Many young people aspire to own their own home but face a myriad of challenges such as high property prices, the need to raise a large deposit, and difficulties of getting a mortgage.

The process of buying a property is also stressful, fraught with complexity and uncertainty, and a mistake can prove very costly. This book therefore provides a much-needed step-by-step guide to help those seeking to buy a property for the first time.

Packed with helpful and practical tips, this book gives a complete overview of the house-buying process, including finance, legal and property aspects. The authors discuss a wide range of topics, including:

creating the right mindset

the pros and cons of home ownership

how to choose a suitable property

how to save for a deposit

how to negotiate for a better price

how to get a mortgage

the steps in the house-buying process

how to ensure that mortgage payments can always be met

The book is written by experienced property buyers who have bought multiple properties, who have worked as a mortgage adviser and financial planner and who understand personal finance. It will be essential reading for undergraduate students in the field of accounting and finance and will also appeal to the general public, particularly those seeking to buy a property for the first time. After reading the book, readers will be able to map out a plan to buy their first property with greater confidence and make a better and more informed decision that will bring financial rewards.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Buying Your Home un PDF/ePUB en línea?

Sí, puedes acceder a Buying Your Home de Lien Bich Luu, Ai-Quang Tonthat en formato PDF o ePUB, así como a otros libros populares de Commerce y Immobilier. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

Home ownership has become a national obsession in the UK, and an overwhelming majority of young people want to buy their own home. A Santander First-Time Buyer Study in 2019 shows that over 91 per cent of young people interviewed aspire to climb the property ladder (Santander, 2019). Home ownership thus has become an important priority for young people, and this is fostered by a wide range of social, economic and psychological factors.

Motivations for home ownership

There are many compelling reasons why many of us desire to own our own home. We all need somewhere to live, and housing is an essential need. Yet, there are not enough homes in the UK to meet demand and the shortage is estimated at one million homes (Gompertz, 2020). The demand for housing is growing due to rising population, increasing life expectancy, high rates of divorce and the number of people living by themselves. However, the supply is restricted, due to the UK being an island country, and the rate of new houses being built has historically always been lagging behind the demand.

A second reason relates to our desire for decent and quality housing. When renting, we might pay high rents, but rental properties are sometimes poorly maintained because landlords may not carry out our requests for repairs, and we may have restrictions on how we use the property (e.g. no pets). In addition, the quality of housing might be poor, the furniture unsuitable and living condition cramped. In fact, it is found that those who own their homes not only spend less money on housing but also enjoy a better lifestyle because they have more space (an extra 4 m2 each over those who rent) (Savage, 2018).

There are also long-term financial benefits associated with owning a property. Sometimes, the monthly outlay to buy a home is little different from the amount paid in rent, but the big difference lies in your future economic security. Renting is often described as ‘dead money’, or ‘money down the drain’, because you are not building any of your own asset but enriching someone else’s pockets. Buying, on the other hand, enables you to acquire an asset and forces you to save to pay this off. Once the debt has been paid, you can live for free, whereas if you rent, you will continue to pay rent in retirement and until the end of your life. The decision to rent or buy thus can affect your quality of life and financial security in the long term.

However, a more compelling factor to own concerns our desire for stability. Rental contracts do not necessarily give us the right to stay in the same house as long as we would like. We all know that private renting can be precarious as we can be asked to move out, even when we do not wish to. No-fault evictions, where private landlords evict tenants at short notice without a good reason, create a lot of uncertainty, stress and anxiety. Insecurity about housing hurts our well-being and pockets, and constant moving makes us poorer because it often involves paying fees and removal costs, and time packing, unpacking and cleaning.

Owning your home, on the other hand, generally means you can stay in the same place for as long as you choose, which avoids disruptions to your work, social life and family ties. Living in the same area for a long time allows you to build up a greater sense of belonging and to form better support networks – known as social capital. A more stable life saves you from stress, helps you avoid moving costs and increases your well-being (Luu, Lowe et al., 2017, Chapter 8).

Owning a place we call home also gives us some healthy psychological benefits. A home after all represents more than just a place to live. A home is a special place in our hearts because it is the hub of our family life and a place of sanctuary where we retreat for relaxation and safety. Owning a home is therefore important because not only does this symbolise our independence and adulthood but it also gives us a sense of pride and achievement.

The sense of independence when owning a home is important because it gives us a strong sense of control and freedom. Home ownership gives us the power to make physical changes to the house and garden and ‘make it ours’; therefore, we have choice and an individual identity. No longer do we feel insecure, not knowing where we will be living and settled. Unless we fail to pay our mortgage payments, no one is going to force us to move out of our home.

The psychological and emotional benefits of owning a home are valued more than financial benefits. When interviewed by Santander Bank in 2019, more than 56 per cent of respondents stated that the most important reason to buy was due to the desire to have a sense of security, while economic benefits such as buying is a means of future wealth preservation (36 per cent), owning is cheaper than renting (36 per cent) and property is a smart investment (34 per cent) assume less importance (Santander, 2019).

Seen in this context, it is little wonder that getting on the housing ladder has become an important life goal for young people. Indeed, the Santander First-Time Buyer Study shows that home ownership is the top life goal for 51 per cent of respondents, followed by financial stability (40 per cent), travelling (29 per cent), getting fit (27 per cent), having children/family (27 per cent), reaching career goals (23 per cent), getting married (19 per cent) and being secure in retirement (16 per cent) (Santander, 2019). Unlike the old days when career, children and marriage came first, it is home ownership now that preoccupies the minds of young people.

