Frequently Asked Questions in International Standards on Auditing

Steven Collings

This is a test

This is a test

Compartir libro

English

ePUB (apto para móviles)

Disponible en iOS y Android

eBook - ePub

Frequently Asked Questions in International Standards on Auditing

Steven Collings

Detalles del libro

Vista previa del libro

Índice

Citas

Información del libro

Auditing has hit the headlines over recent years, and for all the wrong reasons, and in today's environment, the result of negligent auditing can be serious resulting in sizeable fines and even withdrawal of audit registration which can be costly in terms of fee income.

Frequently Asked Questions in International Standards on Auditing presents the relevant standards in a concise and jargon-free way, enabling auditors to appreciate the reasoning behind the standards and undertake audit work effectively. This book focuses on the main areas of the auditing standards and also addresses some key areas where audit firms are failing and which have been flagged up by audit regulators. The FAQs cover the main parts of each standard, and each question will be answered in a practical context, with worked examples showing how the standards are applied in real situations.

Preguntas frecuentes

¿Cómo cancelo mi suscripción?

Simplemente, dirígete a la sección ajustes de la cuenta y haz clic en «Cancelar suscripción». Así de sencillo. Después de cancelar tu suscripción, esta permanecerá activa el tiempo restante que hayas pagado. Obtén más información aquí.

¿Cómo descargo los libros?

Por el momento, todos nuestros libros ePub adaptables a dispositivos móviles se pueden descargar a través de la aplicación. La mayor parte de nuestros PDF también se puede descargar y ya estamos trabajando para que el resto también sea descargable. Obtén más información aquí.

¿En qué se diferencian los planes de precios?

Ambos planes te permiten acceder por completo a la biblioteca y a todas las funciones de Perlego. Las únicas diferencias son el precio y el período de suscripción: con el plan anual ahorrarás en torno a un 30 % en comparación con 12 meses de un plan mensual.

¿Qué es Perlego?

Somos un servicio de suscripción de libros de texto en línea que te permite acceder a toda una biblioteca en línea por menos de lo que cuesta un libro al mes. Con más de un millón de libros sobre más de 1000 categorías, ¡tenemos todo lo que necesitas! Obtén más información aquí.

¿Perlego ofrece la función de texto a voz?

Busca el símbolo de lectura en voz alta en tu próximo libro para ver si puedes escucharlo. La herramienta de lectura en voz alta lee el texto en voz alta por ti, resaltando el texto a medida que se lee. Puedes pausarla, acelerarla y ralentizarla. Obtén más información aquí.

¿Es Frequently Asked Questions in International Standards on Auditing un PDF/ePUB en línea?

Sí, puedes acceder a Frequently Asked Questions in International Standards on Auditing de Steven Collings en formato PDF o ePUB, así como a otros libros populares de Betriebswirtschaft y Wirtschaftsprüfung. Tenemos más de un millón de libros disponibles en nuestro catálogo para que explores.

Chapter 1 What is the Role of the International Auditing and Assurance Standards Board?

The International Auditing and Assurance Standards Board (IAASB) is responsible for setting the International Standards on Auditing (ISAs). It is an independent standard-setting body that sets high-quality, international standards on aspects of:

Auditing;

Assurance;

Quality control;

Review; and

Related services.

The IAASB was founded in March 1978 and was previously known as the International Auditing Practices Committee (IAPC) whose work was then focused on three areas, namely:

Objects and scope of audits of financial statements;

Engagement letters; and

General auditing guidelines.

As one can appreciate, the work of the IAASB has significantly evolved and in 1991 the IAPC's guidelines were renamed the International Standards on Auditing.

In 2002, the IAPC changed its name to the IAASB and the International Federation of Accountants (IFAC) approved a series of reforms that were primarily designed (among other things) to strengthen the standard-setting process, which included the processes at the IAASB, in order to best serve the public interest.

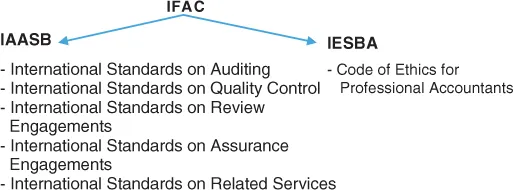

The IAASB is a technical standing committee of IFAC which is also closely linked to the International Ethics Standards Board for Accountants (IESBA) which produces the Code of Ethics for Professional Accountants. An illustration of the hierarchy is as follows:

The standards issued above by the IAASB are authoritative material (as stated in the Preface to International Standards on Quality Control, Auditing, Assurance and Related Services Pronouncements (Revised 2011)). As these standards are authoritative, they must be followed in an audit that is conducted in accordance with the ISAs.

In addition to ‘authoritative’ material published by the IAASB, they also publish ‘non-authoritative’ materials which offer a form of ‘guidance’ rather than mandatory requirements. These are:

International Auditing Practices Notes (IAPNs). These are designed to provide practical assistance to auditors rather than impose mandatory requirements.

Practice Notes Relating to Other International Standards.

Staff Publications: these are designed to raise awareness of new or emerging issues in relation to the standards and to direct attention to the relevant parts of IAASB pronouncements.

Some jurisdictions will have their own standard-setting bodies. For example, the Financial Reporting Council is responsible for standard-setting in the UK. Some countries do adopt ISAs but have to amend them to be country-specific. For example, in the UK, ISAs are adopted but are amended in some areas to be compatible with UK practices and these are then referred to as ISA (UK and Ireland).

Example

ISA 570 Going Concern requires the auditor to consider whether management have made a going concern assessment which covers a period of 12 months from the date of the financial statements. However, in the UK and Ireland, this going concern assessment should cover a period of 12 months from the date of approval (or expected date of approval) of the financial statements.

The UK and Ireland ISA therefore covers a different time span which demonstrates how the standard-setters have amended the mainstream ISA to be specific to the UK and Ireland. In the UK the going concern ISA is known as ISA (UK and Ireland) 570 Going Concern. In the UK and Ireland ISAs are often coined ‘ISA pluses’ because they contain additional or amended requirements to the mainstream ISA issued by the IAASB.

The Clarity Project

In 2004, the IAASB undertook a programme in which the objective was to enhance the clarity of the ISAs. The overall aim of this Clarity Project was to enhance the understandability of the ISAs which would, in turn, enable consistent application of the standards and go to improve overall audit quality on a worldwide level. This was an important exercise following some well-publicised corporate disasters and the decimation of confidence within the auditing profession.

Following the Clarity Project, each standard now has a clear structure with transparent objectives, definitions and requirements, together with application and other explanatory material which drill down further into the requirements of the ISAs. The structure of the new standards makes it easier to understand what is required and what is guidance. In addition, ISQC 1 Q...