![]()

III SYSTEMS AND PROCESSES

In this chapter and the three that follow, we address systems and processes for key account management. In Section II, we discussed the first three elements of the congruence model—strategy (Chapter 2), organization (Chapter 3), and human resources (Chapter 4). This final element of the congruence model includes systems and processes for planning, managing information flows, identifying opportunities, measuring customer satisfaction, and many others. These systems and processes enable key account managers effectively to develop and implement strategies and plans for individual accounts.

To the greatest extent possible, this wide variety of human- and information-technology-based systems and processes should be common across all key accounts. Common systems not only reduce development costs, they promote an organizational coherence that is impossible to achieve if individual managers develop and use idiosyncratic processes. Of course, these systems and processes should not “straitjacket” the key account manager. But within a framework of common systems and processes, the key account director should identify best practice that can increment key account management overall to a higher level of performance.1

Chapters 5 through 7 focus on perhaps the most important managerial process undertaken by key account managers—planning. In firms with well-developed key account management systems, the key account plan is the crucial document that drives the supplier-firm/key-account relationship. In Chapter 8, we turn to a series of other systems and process for enhancing key account management.

PLANNING AND STRATEGY MAKING FOR KEY ACCOUNTS

Key account planning and strategy should be closely related to a broader level of planning and strategy—typically by market or market segment, possibly by customer industry—that logically precedes planning for individual key accounts. However, if a few key accounts together comprise the vast majority of the available market, this broader level of strategy making effectively coalesces with key account planning and strategy. Regardless of the order of strategy development, the key account strategy must be consistent with strategy developed at the higher level.

As part of developing the broader level of planning and strategy making, marketing personnel should collect the appropriate data and conduct various strategic analyses of the market and market segments, competition, and the supplier firm. Key account managers should be able to access this data so that they don’t have to reinvent the wheel for each of their own key account plans. As information is used and reused, the supplier firm benefits from scale economies in data collection and analysis. Since all key account plans in a particular industry are based on a common understanding of critical market and competitive imperatives, individual readers should identify areas where their own organizations might benefit from such centralized data gathering and analysis.

The Key Account Plan

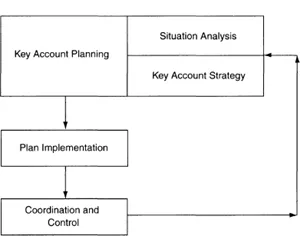

Essentially, the key account plan comprises two elements, the situation analysis and the key account strategy.2 It should, however, also include an executive summary that can serve as a briefing document for senior executives who may interface with the key account. The process for developing the plan is embedded in a broader managerial system that includes plan implementation, and a coordination and control process by which the plan is updated over time (Figure III.1). Later, we offer a series of planning exercises to aid in conducting the situation analysis and formulating a key account strategy.

FIGURE III.1: Managing the Key Account

SITUATION ANALYSIS

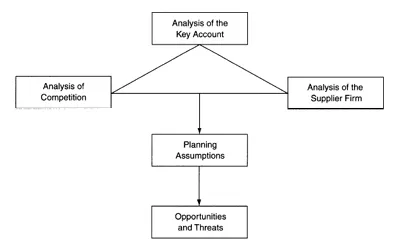

The situation analysis is the fundamental underpinning of the supplier firm’s key account strategy. If competently performed, the situation analysis provides a solid foundation for strategy development. Conversely, if the situation analysis is not well done, the foundation for the strategy will be weak, suboptimal decisions will be made, and scarce resources allocated ineffectively.3 For these reasons, the situation analysis must be comprehensive; as a result, the discussion here and in Chapter 6 is dense. I make no apologies for this, because effective key account strategy is a direct consequence of solid situation analysis (Figure III.2).

Still, we fully recognize that the level of analytic detail suggested may not be appropriate for all supplier-firm/key-account relationships. For example, it is one thing to supply products based on technology critical to the key account’s survival and growth; it is quite another to be a secondary supplier of a noncritical raw material. The appropriate level of information gathering and analysis may well differ in these two cases. Furthermore, many key account managers have responsibility for multiple accounts and just do not have the resources for as extensive an approach as we suggest. For these reasons, the key account manager must decide the appropriate planning approach for his or her situation. That said, better strategy emerges from more thorough planning.

For each of three basic sets of analyses—key account, competition, and supplier firm—three related steps must be conducted:

FIGURE III.2: The Situation Analysis

• Significant amounts of data, some primary and some secondary, some qualitative and some quantitative, some anecdotal and some formal, must be collected to form the raw material for the various analyses.

• From this data, fundamental trends must be separated from random fluctuations and projected into the future.

• For each fundamental trend, two questions must be asked:

• What are the implications of this particular trend for the key account?

• What are the resulting implications for the supplier firm?

Such questioning provides insight that leads both to the development of planning assumptions, and the identification of a set of opportunities and threats for the key account manager to address in developing the key account strategy.

KEY ACCOUNT STRATEGY

The key account strategy is concerned with resource allocation. It is developed in the context of a broad overall focus on the key account relationship comprising a vision and mission that set broad parameters for the resource allocation process. As we shall see in Chapter 7, the key account strategy encompasses several interrelated elements that must both be internally consistent and follow logically from the situation analysis.

