The Insurance Technology Handbook for Investors, Entrepreneurs and FinTech Visionaries

Sabine L.B VanderLinden, Shân M. Millie, Nicole Anderson, Susanne Chishti

This is a test

This is a test

Compartir libro

English

ePUB (apto para móviles)

Disponible en iOS y Android

eBook - ePub

The INSURTECH Book

The Insurance Technology Handbook for Investors, Entrepreneurs and FinTech Visionaries

Sabine L.B VanderLinden, Shân M. Millie, Nicole Anderson, Susanne Chishti

Detalles del libro

Vista previa del libro

Índice

Citas

Información del libro

The definitive compendium for the Insurance Digital Revolutio n

From slow beginnings in 2014, InsurTech has captured US$7billion in investment since 2010 — a 10% annual compound growth rate is predicted until at least 2020. Three in four insurance companies believe some part of their business is at risk of disruption and understanding the trends, drivers and emerging technologies behind Insurance's Digital Revolution is a business-critical priority for all growth-minded firms.

The InsurTech Book offers essential updates, critical thinking and actionable insight — globally — from start-ups, incumbents, investors, tech companies, advisors and other partners in this evolving ecosystem, in one volume. For some, Insurance is either facing an existential threat; for others, it is a sector on the brink of transforming itself. Either way, business models, value chains, customer understanding and engagement, organisational structures and even what Insurance is for, is never going to be the same. Be informed, be part of it.

Learn from diverse experiences, mindsets and applications of technologies

Discover new ways of defining and grasping growth opportunities

Get the inside track from innovators, disruptors and incumbents

Be updated on the evolution of InsurTech, why it is happening and how it will evolve

Explore visions of the future of Insurance to help shape yours

The InsurTech Book is your indispensable guide to a sector in transformation.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es The INSURTECH Book un PDF/ePUB en línea?

Sí, puedes acceder a The INSURTECH Book de Sabine L.B VanderLinden, Shân M. Millie, Nicole Anderson, Susanne Chishti en formato PDF o ePUB, así como a otros libros populares de Business y Finance. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

The six pieces selected for this section bring together the expected multiplicity of views, and provide a rich, informative, and engaging set of connected conversations exploring what InsurTech is, for whom, by whom, and why?

Valentino Ricciardi urges us to cut through the InsurTech “noise”, setting out how the definition of InsurTech should be clear, simple, and comprehensive so that it actively shapes the vision of next generation talents and participation. Ricciardi’s InsurTechs share the characteristics of early adoption of technology, digital by default, focused on specific niches and, most importantly, value creators – for customers, incumbents, or both.

Steve Tunstall also defines InsurTech as absolutely essential for insurance to remain relevant to the customer. His ruthless dissection of the failings of an industry he loves also asks us: insurance needs InsurTech, but does InsurTech need (incumbent) insurance? Tunstall explains how only 10% of corporate risk faced by the CEO finds relevance in insurance solutions today, and how current failings could lead to systemically low penetration in emerging economies. For him, InsurTech may not have all the answers, but certainly some of the most important ones, driven by digitalization.

For Alex Ruthmeier, the digital transformation of insurance is InsurTech. He sees four major transformative changes: customer transparency; direct-to-customer connection; a very few scaled players with low margins; and demand-driven (customer) focus. Ruthmeier’s vision of InsurTech sees “human brokers” disappearing for all but complex risks, and more quickly than you might think.

Michael Jans also sees big challenges for brokers, but equally InsurTech as a huge opportunity for a broking rebirth. Writing from the perspective of the US, and its 40,000+ independent broker/agent firms, Jans envisions a near future of carriers shifting allegiances away from broker partners. He sees InsurTech as the route to delivering on that “peace of mind” customer promise at the core of the broker proposition, and the technology and scale to make the customer’s “heart sing”.

Jannat Shah Rajan posits a definition of InsurTech emerging from insurance’s Industrial Revolution where innovating customers, increasing life expectancy, and change in life stages drive change in Life, Wealth, and Pensions, as well as Non-life. Her theory of a protective “regulatory moat” around incumbents makes it axiomatic for her that collaboration will be the order of the day. As she says, “Incumbents are the best testing ground for new InsurTech propositions.” And lastly in this section, Karl Heinz Passler asks us to see not 1,200+ InsurTechs globally, but a segmented landscape of “InsurTechs” and “Real InsurTechs”. He sees two distinct groups: the first, including those improving Customer Experience (CX); those enabling incumbents; and those becoming risk carriers themselves.

The second group are those Passler considers to be challenging the very underlying assumptions and foundations of insurance. He asks us to see “Real InsurTechs” as those eschewing historic data in favour of real-time and AI-generated data; those adopting usage-based models; and those linking corporate earnings to settling claims. These differing yet related and intertwined definitions share a common core in the belief that InsurTech is directly contributing to the reinvention of the way insurance is imagined, funded, constructed, and done.

