Crypto-Finance, Law and Regulation investigates whether crypto-finance will cause a paradigm shift in regulation from a centralised model to a model based on distributed consensus.

This book explores the emergence of a decentralised and disintermediated crypto-market and investigates the way in which it can transform the financial markets. It examines three components of the financial market – technology, finance, and the law – and shows how their interrelationship dictates the structure of a crypto-market. It focuses on regulators' enforcement policies and their jurisdiction over crypto-finance operators and participants. The book also discusses the latest developments in crypto-finance, and the advantages and disadvantages of crypto-currency as an alternative payment product. It also investigates how such a decentralised crypto-finance system can provide access to finance, promote a shared economy, and allow access to justice.

By exploring the law, regulation and governance of crypto-finance from a national, regional and global viewpoint, the book provides a fascinating and comprehensive overview of this important topic and will appeal to students, scholars and practitioners interested in regulation, finance and the law.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Crypto-Finance, Law and Regulation un PDF/ePUB en línea?

Sí, puedes acceder a Crypto-Finance, Law and Regulation de Joseph Lee en formato PDF o ePUB, así como a otros libros populares de Diritto y Teoria e pratica del diritto. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

Crypto-finance is an anti-establishment movement that has emerged as a response to current financial markets that are intermediated and overcentralised. It has been said that the rise of cryptocurrencies such as Bitcoin is a response to dissatisfaction with the excessive risk-taking of financial intermediaries that led to the financial crisis, and the use by governments of quantitative easing as a remedial measure to bail out failing financial institutions. Blockchain-based crypto-finance has developed through the initial coin offering (ICO) market which aims to create a peer-to-peer platform for financing projects. It also addresses the current gaps in financing in the centralised markets provided by stock exchanges and the intermediated private equity market. As crypto-finance has developed, a number of concepts have been introduced that are unknown in traditional markets. Crypto-assets, cryptocurrency, ICO and security token offering, peer-to-peer project financing and the consensus-based regulatory model are all unfamiliar to the current financial markets. Privately issued cryptocurrency is unfamiliar to both users and regulators who are accustomed to relying on currency issued by central banks for payment, investment and as a monetary tool to manage the economy.

Some products such as crypto-vouchers and rewards-based investments are now used on blockchain-based crowdfunding platforms in a way that creates confusion among financial regulators, who are not clear about their jurisdiction, the legal nature of the products and the technology involved in the transactions. Regulators have attempted to bring ICO platforms into the existing regulatory regime for securities and it is possible to use the current securities framework to help understand ICO activity on the blockchain space and to identify risks. However, attempting to use the existing regime to exercise regulatory control of the innovative new market can have a negative impact on its development when the aim is to address structural problems in the financing gap and the lack of opportunity in a shared economy. The cross-border nature of the internet means that crypto-finance can be used by individuals in all corners of the world, and has the potential to transcend the existing financial markets. Yet we also need to use the current legal and regulatory frameworks as we analyse the components of the markets and their inter-relationships to devise an optimal governance model. There are many examples of the way the crypto-market challenges conventional understanding of the functions of the financial market, the proprietary nature of financial instruments, and the concept of law and justice. This means that we need to clarify the nature and purpose of the crypto-market so that policies, laws and governance models can be developed to ensure stability, safety, transparency and fairness. Technology, finance and the law are all essential components of the crypto-market that together define its concept, structure and dynamics.

Technology

This book examines the technology used to facilitate transactions in the different crypto-markets, including distributed ledger technologies, the blockchain, smart contract, encryption technologies and artificial intelligence. It also discusses how combinations of these technologies can support different crypto-markets, including the cryptocurrency market, the ICO market, the securities tokens offerings market, financial advisory services and the blockchain-based peer-to-peer energy trading platform. In addition, it explores how technology can be used in supervision, as legal technology and as regulatory technology on the crypto-market to provide governance. The aim of the discussion is not to provide detailed explanation of the design of each kind of technology, but to show how they can be embedded in the crypto-financial market to bring transformative effects. Many financial regulators adopt a neutral approach to technology where it is seen as neither good nor bad, so it is important to discuss the functions of technology in the context of finance to see how its transformative effect might operate. By using this approach, we can assess the benefits and risks that technology brings to the financial market and provide a sound basis for legal and regulatory intervention.

