their share price in the short term. For example, from 1997 to 2003, a global consumer products company consistently generated annual growth in earnings per share (EPS) between 11 percent and 16 percent. Managers attributed the company's success to improved efficiency. Impressed, investors pushed the company's share price above those of its peers—unaware that the company was shortchanging its investment in product development and brand building to inflate short-term profits, even as revenue growth declined. In 2003, managers had to admit what they'd done. Not surprisingly, the company went through a painful period of rebuilding. Its stock price took years to recover.

This does not mean that the stock market is not “efficient” in the academic sense that it incorporates all public information. Markets do a great job with public information, but markets are not omniscient. Markets cannot price information they don't have. Think about the analogy of selling a house. The seller may know that the boiler makes a weird sound every once in a while or that some of the windows are a bit drafty. Unless the seller discloses those facts, it may be very difficult for a potential buyer to detect them, even with the help of a professional house inspector.

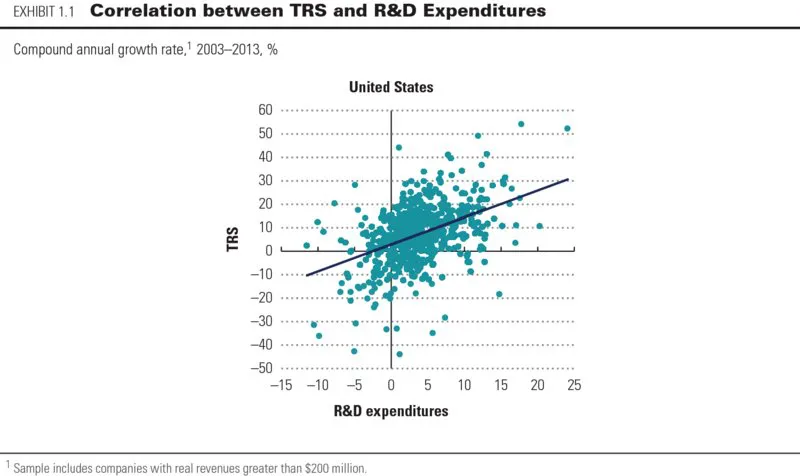

Despite such challenges, the evidence makes it clear that companies with a long strategic horizon create more value. The banks that had the insight and courage to forgo short-term profits during the last decade's real-estate bubble earned much better returns for shareholders over the longer term. Over the long term, oil and gas companies known for investing in safety outperform those that skimp on such investment. We've found, empirically, that long-term revenue growth—particularly organic revenue growth—is the most important driver of shareholder returns for companies with high returns on capital.3 We've also found that investments in research and development (R&D) correlate powerfully with positive long-term total returns to shareholders (TRS), as graphed in Exhibit 1.1.4

Creating value for both current and future shareholders means managers should not take actions to increase today's share price if those actions will damage it down the road. Some obvious examples include shortchanging product development, reducing product quality, or skimping on safety. Less obvious examples are making investments that don't take into account likely future changes in regulation or consumer behavior (especially with regard to environmental and health issues). Faced with volatile markets, rapid executive turnover, and intense performance pressures, making long-term value-creating decisions can take courage. But it's management's and the board's task to demonstrate that courage, despite the short-term consequences, in the name of value creation for the collective benefit of all present and future shareholders.

Can Stakeholder Interests Be Reconciled?

Much recent criticism of shareholder-oriented capitalism has called on companies to focus on a broader set of stakeholders beyond just its shareholders. It's a view that has long been influential in continental Europe, where it is frequently embedded in corporate governance structures. And we agree that for most companies anywhere in the world, pursuing the creation of long-term shareholder value requires satisfying other stakeholders as well. You can't create long-term value without happy customers, suppliers, and employees.

We would go even further. We believe that companies dedicated to value creation are healthier and more robust—and that investing for sustainable growth also builds stronger economies, higher living standards, and more opportunities for individuals. Our research shows, for example, that many corporate social-responsibility initiatives also create shareholder value, and that managers should seek out such opportunities.5 For example, IBM's free Web-based resources on business management not only help to build small and midsize enterprises; they also improve IBM's reputation and relationships in new markets and develop relationships with potential customers.

Similarly, Novo Nordisk's “triple bottom line” philosophy of social responsibility, environmental soundness, and economic viability has led to programs to imp...

Appendix B: Derivation of Free Cash Flow, Weighted Average Cost of Capital, and Adjusted Present Value

Appendix C: Levering and Unlevering the Cost of Equity

Appendix D: Leverage and the Price-to-Earnings Multiple

Appendix E: Other Capital Structure Issues

Appendix F: Technical Issues in Estimating the Market Risk Premium

Index

Advert

EULA

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Valuation by Tim Koller,Marc Goedhart,David Wessels in PDF and/or ePUB format, as well as other popular books in Business & Investments & Securities. We have over 1.5 million books available in our catalogue for you to explore.