The Ultra-High Net Worth Guide to Growing and Protecting Assets

Richard P. Rojeck

This is a test

This is a test

Compartir libro

English

ePUB (apto para móviles)

Disponible en iOS y Android

eBook - ePub

Wealth

The Ultra-High Net Worth Guide to Growing and Protecting Assets

Richard P. Rojeck

Detalles del libro

Vista previa del libro

Índice

Citas

Información del libro

With few exceptions, books on personal finance focus on investing. And with few exceptions, these same books focus on the general public. This book takes a comprehensive approach to the subject, directed to the ultra-high net worth reader, filling this void.

While there is no shortage of experts in legal, tax, investment, and other matters, in many ways, ultra-high net worth individuals are underserved, even as they are confronted with potentially increasing challenges to the growth and protection of their wealth. Planning strategies lacking a foundation of client-driven values and purpose, coordination and a mechanism for ongoing review and maintenance result in suboptimal outcomes.

As a Certified Financial Planner Professional with over 30 years of experience serving individuals with substantial wealth, Richard Rojeck presents an alternative approach, one based upon a comprehensive planning process. He addresses the eight key planning areasfor the ultra-high net worth individual, describing the top strategies within each. He challenges you to assess your current planning and provides guidance on how to select an often-missing member of the advisory team.

With a readable and approachable style, this book will help you more effectively grow and protect your assets for yourself, your family, and your charitable causes.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Wealth un PDF/ePUB en línea?

Sí, puedes acceder a Wealth de Richard P. Rojeck en formato PDF o ePUB, así como a otros libros populares de Negocios y empresa y Servicios financieros. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

In his book, The Affluent Society, American economist John Kenneth Galbraith writes “Wealth is not without its advantages and the case to the contrary, although it has often been made, has never proved widely persuasive.”1 The creation and accumulation of wealth being the natural outcome of an ambitious individual encountering a free-market system, the question remains only “how much wealth is enough?” At the individual level, the answer to “Do I have enough?” can be both a mathematical as well as an emotional issue, and it has very little to do with the traditional notion of retirement. The question, “Do I have enough?” can be translated into “Am I financially independent?”

Of course the answer depends on your desired lifestyle, since we know that there is no amount of wealth that a given standard of living could not consume. People with vast sums of wealth are declaring personal bankruptcy merely because of an out-of-control lifestyle.

The answer also depends on how you define your financial independence, for which I suggest the following definition: “Being able to enjoy one’s desired standard of living while engaging in one’s desired activities, without regard to the current rewards associated with them.” In other words, “I want to be able to do what I want to do when I want to do it and not care about the financial rewards.”

As you think about financial independence, it’s important that you consider whether it should be built on the endowment or the annuity concept. Let me explain. An endowment is a sum of money sufficient in amount such that the earnings (current income plus appreciation) are sufficient to provide for the need, adjusted for inflation, forever. In other words, your original capital will remain intact and, in fact, will grow at least at the rate of inflation. The point in building an endowment is so you never have to worry about how long you live. Life expectancy becomes irrelevant. I would suggest this is the truest measure of financial independence. And, by definition, at your death, your wealth will pass to your heirs and or to society.

By the Numbers

You have heard about college endowments or endowments for the arts. This is the same concept. The amount of the endowment is deemed sufficient to pay for a college professor’s salary, or to augment an opera’s performing costs, or an art museum’s operations, indefinitely, without consuming the original principal, adjusted for inflation. The process starts by establishing an expected long-term return for its investment portfolio: 7–8% is most common. From this is subtracted the expected rate of inflation, the portion of the return that must be reinvested, to allow the portfolio to grow and offset the future impact of inflation. The U.S. inflation rate has averaged about 3% over the past 100 years. Subtracting 3% from 7% yields the 4% spendable return commonly used. As charities are generally tax exempt, absent from this calculation is an adjustment for income tax. So for example, an endowment of $2.5 million invested at 4% net, would generate income of $100,000 annually to support the organization’s operations.

The annuity concept, on the other hand, assumes that a sum of capital is accumulated so that—based upon an anticipated investment return—the principal plus earnings on a declining balance will satisfy the need for a given period of time. In this case, the given period of time is, of course, how long you plan to live. In other words, in addition to consuming all the income, you are also using up an increasing amount of the principal each year until it is exhausted.

The risk here is that you may live too long, exhaust your principal, and wind up on your children’s doorstep, tin cup in hand. Given the choice, most everyone would prefer the endowment approach. But like everything else in life, you get what you pay for. Endowment “costs” more, and therefore, has implications on everything else, from how long you must work, how much you must sacrifice in order to save, your future sustainable income, and everything in-between.

Let’s look at an example, first taking the endowment approach. Assume your desired lifestyle comes with a $1 million annual price tag after tax, meaning you spend about $83,000 per month. If we use 3% as the assumed after-tax investment return (versus 4% in the case of a tax-exempt organization), dividing $1 million by 3% yields required invested capital of $33.3 million. Of course, invested capital excludes your other, non-income-producing assets such as your home, a second home, furnishings, artwork, cars, a yacht, etc. In contrast the annuity approach would require just $21 million using the same assumptions and a 30-year life expectancy. Results are proportional, so if your lifestyle is $2 million, $3 million or more, simply increase the required sums accordingly.

The mathematics behind this endowment approach is similar to that in valuing income-producing assets, whether they be bonds, oil wells, stocks, real estate, or closely held businesses. The income stream (e.g., interest, dividends, net operating income) is divided by a discount or “cap rate” to yield a “present value” or today’s dollar equivalent of the income stream, which yields the price a buyer would pay to acquire it. So in our example above, a buyer would be willing to pay $33 million in order to purchase a $1 million income stream, after tax, paid indefinitely, adjusted for inflation.