Pros and cons of home ownership

Home ownership provides many benefits but there are also challenges.

The first recognized benefit is that homeownership can lead to wealth creation, which, in turn, can result in enhanced life satisfaction, better physical health and higher psychological well-being.

The second benefit is that homeownership tends to bring greater residential stability, which, in turn, is believed to produce better school performance among children and higher levels of civic engagement and social capital among adults. Traditionally, homeowners have remained in their homes considerably longer than renters. Evidence from the English Housing Survey supports this, and its 2018–19 report found that owner occupiers had lived at their current address for an average of 18 years, social renters 11.6 years and private renters 4.4 years. Among the private renters, 10 per cent had lived in the sector for less than one year (English Housing Survey, 2018–19). Private renters, thus, experience a highest level of residential instability.

The third benefit is that homeowners enjoy better quality housing. Compared to renters, homeowners tend to live in a house, often with gardens, and this type of housing provides a more stimulating environment for their children because they have somewhere to play and run around. As they own their property, there is a greater incentive in carrying out improvements and repairs to enhance their enjoyment and the value of their home. Thus, homeowners enjoy more control over their homes and a heightened sense of personal accomplishment and social status. This, in turn, leads to greater life satisfaction and psychological well-being.

Table 1.1 Pros and cons of home ownership

Positive impact

Expected benefits/liabilities

Anticipation of/actual wealth creation

Improved health, enhanced life satisfaction, improved parenting

Greater residential stability/security

Higher levels of high school and post-secondary completions, social capital, civic engagement

Better quality housing/home environment

Better school performance and youth behaviours, greater residential satisfaction, greater self-esteem

Better quality neighbourhood: physical and social

Better schools lead to better educational outcomes, and higher homeownership rates lead to enhanced social capital and less crime

Heightened sense of control/social status/accomplishment

Higher levels of life satisfaction and psychological health

Negative impact

Negative benefits

Mobility restrictions

Homeowners have more difficulty moving to better homes and neighbourhoods

Mortgage payment stress and repossession

Some homeowners experience considerable stress and other psychological problems

Home maintenance and repair stress/impacts

Some homeowners cannot afford to maintain their homes which may lead to health problems

Source: Rohe and Lindblad, ‘Re-examining the Social Benefits of Homeownership’ (2013)

Homeownership, however, does not always confer positive benefits. Some academics argue that homeownership can trap households, particularly those from ethnic minority and lower-income backgrounds, in areas that they would rather leave. Compared to renters, homeowners face higher transaction costs and their homes may be worth less than they owe on their mortgages (known as negative equity). However, a careful choice of property can help avoid negative equity.

Other challenges include difficulties in paying mortgage payments or carrying out repairs, and this can produce a high level of financial and psychological stress. However, planning for the future and taking out a suitable insurance policy can help address these issues.

Overall, the benefits of home ownership can outweigh the challenges, but you need to take appropriate steps to ensure that you buy in the right area and that you can always pay your mortgage.

Factors influencing home ownership

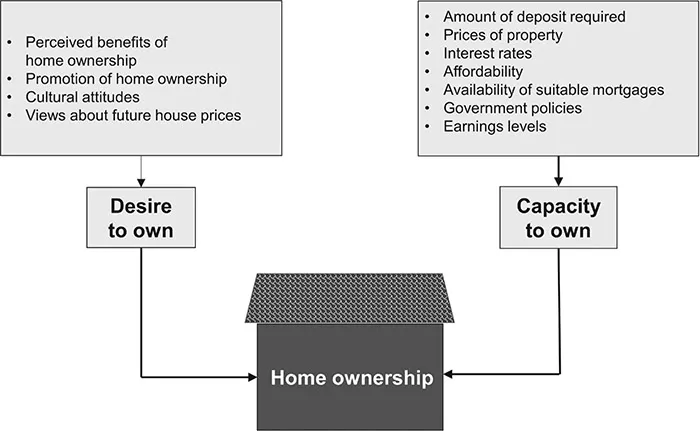

A study by Rohe and Lindblad (2013) for Harvard University argues that the tenure decision – to buy or rent – is a function of both the desire and the capacity to own. The desire to own is influenced by perceived benefits, cultural attitudes, promotion of home ownership by the government, estate agents, builders and others involved in the housing industry, and views about future house prices, as illustrated in Figure 1.1.

Figure 1.1 Factors affecting home ownership

Source: Adapted from Rohe and Lindblad, ‘Re-examining the Social Benefits of Homeownership’ (2013)

The authors argue that the perceived benefits are also affected by both direct and indirect experience with home ownership. This influence may be direct – individuals have a bad home ownership experience themselves – or indirect – they know someone who has had a good or bad home ownership experience.

In addition to the desire to own, home ownership is also influenced by the capacity to own. That capacity is determined by the amount of deposit required, availability of suitable property and mortgages, property prices, interest rates, affordability, and earnings levels. These factors, in turn, are affected by the state of the economy, government policies and lending practices.

Although the desire to own is high among young people, their capacity to own is now curbed by a wide range of economic and social factors. These will be discussed below.

Barriers to home ownership

Climbing the property ladder now is much more difficult than before for first-time buyers. Indeed, 70 per cent of would-be first-time buyers in the UK believe that the dream of homeownership is now impossible to achieve, and thus only 30 per cent are still hopeful....