Finance

Like technology, finance is also a neutral activity and financial markets can be forces for good as well as evil. So it is important to divide the current financial markets into different sectors such as payment markets, trading spaces, advisory services and peer-to-peer energy trading platforms, to see how technology may be used in each segment or sector. Combinations of the various technologies can result in greater efficiency and efficacy, but they also bring risk. The main function of the financial market is to act as an intermediary between entrepreneurs’ projects and investors’ finance and in this way they distribute both profit and risk. There are various ways of managing this distribution through the design of different financial products but the financial crisis has shown that financial intermediaries have themselves been taking on the role of investors by partaking in both profits and risks. There were no effective rules in place to control the level of profits gained or to mitigate risk. In the recent crisis, there were such large defaults in the market that institutions were unable to absorb the consequences and states needed to step in to bail them out. In this situation, the financial intermediaries broke the chain that is needed to support a healthy economy. Because states had to bail out the intermediaries and inject more cash into the economy, the legitimacy of the state as the guardian of financial stability was threatened. If the crypto-market is to provide a solution to structural problems in the current financial markets, it should not only provide potential remedial action to crises that arise, but also act as a catalyst for a socio-economic transformation. The hope is that the crypto-market can transform the financial market by democratising it.

As the industry develops, the crypto-market can play a role not only in finance but also in laying down the conditions for socio-economic transformation by providing access to finance, a shared economy and justice. Because of this, it is important to decide what kind of financial markets the crypto-market should support. It might be that using technology can enhance the efficiency of the market, but this single benefit might be disproportionate to the investment needed to create the necessary infrastructure. In this book, I discuss some new financing markets including cryptocurrency, initial coin offering, securities token offering, algorithm-driven execution and advisory services and the peer-to-peer energy trading platform, to show how disintermediated and decentralised markets can give control to entrepreneurs and investors. In addition, I also discuss what roles financial intermediaries and the state should play in distributing profits and risk through a renewed governance model in this virtual space.

Law

Law therefore plays an essential role in the development of technology in financial markets. Regulators need to understand and approve any technology proposed and must consider both whether it is safe to use and whether it complies with regulatory objectives. For Fintech, policy makers and regulators can apply risk-based regulation and leave the participants to negotiate their intended outcomes. However, the crypto-market has a stated outcome of bringing transformative effects so is it appropriate there to continue to use risk-based regulation or should the law play a more active role in promoting the crypto-market’s aims? The intended outcome is relevant to the design of the governance framework and in identifying gaps in the application of current regulation to a particular crypto-market. Clarity about the intended outcome can also help to determine whether property law or relational law should apply to a particular transaction. When the crypto-market is combined with another utility market such as the retail energy market, the combination alters the key purpose of the market. The legal framework and regulatory regime should then be designed to facilitate that new regime, promoting sustainability in this example.

Data governance in the crypto-market

Data and data governance have not been extensively explored in the literature of financial law and regulation. The crypto-market generates large quantities of data, which can be used to transform socio-economic conditions and improve living standards. The current centralised and intermediated market prevents smaller investors and individual entrepreneurs from accessing critical data for raising finance, identifying suitable investment targets or monitoring the risk of their investment. Centralised market infrastructures such as central banks, exchanges, clearing houses and settlement institutions possess and control large amounts of transaction data that are used by financial intermediaries and states to provide services and monitor risk as well as to develop new products, services, projects and policies. But they are also in a position to restrict access to data, charge fees for access or exchange data for benefits with third parties. If the crypto-market is to democratise information and give individuals control, data must be shared with them. Financial intermediaries also collect critical data as required by financial regulators in order to fulfil their risk management obligations. Yet at the same time, data in their possession can enable them to provide further projects and services for the market. What is more, financial intermediaries have super computers that can process data and obtain information more quickly than is possible for individuals. The fundamental role of financial intermediaries is to bring together projects and investors, but with the advantage of privileged access to data, they can themselves act as entrepreneurs and investors rather than simply providing intermediary services. For instance, a bank’s client database allows it to develop an asset management business which in turn helps it to develop securities services that also enhance M&A business advisory services. Without resetting the goals for digital finance, market foreclosure and unfair market practices can exacerbate the structural problems caused by intermediation and centralisation.

Three components

Therefore, this book examines three components of the financial market – technology, finance and the law – and shows how their interrelationship dictates the structure of a crypto-market. Technology is an enabler and can drive improvement to social-economic conditions but it can also be used to foreclose the financial market, deprive an individual of wealth and enable state surveillance of citizens. The financial market can be a means of promoting social benefit and prosperity by facilitating the exchange of goods and services. However, it can also play a role in supporting imperialism, colonisation, financial crisis and war. The financial market should provide stable, safe and fair conditions for all its participants: infrastructure providers, intermediary firms, entrepreneurs and investors. And along with these stakeholders, there are others who benefit from the activity of financial markets such as regulators, the government and market service providers. If the aim of the financial market is not clearly defined and innovation continues without a sense of purpose, the financial market can become a space for gaming where the drive for profit leads to excessive risk-taking without accountability. In this regard, technology can help realise the purpose of the financial market and help participants achieve their aims but the purpose and goals of the market need to be agreed upon by stakeholders. Participants can agree to create a casino without a sense of purpose aside from financial gain if they wish to, but if something with a higher ideal is intended, a social contract needs to be agreed that specifies the market’s objectives. Based on this, it is possible to develop new principles for a financial market that set out the conditions for socio-economic transformation.