While this methodology is broadly accepted and, arguably, straightforward, it does have a shortcoming in that it assumes a consistent investment return. That is, it assumes the investment portfolio earns 7%, inflation is 3%, taxes 1%, every year. But we know this is not the case; investment returns can vary widely from year to year and this can have a big impact on the outcome. In fact a significant body of research supports the notion that the pattern or sequence of returns greatly influences whether your assets will be sufficient to sustain your lifestyle.2

To more accurately determine the amount of invested capital necessary, considering the variability of returns, financial planners often use a Monte Carlo simulation. It gets its name from the famous Mediterranean seaside resort known for its casinos and high rollers. Monte Carlo simulation seeks to determine the likelihood of a given outcome by running numerous trials or iterations, typically 1000. It’s particularly useful when no mathematical formula exists to precisely calculate an outcome, though as a simulation, the result is a range of outcomes rather than a precise forecast.

Let’s look at a Monte Carlo simulation outcome for our example: $1 million lifestyle, 3% inflation assumption and 7% annual returns from a broadly diversified portfolio. For a $50 million investment portfolio, there would be virtually a zero percent probability of portfolio depletion, 62% probability of preservation of the original sum, with a $66 million median ending balance (i.e., half the outcomes were above and half were below this sum), adjusted for inflation in 30 years. Obviously, this tool can provide valuable insight.

Another way to forecast financial independence is to simply use a spreadsheet, conservatively projecting income from existing businesses, real estate, your investment portfolio and other holdings, considering income tax and the impact of inflation on the income need.

Enough Already

Enough about the mathematical implications, what about the emotional dimensions of “Do I have enough?” People are motivated by a variety of factors: fear, greed, guilt, altruism, competitiveness—any of which may drive them to aspire to and strive for a certain level of wealth. Often, these attitudes and values were imparted by parents or influential figures or developed through life experiences. They can be both constructive and destructive. Discerning the difference and knowing when you have “enough” can be an enlightening experience.

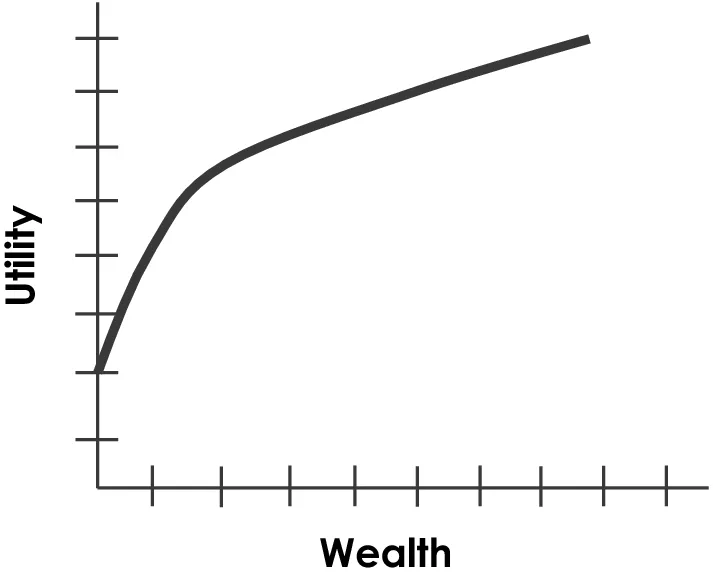

We’re all familiar with the concept of diminishing marginal utility. Thinking about the marginal utility of nice to haves: a bigger or a second or third home, a yacht, or airplane and whether they bring you genuine happiness, may help you answer the question “Do I have enough?” There are, after all, consequences associated with acquiring and maintaining them: the potential toll on your financial security, your health, family and other relationships. Understanding the trade-offs frees you to put less at risk (Fig. 1.1).

Fig. 1.1

Utility of wealth

I’m reminded of a client who was very nearly financially independent, enjoying a seven-figure lifestyle and an eight-figure estate built as a real estate developer and investor. He was neither liquid nor well-diversified. And he was highly leveraged, convinced it would support even greater wealth accumulation. When I challenged him with the question, “Is it really necessary to put so much at risk in the pursuit of more?”, he was dismissive of the notion that he was overly aggressive. The year was 2007. In the ensuing financial crisis his assets fell like dominos and he found himself having to virtually start over. Perhaps a check on your own situation is to ask yourself, “In the next financial crisis, will I be a buyer of distressed assets, or a seller of them?”

Of course, many continue to build wealth not from a need to secure financial independence. They are financially independent many times over, living comfortably, well within their means. They enjoy their worldly possessions but are not enslaved by a need for more of them. They love the occupation by which they’ve earned their wealth, and are exceptionally good at it. And so their estate continues to grow.

It’s been said, “You’re rich when you know you have enough.” A financial planner can be the catalyst to helpingyou determine what’s important and where your utility function begins to diminish and the curve flattens. She can do the modeling to help you quantify “enough.” And she can show you how to deploy surplus wealth for the benefit of your family and community.

Questions to Consider

Do you have enough?

Do you have adequate liquidity and reasonable diversification?

Is your debt level and structure prudent considering the risk to your financial security?

Do you have a plan to deploy your surplus wealth for the benefit of your family and community?

Footnotes

1

John Kenneth Galbraith, The Affluent Society (Boston: Houghton Mifflin, 1958).

2

Philip L. Cooley, Carl M. Hubbard, and Daniel T. Walz, “Portfolio Success Rates: Where to Draw the Line,” Journal of Financial Planning 24, no. 4 (April 2011): 48–60.