In the wake of the 2016 U.S. presidential election, investors and the electorate alike are seeking clarity on a wide range of macro policy issues that will impact the economy and markets in the years ahead. The primary goal of this book is to provide an objective source for investors to learn about economic policy issues that surfaced. Topics include long-term growth, the federal budget deficit, healthcare reform, tax reform, regulatory policies affecting the financial system and environment, the nexus of monetary, exchange rate and trade policies, and globalization. The book explains how these issues have evolved, considers arguments from both sides of the political divide, and draws upon evidence from studies by experts in the respective areas. A related goal is to assess the likely impact of economic policies on financial markets. While the presidential election was close, the markets' response was decisive: U.S. and global equity markets went on a tear as consumer and business confidence soared. This surprised many investors who believed a Trump victory would be bad for financial markets. It also caused many to question whether expectations embedded in markets were too optimistic. Sargen's assessment is presented in the opening and concluding chapters.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Investing in the Trump Era un PDF/ePUB en línea?

Sí, puedes acceder a Investing in the Trump Era de Nicholas P. Sargen en formato PDF o ePUB, así como a otros libros populares de Business y Financial Services. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

Nicholas P. SargenInvesting in the Trump Erahttps://doi.org/10.1007/978-3-319-76045-2_1

Begin Abstract

1. Is Trump’s Election a Game-Changer?

Nicholas P. Sargen1

(1)

Fort Washington Investment Advisors, Cincinnati, OH, USA

End Abstract

Donald Trump’s victory over Hillary Clinton in November 2016 caught most political pundits and market commentators completely off guard, much like the outcome of the Brexit vote in the United Kingdom. Previously, markets had been priced for a Clinton victory and Republican control of Congress, which spelled more policy gridlock. Following Trump’s victory and Republicans retaining control of both houses of Congress, investors became hopeful that a decade of government dysfunction might finally be over.

On the eve of the election the consensus among Wall Street commentators was Trump’s chances of winning were low—on the order of 30–35%. Moreover, in the event he pulled off a rare upset, it was widely believed financial markets would sell off, because Trump had no prior political experience and was accustomed to make off-the-cuff statements and tweets. Immediately following the announcement of his victory, the US equity markets plummeted. However, they stabilized soon after, and then began to take off once Trump made a conciliatory speech about his opponent.

In ensuing weeks investors were willing to give the President-elect the benefit of the doubt that his pro-growth agenda would reap benefits in the future. Trump campaigned on a theme of making America great again, and his list of policies included a host of measures favorable to US businesses. After the election, he followed up by appointing several prominent business leaders to Cabinet positions and advisory roles.

The US markets responded with a powerful surge in stocks and somewhat higher bond yields that lasted throughout 2017 (Table 1.1). While the consensus among economic forecasters was the economy would continue to expand close to the 2% trend rate during the current expansion, investors were hopeful that the former growth trend of more than 3% per annum would be restored before long. At the same time, Wall Street analysts revised their projections of S&P 500 corporate profits higher: The consensus called for them to expand by 12% in 2017, which is the high end of the range over the past decade.

Table 1.1

Financial market returns, pre- and post-2016 elections through 2017

Pre (Jan 1–Nov 8)

Post (Nov 8, 2016)

S&P500

6.6%

27.9%

Russell 2000

6.5%

30.5%

EAFE ($)

−0.6%

28.4%

MSCI EM ($)

16.3%

31.9%

US Treasury

3.8%

−0.5%

IG credit

7.8%

4.1%

High yield

15.2%

9.4%

Source: S&P, Frank Russell, MSCI, US Treasury, Barclays, ML

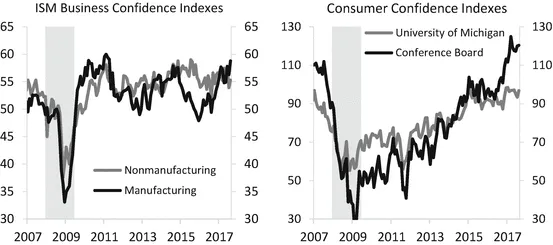

Indeed, some commentators observed that Trump’s victory unleashed “animal spirits,” as confidence readings for both businesses and consumers spiked (see Fig. 1.1). It also spilled over to business surveys for both the manufacturing and services sectors. Within financial markets the term “Trump trade” was used to describe the combination of a surging stock market, rising Treasury yields, narrowing corporate credit spreads and a strong dollar, as well as a general rise in risk assets globally.