2 Distributed ledger technologies in capital markets

DOI: 10.4324/9780429023613-2

Introduction

In this chapter, I will explain how blockchain technology can be implemented on the current capital markets and identify the relevant risks and the possible governance solutions needed.

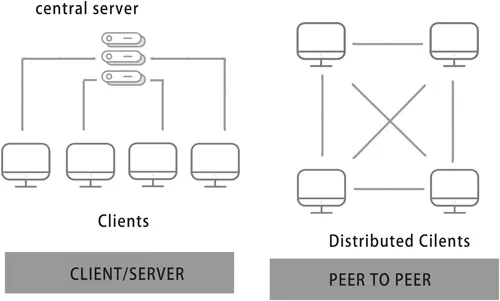

Blockchain is one of the algorithmic technologies and distributed ledger technologies (DLTs), as illustrated in Figure 2.1. It is a register containing information shared, recorded and replicated among nodes1 that has been successfully applied to the creation of cryptocurrencies – value units of transactions on the blockchain ecosystem – such as Bitcoin and Ethereum.2 Bitcoin and Ethereum are two types of cryptocurrency built on blockchain technology. They are token-based and traded on exchanges, such as on Coinbase.com, a currency exchange brokering between digital assets – a cryptocurrency or reference to a record of the ownership of an asset on a blockchain – and fiat currencies. It should be noted that there is a distinction between public/permission-less networks (public chain) like Bitcoin and Ethereum and the private permissions world (private chain) where only permitted nodes can participate in the network. Public/permission-less ledgers are open to everyone to contribute data to the ledger and cannot be owned. Private and permissioned ledgers may have one or many owners, and only they can add records and verify the contents of the ledger. The successful usage of blockchain in cryptocurrency, which transforms the internet information to internet value,3 has promoted interest in applying it to capital markets – mainly securities trading.4 This is because such blockchain technology can be modified to incorporate rules, smart contract, digital signatures and other tools such as Artificial Intelligence5 to make contracts and financial transactions safer and more cost-effective.6

1 Nodes refer to the device participating in the peer-to-peer network by running a blockchain client software and relaying information (transactions and blocks). 2 The Economist, ‘The Promise of the Blockchain: The Trust Machine’ (31 October 2015) www.economist.com/news/leaders/21677198-technology-behind-bitcoin-could-transform-how-economy-works-trust-machine. [Accessed 06 November 2017]; Philip Boucher, European Parliamentary Research Service, ‘How Blockchain Technology Could Change Our Lives’ (February 2017) http://www.europarl.europa.eu/RegData/etudes/IDAN/2017/581948/EPRS_IDA(2017)581948_EN.pdf; Saman Adhami, Giancarlo Giudici, and Stefano Martinazzi, ‘Why Do Businesses Go Crypto? An Empirical Analysis of Initial Coin Offerings’ (20 October 2017). Available at SSRN: https://ssrn.com/abstract=3046209; Satoshi Nakamoto, ‘Bitcoin: A Peer-to-Peer Electronic Cash System’ (2008) available at: https://bitcoin.org/bitcoin.pdf. 3 See Chapter 5 on cryptocurrency. Dan Tapscott and Alex Tapscott, How the Technology Behind Bitcoin Is Changing Money, Business, and the World (Penguin Publishing Group 2016). 4 Trevor Kiviat, ‘Beyond Bitcoin: Issues in Regulating Blockchain Transactions’ (2016) 65 Duke Law Journal 65; Philipp Paech, ‘Securities, Intermediation and the Blockchain: An Inevitable Choice between Liquidity and Legal Certainty’ (2016) 21(4) Uniform Law Review 612–639; and Taketoshi Mori, ‘Financial Technology: Blockchain and Securities Settlement’ (2016) 8(3) Journal of Securities Operations & Custody 208–227. 5 See Chapter 7 on artificial intelligence. 6 Digital Asset Holdings, a US blockchain startup, is building business applications and market structure systems based on the distributed ledger, such as working with exchanges and post-trade providers i.e. Depository Trust & Clearing Corp., which provides settlement and clearing services.

Figure 2.1 Central and distributed models

Some people are sceptical of such a use in capital markets and have discounted securities trading with blockchain as mere hype, presented as a replacement for all the other technologies as a sol...