The book explores the endogenous creators of inside money, the commercial banks, and their key role in igniting the 2007-8 monetary crisis and the aftermath of the Great Recession. This is an area of study overlooked by the traditional approach in the form of neo-classical analysis, a body of theory based on a barter system of exchange. Money has evolved from a construct of barter to become a medium of exchange based on fiat money and loan creation by the banking system, underpinned by legal tender, and therefore, a creature of law. It is not a phenomenon exogenously controlled by the monetary authorities and simply assumed to be a "veil" over the real economy, which just determines the absolute price level.

This monograph, in the eyes of the student, represents critical thinking and the realization of a more precise formulation of the endogenous money supply with various features systematically added in an attempt to derive a fully dynamic model of the monetary system, which will be straightforward to visualize and contrast with the benchmark approach.

Domande frequenti

Come faccio ad annullare l'abbonamento?

È semplicissimo: basta accedere alla sezione Account nelle Impostazioni e cliccare su "Annulla abbonamento". Dopo la cancellazione, l'abbonamento rimarrà attivo per il periodo rimanente già pagato. Per maggiori informazioni, clicca qui

È possibile scaricare libri? Se sì, come?

Al momento è possibile scaricare tramite l'app tutti i nostri libri ePub mobile-friendly. Anche la maggior parte dei nostri PDF è scaricabile e stiamo lavorando per rendere disponibile quanto prima il download di tutti gli altri file. Per maggiori informazioni, clicca qui

Che differenza c'è tra i piani?

Entrambi i piani ti danno accesso illimitato alla libreria e a tutte le funzionalità di Perlego. Le uniche differenze sono il prezzo e il periodo di abbonamento: con il piano annuale risparmierai circa il 30% rispetto a 12 rate con quello mensile.

Cos'è Perlego?

Perlego è un servizio di abbonamento a testi accademici, che ti permette di accedere a un'intera libreria online a un prezzo inferiore rispetto a quello che pagheresti per acquistare un singolo libro al mese. Con oltre 1 milione di testi suddivisi in più di 1.000 categorie, troverai sicuramente ciò che fa per te! Per maggiori informazioni, clicca qui.

Perlego supporta la sintesi vocale?

Cerca l'icona Sintesi vocale nel prossimo libro che leggerai per verificare se è possibile riprodurre l'audio. Questo strumento permette di leggere il testo a voce alta, evidenziandolo man mano che la lettura procede. Puoi aumentare o diminuire la velocità della sintesi vocale, oppure sospendere la riproduzione. Per maggiori informazioni, clicca qui.

The Creators of Inside Money è disponibile online in formato PDF/ePub?

Sì, puoi accedere a The Creators of Inside Money di D. Gareth Thomas in formato PDF e/o ePub, così come ad altri libri molto apprezzati nelle sezioni relative a Business e Servizi finanziari. Scopri oltre 1 milione di libri disponibili nel nostro catalogo.

Money is a characteristic of every transaction since the dawn of civilisation and trade. There have been various commodities and precious metals used as the medium of exchange , but it was the warrior monks (http://www.bbc.co.uk/news/business-38499883) that were the forefathers of modern banking and the creation of paper money , which has evolved into a digital format on computer platforms, underpinned by legal tender .1 It shows the crucial part of money plays in the evolutionary development of the modern economy and that it is the lifeblood of the monetary system . It is a fact that the lion’s share of consumption and investment depends not only on saving but on the creation of loanable funds by retail banks. They can create money with loans as a medium of exchange out of themselves (Schumpeter 1934). At the height of the process of creative destruction (Schumpeter 1943), where the new stage of growth by way of new goods and services based on fresh discoveries of new technological advances and innovations, which must be financed by the banking sector (which) and is key part of the division of labour .