Fig. 1.1

US business and consumer confidence indexes. (Source: ISM, Conference Board, University of Michigan)

Amid these developments many people asked the following question: Will Trump’s election mark a turning point for the economy and markets, or are investors’ expectations too high? I gave a presentation on that topic just as President Trump assumed office, which helps to frame the issues covered in this book.

Elections Usually Have Fleeting Impacts on Markets

My answer to the question is that if history is any guide, the market’s optimism may prove excessive. The reason: It is rare that presidential elections impact the economy and financial markets for very long. Most of the time the effects are fleeting, and the ultimate outcomes are dictated by factors unrelated to elections.

A notable exception is Ronald Reagan’s first election victory.1 Investors at the time were hopeful President Reagan’s “supply-side” policies of tax cuts and regulatory relief and his commitment to low inflation and a strong dollar would transform the American economy, ending a decade of stagflation and pessimism. These hopes were ultimately borne out, but it took several years for Reagan’s economic policies to bear fruit.

Even then, credit must be given to Paul Volcker and the Federal Reserve for abandoning policy gradualism in favor of “shock therapy,” in which interest rates were allowed to rise to record levels to break the back of inflation and inflation expectations. This resulted in a severe recession and a developing country debt crisis in 1982 that threatened the stability of the world’s financial system. However, once the Fed altered course by easing policy aggressively, the stage was set for an ensuing recovery and expansion that proved to be one of the strongest on record. Furthermore, the rally in financial markets that began in mid-1982 continued through Reagan’s second term, the administration of George H.W. Bush and throughout the Clinton era , when the United States benefited from a technological renaissance.

The ensuing period from 2000 to 2016 is another story, as both the Bush and Obama Administrations were adversely affected by busts in asset bubbles, first in technology and the second in housing. In both instances, aggressive policy easing by the Federal Reserve helped to contain the fallout to the economy and financial system. However, the trend growth rate of the US economy slowed to about 2% per annum, well below the prior rate of more than 3% in the post-World War II era. This slowdown in economic growth was accompanied by material changes in productivity growth for the economy and in labor force participation rates.

Given this backdrop, the overriding goal of the Trump administration is to restore the glory years before the bursting of the tech and housing bubbles—or what Trump characterized in his campaign motto “Make America Great Again.” The challenge facing his administration, therefore, is to formulate a coherent set of policies that not only will revive the economy in the short run, but over the long term as well. In this regard, investors need to have a clear understanding of the ways macroeconomic policies affect economic growth and financial markets so they can formulate a sound investment strategy.

Economic Prospects at the Start of 2017

As President Trump assumed office in January, investors were generally upbeat that the US economy was about to improve and break out of the 2% growth doldrums. Part of the reason is the economy gained traction in the second half of 2016 and the unemployment rate dipped to 4.6%. Personal consumption, which accounts for about 70% of aggregate demand, had been solid, and car sales were running at a record pace.

At the same time, growth abroad was improving, as Europe benefited from persistent low, and even negative, interest rates and a soft euro. The Chinese economy also stabilized in the second half of 2016 from a subpar start, which in turn affected many emerging economies that were suppliers to China. The Japanese economy also showed signs of improvement. Thus, for the first time since 2010, the global economy was on the cusp of a synchronized expansion.

The main factor that excited investors was the prospect of significant changes in policies that would impact the US economy . They included cuts in personal and corporate taxes that were intended to boost consumption and to encourage business capital spending, which had been an area of persistent weakness during the economic expansion. Also, another component of Gross Domestic Product (GDP) that had been unusually weak—government spending—appeared to be set to increase, as the Trump administration was in favor of increased spending for the military. During the campaign, Trump also spoke about the need for a large increase in spending on infrastructure, with the financing to come from a combination of public and private sources. Consequently, it appeared that aggregate demand was poised to accelerate, although the timing and magnitude were uncertain.

In order to achieve sustained growth, however, supply-side forces needed to be unleashed as well. The principal reasons some economists are pessimistic about the future are they foresee only modest growth of the labor force and continued low productivity growth. They contend economic growth is likely to remain in the vicinity of 2%—or more than a full percentage point below the post-war average. (This issue is discussed in depth in the Chap. 2.)

The underlying theme of the Trump administration and Congressional Republicans , by comparison, is that subpar growth is mainly a consequence of government policies that have discouraged growth and deterred businesses from investing on plant and equipment. Accordingly, the thrust of their policies is to reinvigorate confidence of business leaders so they are willing to expand business capital spending that is vital to improved productivity growth. Toward this goal, the Trump administration and Republicans in Congress are seeking to reduce and simplify corporate taxes, encourage businesses to repatriate overseas pr...