![]()

CHAPTER FIVE

Key Account Planning

Analysis of the Key Account

THE PURPOSE OF KEY ACCOUNT ANALYSIS

Successful completion of the key account analysis provides the key account manager with various possible means of assisting the key account in achieving its several corporate, business, financial, and market objectives. The analysis helps the key account manager identify the full scope of potential opportunities and threats at the key account. This identification, together with analyses of competitors and the supplier firm itself (Chapter 6), leads to a series of decisions regarding which opportunities to pursue (and which to avoid), which threats to combat, and the particular strategic approaches to pursue (Chapter 7).

To achieve the level of insight necessary to become so well positioned, the key account manager must seek information and conduct analyses in four related areas. In this chapter, we discuss key account fundamentals, strategic key account analysis, identifying and addressing key account needs and delivering customer value, and the buying analysis. We conclude by identifying potential information sources. (See Exercise 1 for a planning document to conduct an analysis of the key account.)

KEY ACCOUNT FUNDAMENTALS

Key account fundamentals represent what an educated observer of the key account, much less a key account manager, should know about the account. For the key account manager, it frames the account and helps provide perspective when a particular subunit of the organization is addressed. Of course, the supplier firm may seek business only in a restricted domain, for example, in an individual business unit. Nonetheless, a broad knowledge of the organization can be invaluable in understanding the internal reality faced by those key account executives with whom the manager and other supplier firm personnel must deal.

In addition, good understanding of the fundamentals demonstrates to key account executives a significant personal commitment by the key account manager. The ability to speak knowledgeably about the organization enhances the manager’s credibility with key account personnel. This is especially true if the key account manager can show himself as better acquainted with the key account than its own employees! Conversely, if the key account manager does not possess this information, it may result in a real credibility problem at the account.

Finally, in those organizations with complex interlocking shareholdings and directorships, understanding the overall corporate dynamics may provide invaluable insight into the location of critical sources of power in the key account.1

Among the sorts of fundamental data the key account manager should assemble are:

• Ownership. How does the overall organization fit together in terms of parent companies, subsidiaries, ownership interests, and so forth? Who are the directors, principal owners? What roles do they play in the corporation? Do they rubber stamp the CEO’s decisions or are they more active? Where are corporate offices located? Is the key account a public company; if so, where are its shares listed?

• Organization. Is the organization centralized with significant power at corporate headquarters or do individual subsidiaries operate more or less autonomously? If the key account is a global organization, does it operate with a domestic U.S. division and a separate international division, with geographic area divisions, with global product divisions, or some other kind of structure? How are developments in telecommunications, computer technology, and the Internet affecting the key account’s organization structure and processes?

• Top Management Cadre. Who is the CEO and who are other members of the top management group? Are they successful? Do they have the confidence of the board of directors or is there a difficult relationship? What is known about their business and management philosophies? What type of corporate culture are they trying to instill? In particular, have they articulated a vision and/or values for the corporation:

• Vision is the description of an ideal future state, a statement meant to inspire employees over the long haul.

• Values are a set of beliefs that serve to guide behavior. Values may either be “hard,” such as profitability and market share, or “soft,” such as integrity, respect for others, trust, and preeminence of customers.

Locations. Where are the account’s fixed assets located? Where are its plant and distribution center locations? What are its production capacities? How many employees does the account have? How are they distributed across locations?

Corporate Actions. What important actions has the key account taken recently as regards major resource shifts, significant capital spending, mergers, acquisitions, divestitures, strategic alliances, joint ventures, R&D initiatives, vertical integration and disintegration (outsourcing), new product introductions, increased internationalization, new market entry, use of the Internet, participation in B2B exchanges, and the like? How successful have these been?

Financial Performance. What has been the key account’s revenue and profit history both overall and for relevant business units? What is its trend in return on assets? What is the trend in its stock price? What is the trend in earnings per share? What is its debt/equity ratio? How is its debt rated? What ratios are important to the account? How does its performance compare to major competitors?

Future Prospects. What is the long-run outlook for the key account? Does it face any significant legal or regulatory problems? How is it perceived by the financial community? Do the majority of financial analysts recommend sell, hold, or buy? Why?

• Timing. What are the time cycles for the key account—for example, the budgeting cycle? What are important dates, such as the fiscal year and annual meetings. Is there a regularity to important announcements, for example, CEO meetings with financial analysts.2

STRATEGIC KEY ACCOUNT ANALYSIS

Strategic account analysis is especially important for those firms that wish to become quality suppliers to, or partners with, their key accounts. In order to make sensible decisions on how to help the key account achieve its objectives, the key account manager must both understand the key account’s objectives and strategy, and also assess its ability to be successful. To develop the appropriate depth and breadth of data to conduct these analyses, the manager should attempt to become intimately involved with the key account’s strategic planning process. She should strive to secure a seat at the table as the key account’s senior executives plan their firm’s future directions. The manager should not be just a passive recipient of information about the key account. Rather, by working closely together, supplier firm and key account personnel may together engage in creative problem solving that improves the competitiveness of both parties.

Clearly, to achieve this level of intimacy with key accounts is not a simple matter. However, over the years, I have been impressed with the number of key account managers who claim to enjoy this sort of relationship with their major clients. Such a level of mutual commitment only results from feelings of trust that may take many years to develop. But, once achieved, if carefully nurtured, these relationships can provide enormous...