In this introductory chapter, the concept to notice is the flow of income through the medium of money from those who have a surplus to those in deficit via the financial system, which embodies markets where agents and financial firms trade financial instruments such as derivatives, shares and bonds . These financial firms include commercial (or retail) banks, for example, which are institutions that receive agents’ creation of real income in the form of interest, profit , rent and wages paid as deposits, who wish partly to save or use as a medium of exchange for their day-to-day transactions. In turn, banks use this deposit base to lend to borrowers through loans , creating new credit as a medium of exchange for households and companies. They create further deposits and saving in the form of ‘circular causation’: circularism . The point to notice is that they are not financial intermediates in the traditional sense because they create new money , whereas contributions by policyholders within insurance companies form investment funds in a broad range of securities. The buying of these securities, such as equities, represents the flow of income to the issuers for, say, the running of firms to earn profits from production or in providing services. These activities are effectively transferring saving of excess income in the form of bank deposits from lenders to borrowers .

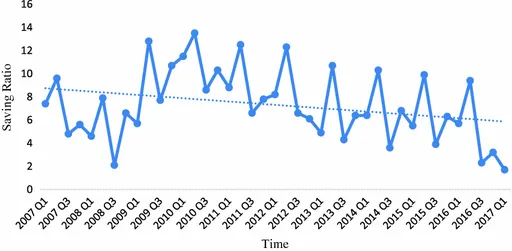

In the advanced countries like the UK, incomes are high with many individuals and groups of agents who would like to lend. Keynes in the General Theory ofEmployment, Interest andMoney (1936) made the assertion that as income grows the difficulty is that the marginal propensity to save has a tendency to rise, whilst the marginal propensity to consume falls. This, however, has not been the experience of the UK economy recently, where the underlying trend of the saving ratio (http://www.bbc.co.uk/news/business-40454385) has been in decline along with disposable income, as shown in Fig. 1.1, which means the demand for loanable funds will increase. Historically setting aside this recent fact, this is why developed economies have complex financial systems with indirect lending to reduce transaction costs and increase economic growth (Bywaters and Mlodkowski 2012). Direct lending is costly and risky, although unlikely to happen in reality because organised markets reduce this costly search and risk on account of willing traders and financial intermediaries who provide the avenue for the transfer of funds between borrowers and lenders , pushing the banking sector to one side. The biggest advantage for lenders is that they can sell their financial claims on the borrowers after making loans . In fact, the main activity is the refinancing of loans originally made by others. This is the advantages of organised markets for saving and lending of financial funds.

Fig. 1.1

Decline of saving ratio over the period, 2007 Q1–2017 Q1

(Source Office of National Statistics)

1.2 Saving and Lending

According to Keynes , agents have conflicting motives and it is the financial system’s function to reconcile these differences. Saving

is the difference between income

and consumption

, which is

which is a function of income along with the secondary variable, the rate of interest , whereas real investment depends on expectations of future profit . In theory, this saving finances the purchase of capital goods via real investment (I), but there is no reason why they should be equilibrium. In fact, in advanced countries incomes are high and exceed real investment , and as a result, there is a financial surplus (or surplus units) available for lending. This is the net acquisition of financial assets

, expressed in the following form as an identity:

(1.1)

This is equal to potential lending or the accumulation of ‘hoards’ in the form of liquidity .2 Initially, saving can be a combination of investment and net acquisition of financial assets , which could be in the form of lending or hoards, that is

(1.2)

In order to induce lenders with a surplus to lend, it is necessary for them to obtain the maximum return for the minimum ofrisk, although there is a chance that the return may differ from their expectations . It could come in the form of default, reduced income and capital losses as well as inflationary risks. Organised markets reduce these risks in addition to offering liquidity to lenders so that they can retrieve their capital funds quickly with certainty. There are, however, considerable advantages for borrowers as well, the discussion below at the outset.

1.3 Borrowing

Those who wish to spend over and above their income have financial deficits (or deficit units). This means having to reduce the accumulation of past financial assets or incur liabilities (or debts). This could be state institutions, firms and individual households, whose incomes are not large enough to cover their current consumption or capital expenditure. In the case of firms, they borrow funds to buy investment goods and renew circulating capital that will derive future incomes at present value that will not only service the loans , but also repay the principal debts along with earning gross profits.

The motives of the borrowers are to minimise cost and to maximise the period for which they want ...