Corporate Valuation

Measuring the Value of Companies in Turbulent Times

Mario Massari, Gianfranco Gianfrate, Laura Zanetti

- English

- ePUB (apto para móviles)

- Disponible en iOS y Android

Corporate Valuation

Measuring the Value of Companies in Turbulent Times

Mario Massari, Gianfranco Gianfrate, Laura Zanetti

Información del libro

Risk consideration is central to more accurate post-crisis valuation

Corporate Valuation presents the most up-to-date tools and techniques for more accurate valuation in a highly volatile, globalized, and risky business environment. This insightful guide takes a multidisciplinary approach, considering both accounting and financial principles, with a practical focus that uses case studies and numerical examples to illustrate major concepts. Readers are walked through a map of the valuation approaches proven most effective post-crisis, with explicit guidance toward implementation and enhancement using advanced tools, while exploring new models, techniques, and perspectives on the new meaning of value. Risk centrality and scenario analysis are major themes among the techniques covered, and the companion website provides relevant spreadsheets, models, and instructor materials.

Business is now done in a faster, more diverse, more interconnected environment, making valuation an increasingly more complex endeavor. New types of risks and competition are shaping operations and finance, redefining the importance of managing uncertainty as the key to success. This book brings that perspective to bear in valuation, providing new insight, new models, and practical techniques for the modern finance industry.

- Gain a new understanding of the idea of "value, " from both accounting and financial perspectives

- Learn new valuation models and techniques, including scenario-based valuation, the Monte Carlo analysis, and other advanced tools

- Understand valuation multiples as adjusted for risk and cycle, and the decomposition of deal multiples

- Examine the approach to valuation for rights issues and hybrid securities, and more

Traditional valuation models are inaccurate in that they hinge on the idea of ensured success and only minor adjustments to forecasts. These rules no longer apply, and accurate valuation demands a shift in the paradigm. Corporate Valuation describes that shift, and how it translates to more accurate methods.

Preguntas frecuentes

Chapter 1

Introduction

1.1 WHAT WE SHOULD KNOW TO VALUE A COMPANY

- Industrial economics and business strategy with reference to the analysis of the industry and competitive context devoted to understanding the validity of the company's business model, its past results, and its future plans

- Theory and techniques of finance with regard to the basic principles of net present value, to the underlying links between leverage and value, to models that explain stock prices on financial markets, and finally to the techniques which correctly depict the business plan in terms of cash flow

- Economic theory, in particular with regard to the relationship between uncertainty and value1

- in all those cases in which the simplifications assumed in the standard models presented in the finance textbooks do not permit the development of convincing valuations

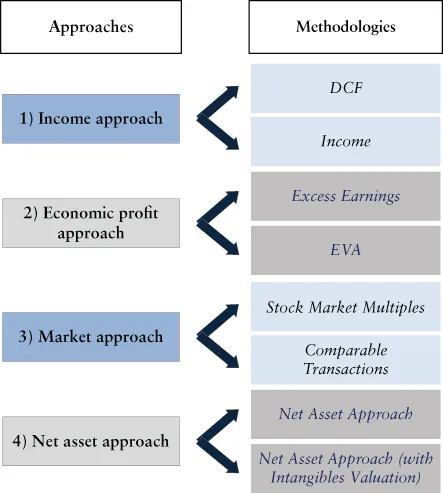

1.2 VALUATION METHODS: AN OVERVIEW

- Income approach

- Economic profit approach

- Market approach

- Net asset approach

1.2.1 Common Practices in the Accounting and Financial Communities

- The DCF method based on the discounting of future cash flows derived from the company's business plan or assumed by the analyst

- Stock market multiples or multiples derived from comparable transactions

- better fit into some economic and accounting environment;

- follow, therefore, a logic more understandable to the actors for whose benefit the valuation is performed; and

- allow one to effectively and convincingly deal with special valuation problems, such as third-party interests or tax benefit valuations.

1.2.2 Approach of This Book

- The net present value (NPV) principle

- How to deal with uncertainty

- The relationship between uncertainty and value

- The need for preventing, when possible, subjective judgments in value determination

1.3 THE TIME VALUE OF MONEY

- Calculate the asset relevant cash flows and their time distributions.

- Discount any cash flows at a rate expressing the time value of money.