FinTech Innovation examines the rise of financial technology and its growing impact on the global banking industry. Wealth managers are standing at the epicenter of a tectonic shift, as the balance of power between offering and demand undergoes a dramatic upheaval. Regulators are pushing toward a 'constrained offering' norm while private clients and independent advisors demand a more proactive role; practitioners need examine this banking evolution in detail to understand the mechanisms at work. This book presents analysis of the current shift and offers clear insight into what happens when established economic interests collide with social transformation. Business models are changing in profound ways, and the impact reaches further than many expect; the democratization of banking is revolutionizing the wealth management industry toward more efficient and client-centric advisory processes, and keeping pace with these changes has become a survival skill for financial advisors around the world.

Social media, big data analytics and digital technology are disrupting the banking industry, which many have taken for granted as set in stone. This book shatters that assumption by illustrating the massive changes already underway, and provides thought leader insight into the changes yet to come.

Examine the depth and breadth of financial technology

Learn how regulations are driving changing business models

Discover why investors may become the price-makers

Understand the forces at work behind the rise of FinTech

Information asymmetry has dominated the banking industry for centuries, keeping the bank/investor liability neatly aligned—but this is changing, and understanding and preparing for the repercussions must be a top priority for wealth managers everywhere. Financial Innovation shows you where the bar is being re-set and gives you the insight you need to keep up.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Chapter 1 The Theory of Innovation: From Robo-Advisors to Goal Based Investing and Gamification

“People don't want to buy a quarter-inch drill. They want a quarter-inch hole.”

—Theodore Levitt (1925–2006)

This chapter sketches the main arguments of this book. The theory of innovation provides the framework that helps to explain why robo-technology (disruptive) and the gamification of Goal Based Investing (sustaining) sit together as key determinants of today's banking transformation. The search for personalization is the fil rouge that links the main elements of wealth management innovation. Industry decision-makers are therefore addressed with some useful action items, which allow them to tackle with clarity and rationality the challenges of robo-technology transformation.

1.1 Introduction

The history of banking is clearly the history of money, hence the history of trade which can be traced back as early as 12,500 b.c. to the usage by Anatolians of obsidian, a raw material used to build stone-age tools. But banking, as we know it today, is a more recent industry which was forged during the 12th century and early Italian Renaissance to facilitate commerce and manage personal finance for wealthy families in rich cities such as Florence, Venice, and Genoa; Monte dei Paschi di Siena being the oldest bank operating continuously since 1472. During the 17th and 18th centuries North European cities such as Amsterdam and London took the lead, fostering systemic innovations like central banking. Yet, only during the 20th century, and especially after the industry deregulation in the 1980s, which saw New York and London emerge as world leading financial centres, has financial innovation enabled banks to stretch their balance sheets and grow the level of international interdependence to the point of becoming a potential systemic threat to the stability of modern economies, as demonstrated by the unfolding of the Global Financial Crisis (GFC) in 2007.

Given the global scale of the banking industry, the interdependence between finance and technology has also grown steadily because information technology (IT) has facilitated the harnessing of economies of scale. For many decades banks have been front runners in IT spending. This has followed regulatory pressure to strengthen their fast growing operations, but also a need to compete and adapt to more efficient technology frameworks with the motto “invest more to save more”. Notwithstanding, today's digitalization shift has revealed that most banking systems are still obsolete and leave the industry exposed to unexpected competition: small FinTechs, financial technology companies, are imposing themselves against traditional models by using digital technology as a weapon to tear down the barriers of entry and potentially disrupt the whole industry.

