The Impact of Joint Ventures on Bidding for Offshore Oil

John Douglass Klein

This is a test

This is a test

Compartir libro

256 páginas

English

ePUB (apto para móviles)

Disponible en iOS y Android

eBook - ePub

The Impact of Joint Ventures on Bidding for Offshore Oil

John Douglass Klein

Detalles del libro

Vista previa del libro

Índice

Citas

Información del libro

This volume, originally published in 1983 investigates join venture participants in outer continental shelf sales from institutional, theoretical and statistical points of view. It includes a section on the 1975 joint bidding ban, which reviews the principal study which led to the ban and several which are critical of it. The study of ofshore leasing sales goes far beyond the field of economics and this volume will therefore be of interest to those in geology and geophysics, finance, law, politics and statistics.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es The Impact of Joint Ventures on Bidding for Offshore Oil un PDF/ePUB en línea?

Sí, puedes acceder a The Impact of Joint Ventures on Bidding for Offshore Oil de John Douglass Klein en formato PDF o ePUB, así como a otros libros populares de Negocios y empresa y Industria energética. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

According to the theory of competitive bidding developed in Chapter III, bidders with superior ability to judge the value of tracts offered for sale tend to win more often, and to rank higher when not winning than other bidders. Furthermore, Chapter III suggested that one group of bidders, pure bidding joint ventures, were better at tract evaluation by virtue of their access to several independent sets of exploration data.

This chapter tests the theoretical conclusions of Chapter III, using the record of bids compiled by the United States Department of Interior, covering all federal offshore sales. Section one of this chapter describes the data set.

Section two considers the need to control for tract quality, or true tract value. In the theoretical discussion of bidding, true tract value was assumed to be equal for all tracts. Tracts in an offshore sale do not, however, have the same true value. In order to compare bids across tracts, differences in bids resulting from different true values must be eliminated or controlled for.

Section three identifies several types of joint ventures which have bid in offshore sales. The characteristics of joint ventures which would classify them as pure bidding joint ventures are also examined.

Section four contains the major empirical tests of the theory in Chapter III. The major conclusions are that pure bidding joint ventures do in fact win more often and in general rank higher than their rivals, but the joint ventures’ success comes at the expense of paying on average more for tracts won than other bidders. The latter result is at odds with the theory of Chapter III, in which all bidders expect to pay the same amount for tracts won.

Finally, the chapter concludes with a discussion of the costs and benefits of the prohibition of various types of joint ventures, including the recently proposed ban on joint ventures involving two or more major oil companies. Such a rule has been proposed by the Department of Interior, and is tentatively scheduled to take effect in the summer of 1975.1

1. The Department of Interior Data

Data employed in this chapter are published by the United States Department of Interior, in the Outer Continental Shelf Statistical Summary: 1954–1972, along with supplements issued following each federal offshore sale since 1972.2 The book lists every bid placed in a federal offshore sale, along with the identity of the bidder. In the case of joint ventures, the several participants are all identified, along with their respective shares in the joint venture.

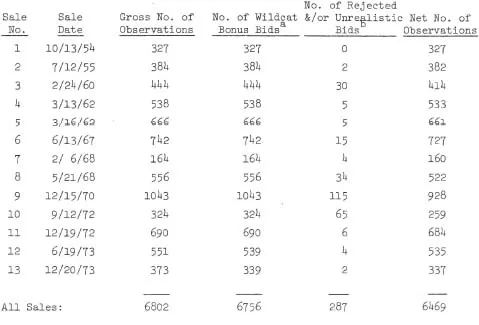

The sales included in the analysis are the thirteen major wildcat sales held between October, 1954 and December, 1973. Wildcat sales are those sales which offer tracts in relatively unexplored areas. During this period, the government also held eleven so- called drainage sales, in which tracts adjacent to previously leased lands were sold. Drainage sales were excluded from the current analysis, due to the asymmetric information, and the peculiar bidding strategies adopted by many firms in drainage sales. For a brief statistical description of all federal sales, see table 2-1.

For the sales included in the analysis, the data set included the following variables:3

(1) tract identification number;

(2) tract acreage;

(3) total bid (in dollars);

(4) rank of this bid among bids on the tract;

(5) total number of bids on the tract;

(6) oil company identification number;

(7)percentage interest of this firm in the bid;

(6') (7') if the bid was submitted by a joint venture, the last two items are repeated until all members are included;

(8)dummy variable indicating whether the bid was accepted or rejected by the government;

(9)sale date.

One variable frequently employed was the natural logarithm of bid. Since bids are generally acknowledged to fit a lognormal distribution,

n (bid) is approximately normal. Use of

n (bid) rather than absolute bid eliminates the overwhelming influence of large outliers in the data characteristic of a lognormally distributed variable.

In some of the empirical work which follows, each bid was considered an observation, while at other times, observations were made on the basis of tracts. In addition, much of the analysis was done on a sale by sale basis, to avoid the uncontrollable effects of time on bidding behavior. Fortunately the quantity of data available permits this kind of breakdown. The data set for the thirteen sales consists of a total of 6756 wildcat bids on 1689 different tracts.

The data set was restricted for most calculations in two ways. First, all bids rejected by the government were eliminated. These bids do not reflect the "fair market value" of the tract offered according to the Department of Interior. Second, a large number of unrealistically small bids, placed by private individuals such as Fats Domino and Howell Spear, were eliminated. These bids, often as low as one dollar per acre, never won a tract, for even when they were the only bids on a tract, they were rejected. Any bid of less than $22,026 was arbitrarily classified as unrealistic, and was eliminated from the data set (

n(22026:) = 10.0). Table 4-1 indicates the numbers of observations eliminated from each sale. Unless otherwise specified, calculations use the net data set, after eliminating unrealistic and rejected bids.

2. Controlling for Tract Quality

In order to explain the amounts bid in offshore sales, and to measure the impact of joint ventures, tract quality is an essential variable. An estimate of tract quality probably influences a bid more than any other single factor.

Table 4-1: Adjustment of Data Set.

aFive and 12 drainage tracts, respectively, were offered in the 6/13/73 and 12/20/73 sales. These tracts are excluded from the analysis.

bSome bids were both unrealistic and rejected.

Neither of the two possible ways to directly estimate the quality, or true value of a tract proves to be practical. First, pre-sale data might be used to estimate tract value, much in the fashion that bidders themselves make their estimates. The detailed geological and financial data required for each tract to make such estimates are, however, unavailable, not to mention the great technical knowledge needed to analyze these data to make an estimate of tract value.

Alternatively, data available after a tract has been developed might be used to estimate how much the tract should have been worth at the time of its sale. Actual production and cost records of tracts leased are available, and could be used to calculate a present discounted value of a tract at its leasing date.4 The major drawback to this method of estimating tract quality lies in the paucity of the data. As production from offshore tracts may continue for many years, only a relatively few tracts leased in federal offshore sales have completed their productive lives. Of course many tracts have been abandoned as being unproductive, but many other tracts leased as long ago as the 1950’s remain in production. This makes a complete tabulation of discounted present value possible in only a few cases.

Having ruled out direct measurement, tract quality must be estimated by observing bidding behavior. More valuable tracts should be characterized by first, higher bids, and second more bids. First, since bids are based in part on a bidder’s estimate of tract value, bids on a tract provide clues to the tract’s worth. Second, many bidders cannot afford to bid on all tracts in an auction, and they must choose which tracts to bid on, and which to pass over. Valuable tracts are likely ...