InsurTech Definition as Its Own Manifesto

By Valentino Ricciardi

Insurance and InsurTech Knowledge Consultant, McKinsey & Co.

InsurTech is the new cool word within the vocabulary of the financial services, replacing the term FinTech, which established itself in the last years of 2000 when companies like Square, Transferwise, and Stripe accelerated the payments revolution launched by PayPal in the US and Alipay in China. However, I believe that InsurTech does not have yet a clear, agreed, and established definition.

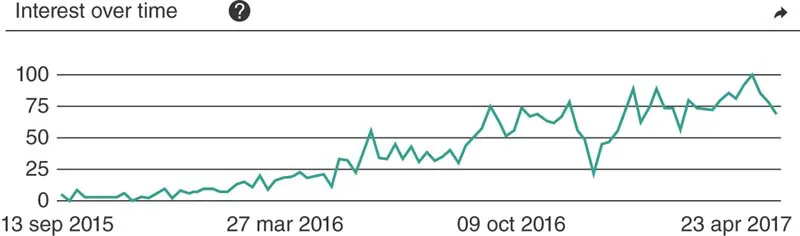

An InsurTech definition should cover different concepts well beyond the idea of combining insurance and technology to include the native customer-centric approach, as well as the potential that technology has to enable incumbents’ value chain or to disrupt incumbents’ consolidated business models. This definition should be open and inclusive so as to host new and innovative technologies that are relevant both now and in the future. So all technologies at the forefront of insurance innovation, such as artificial intelligence, chatbots that enable H2C (Human to Customers) in distribution, as well as advanced analytics that are looking for the right use cases in the data-driven business of insurance, need to fit and find their own space in the definition and concept of InsurTech, which has increased significantly, as shown in Figure 1.

Figure 1: InsurTech interest over time based on Google research Source: Data from Google Trends (September 2015 – June 2017)

Three Enigmas: Who? What? How?

Incumbents, startups, Venture Capital (VC) funds, and many other stakeholders are all players within the InsurTech field with their own agenda, perspective, and view of the InsurTech phenomenon. The fact that no shared definition was out there increased the temptation for stakeholders to come up with their own, based on their understanding of InsurTech. It often resulted in partial definitions, or definitions not yet shared and adopted by the insurance innovation community. This generated “noise” and hasn’t helped to provide a clear understanding of the InsurTech phenomenon. A simple approach to get to a definition of InsurTech will be to find the answer to three simple enigmas: Who? What? and How?

The first question to address is: “Who is the subject, the engine of transformation within the insurance and insurance technology landscape? Is InsurTech identifying a specific type of startup, or a whole ecosystem of multiple companies operating in the domain of insurance technology?”

InsurTech, in its current common use of experts, practitioners, and bloggers, is identifying an ecosystem of many different companies that operate in the insurance technology domain. Those companies are early adopters of new technologies, digital by default and, most importantly, focused. InsurTechs are early adopters of innovative technologies such as big data, machine learning, cloud, and the Internet of Things, compared to the insurance incumbents, slowly evaluating and adopting. The early adopters are advantaged on this path by the fact that they are “digital by default”, enabling innovation without the legacy of IT systems or overcomplicated procedures and operations.

Focus is another strong quality of the InsurTech, whose success is dependent on their concentrating on a specific line of business, area of the value chain, or client segment. There is no InsurTech so far that focuses on more than one line of business and customer segment at the same time. Successful InsurTech companies like Lemonade, Trov, and Oscar focused only on a specific line of business, i.e. Home, Property, and Health, respectively. The fact that they are looking for niches in the insurance business makes them more credible when they promise to challenge or help incumbents who are constrained by their size or other organizational factors.

Once we have in mind the concept of an InsurTech ecosystem it will be easy to define an “InsurTech company” as the company or startup that plays on this field. But they are not the only players in this domain; established, innovative players are fully entitled to be included. Arguably, the first InsurTechs were in fact the direct insurance companies that posed the initial threats to incumbents in the retail motor sector, such as Admiral in the UK and Geico in the US; the price comparison websites popular in the UK; or the IT and ERP system providers focused on insurance, like Guidewire and Tia Technology.

The second questions to address are: “What are those startups doing within the context of the InsurTech ecosystem? What is their primary goal?”

InsurTechs disrupt the traditional business model of incumbents developing innovative customer value propositions able to attract and engage clients, for example, they can enable full digital distribution of insurance products. Most often, InsurTechs enable the value chain of incumbent insurers offering innovative technologies and solutions to improve operational efficiency; for example, they can automate relevant processes across the value chain. However, our answer will remain partial if we don’t add the primary goal of InsurTechs: to generate value either for customers, insurance incumbents, or both. Of course generating value is a “sine qua non” for any new industry that wants to ensure its own survival and sustainability to prosper over the long term. InsurTechs can focus either on generating value for clie...