Technology is not the only force in motion to transform financial services. Regulation is clearly the other major driver affecting existing business models, if not the leading force. Widespread criticism has hit established banking practices in the aftermath of the GFC, alerting international regulators to the importance of strengthening the rules of conduct of the intermediaries to protect the interests of individuals and the community of investors at large. Transparency, adequacy, and suitability have become the major leitmotifs for compliance officers. But most importantly, the ban on retrocessions and the required transparency about costs and fees, as well as the rise of personal financial advisors, have started to hinder established business models which seemed too rigid to embrace change. Existing incentive schemes based on product selection have become inconsistent with a global push towards added-value and fee-only investment services. This is clearly a threat to the sustainability of banks' balance sheets, because it severely impacts the sustainability of cost/income ratios. Banks are required to increase their IT spending to transform digitally, while intermediation margins are shrinking and economic capital has become scarce and very expensive. Yet, from a high-level perspective, such an increase in the cost of capital has pushed many institutions to reduce their investment banking and proprietary desks, and forced them to look at wealth management operations more strategically (Goldman Sachs being one of the few exceptions). This repositioning of banks' portfolios can be the opportunity to transform this ancient industry, and enable private investors to take centre stage in the investment process by starting from the eliciting of their ambitions and fears, hence by personalizing the investment process to their individual needs and abandoning the more generalist asset management point of view. This shift is a change of perspective from the analysis of market variables (e.g., expected return, variance, Sharpe ratios) towards client-centric representations of investment goals (e.g., probability of achieving targets), which goes under the name of Goal Based Investing. As a matter of fact, it is not surprising that most of the FinTechs operating in the domain of personal finance have adopted rudimentary GBI schemes to design their disruptive investment propositions: they anchor the investment dialogue to personal goals and time horizons that match individuals' personal traits.

“But are FinTechs truly disruptive? Is banking about to be unbundled? Would regulators favour this shift in the long term, or would they oppose it given considerations of financial stability?”

Disruption is effectively underway, though it might take the form of transforming existing firms more than putting them out of business by the rise of Robo-Advisors. However, not all firms may be able to transform, so that there will be winners and laggards, which may well be forced out of the game. Clearly, no future can be predicted for any industry, nor the fate of any individual company. But the theory of innovation can provide the mindset to explain the transformation at play by revising, and helping to understand, the most common reasons that lead companies (e.g., banks) to go out of business, no matter how dominant they were or how much skill their respective management possessed at the time of downsizing. The remainder of this chapter is dedicated to discussing what FinTechs do, dissecting the principles of innovation theory, and explaining why robo-technology, Goal Based Investing and Gamification directly relate the one to the others.

1.2 A Vibrant FinTech Ecosystem

FinTechs are start-up companies which appeared between 2008 and 2010 particularly in the US, not confined to Silicon Valley creative capabilities, but fast spreading out to the East Coast, Europe, Hong Kong, Singapore, Australia, and much of Asia. The FinTechs' ecosystem features a variety of business propositions which can span from peer-to-peer lending to digital payments or Big Data analytics. Yet, if we look at the business philosophy and aspirations of their founders, we can draft a quick and dirty definition that links their most common ambitions: digitalization, analytics, specialization, and long-tail consumers. We can therefore refer to them as follows:

“FinTechs are a global phenomenon, born at the intersection between financial firms and technology providers, attempting to leverage on digital technology and advanced analytics to unbundle financial services and harness economies of scale by targeting long-tail consumers.”

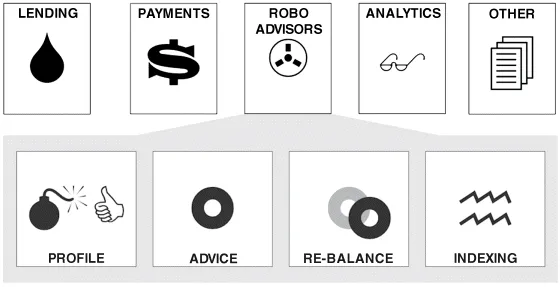

Clearly, digitalization plays a key role, because digital tools allow the creation of captive customer experiences as weapons to tear down the barriers to entry in financial services, hence fostering borderless competition against established institutions. Most of today's FinTechs make usage of analytics to generate competitive business propositions in terms of marketing, positioning, social media, and handling of Big Data. They feature a high level of specialization, hence very narrow and simple business propositions, to profit from a concerted attempt to unbundle financial services into leaner and specialized digital offers. Finally, they target directly or indirectly long-tail consumers to disintermediate established providers with cheaper services. Typically, they are Business to Consumer firms (B2C), but Business to Business (B2B) and Business to Business to Consumer (B2B2C) models are emerging to fill the void between starlight innovators and the need of financial institutions to transform fast. The FinTech parterre changes very fast and is populated by new firms and ideas almost every quarter. Hence, we refrain from commenting on individual cases: such an exercise of market intelligence would be the focus of research analysts, whose thorough work has also kindly inspired the drafting of this book and helped to navigate through the variety of species fighting for affirmation within this ecosystem. By and large, they can be classified as in Figure 1.1: retail lending, payments, analytics, personal finance, and residual models.

Figure 1.1 FinTechs high-level classification

Peer-to-peer retail lending solutions and digital payments seem to be the offers with stronger disruptive power. This can be due to the protracted credit crunch cycle in developed economies (following the GFC) and the astonishing growth of shadow banking in growth markets, as well as their appeal to established brands in social media and technology (e.g., Alibaba, Apple, Facebook, and Google), capable of intercepting money flows and direct consumer spending by means of behavioural analytics. Social media and digital technology are affording the opportunity to leverage virtual networks among individuals, without the need for traditional intermediaries. Potential creditors can reach out “almost directly” to potential debtors, by pooling in small ticket investments to lending facilities specialized in personal lending or small corporate. Although an exciting application of the synergies between finance and technology, there is mounting concern among international regulators about the soundness and sustainability of the players operating in shadow banking as these businesses thrive outside traditional channels regulated by international supervisory bodies.

As a matter of fact, cryptocurrencies are a rising and highly debated phenomenon at a time when world economies are running progressively on paperless cash, which can be used and transferred online. Mobile and wearable are granting IT firms unprecedented power to disintermediate centuries-old banking centrality of cash repository and payment services, and help to foster financial inclusion in poor countries. As telecommunications and the world wide web have become fairly ubiquitous, we can nowadays visit smarter cities and pay-per-use the underground using a smartphone instead of holding physical travel cards, carrying a credit card or unloading spare change out of our pockets. In this domain, blockchain technology has the potential to be truly revolutionary.

The internet has favoured the global acceptance of social media and granted innovators with a fertilized terrain to develop advanced analytics which identify, analyse, and target investors' preferences, and track their digital interaction and peer-to-peer relationships. Big data analytics, behavioural analytics, and cognitive computing operate in this space. FinTechs are given the opportunity either to adopt these techniques as part of their operations or to create new business models that provide analytics-driven services, such as digital assessment of personal credit risk.

FinTechs operating in the domain of personal finance are also on the rise. One of the main consequences of the GFC has been a tightening of international regulation to increase the cost of capital and foster investor protection. Although regulation is not always an even playing field across constituencies, we can clearly see a global trend towards the increase of fiduciary standards and suitability constraints, affecting the economic relationship between product factories (e.g., asset managers) and final advisors. This has ignited the rise of Robo-Advisors, which use digital tools to attract private money across the continuum of the clientele, promoting low fees and tax harvesting, typically built on passive investments or portfolio algorithms that threaten asset and wealth managers.

Finally the FinTech ecosystem is enriched by more models which we refer to as residual simply because they do not yet reach the headlines as much as the other players and are somewhat less numerous in each bucket. This is the case of FinTechs providing market or economics research, dealing with encryptions, password storage, or broader digital security.

Within this variegated ecosystem, Robo-Advisors are the game changers of personal finance and the main focus of this book. Most of the professional debate we can follow on social media and read in the financial press refers to the advantageous price point of Robo-Advisors, which is often a fraction of the cost that private investors face by accessing traditional banking. However, while the price battle may be short-lived, the aspect which provides them with long-term strength and which is fostering industry-wide transformation resides in their advanced user experience (UX). Final investors are often seduced by an investment experience which seems to be more personalized when compared with traditional e-trading solutions. Notwithstanding, we must be aware that most of the underlying investment processes which existing Robo-Advisors hide behind their catchy UX are instead somewhat institutionalized, as they are based on a limited number of model portfolios compared with the larger variety of individuals' needs and characteristi...

Table of contents

Cover

Series Page

Title Page

Copyright

Dedication

Preface

Acknowledgments

About the Author

Part One: Personalize Personal Finance

Part Two: Automated Long-Term Investing Means Robo-Technology

Part Three: Goal Based Investing is the Spirit of the Industry

Concluding Remarks

Bibliography

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access FinTech Innovation by Paolo Sironi in PDF and/or ePUB format, as well as other popular books in Commerce & Finance. We have over 1.5 million books available in our catalogue for you to explore.