1 Introduction

Islamic banking is now a widely used term. Islamic banking has emerged in recent decades as one of the most important trends in the financial world. There has always been a demand for financial products and services that conform to the Syariah (Islamic law). With the development of viable Islamic alternatives to conventional banking , there are now Syariah-compliant banking products to meet the short-term and long-term banking needs of the customers.

Islamic banking is based on the principles of Syariah law. The Islamic banking system offers similar functions and services as the conventional banking system while abiding by Syariah principles.

There are two basic principles underlying Islamic banking:

- 1.The prohibition of riba (interest ); and

- 2.The sharing of profit and loss between a bank and its customers.

The operations of Islamic financial institutions are based on a profit- and loss-sharing principle. An Islamic bank does not charge any interest for the financing offered to customers but rather participates in yield, resulting from the use of funds. On the other hand, depositors get their share from the bank’s profit based on a predetermined ratio.

With the growth of Islamic finance, banks are now introducing various riba-free products and services to expand the banking scope and customer base.

1.1 Definition of Islamic Banking

An Islamic bank is a financial institution that operates with the objective to implement the economic and financial principles of Islam in the banking arena. Islamic banking has been defined in a number of ways.

The definition of an Islamic bank, as approved by the General Secretariat of the Organisation of the Islamic Conference (OIC), is stated in the following manner:

An Islamic bank is a financial institution whose statutes, rules and procedures expressly state its commitment to the principle of Syariah and to the banning of the receipt and payment of interest on any of its operations…. (Ali and Sarkar 1995)

According to the Islamic Banking Act 1983 , Malaysia, an Islamic bank is

…a company which carries on Islamic banking business. Islamic banking business means banking business whose aims and operations do not involve any element which is not approved by the religion of Islam…. (Islamic Banking Act 1983 )

The above definition was too generic and there was no exact definition of banking business. This is replaced by the new Islamic Financial Services Act (IFSA) 2013, and the revised definition under section 2 ‘Islamic banking business’ means the business of:

- (a)Accepting Islamic deposits on current account , deposit account, Saving Account , or other similar accounts, with or without the business of paying or collecting checks drawn by or paid in by customers; or

- (b)Accepting money under an investment account ;

- (c)Provision of finance; and

- (d)Such other business as prescribed under section 3; (http://www.bnm.gov.my/index.php?ch=en_legislation&pg=en_legislation_act&ac=1080)

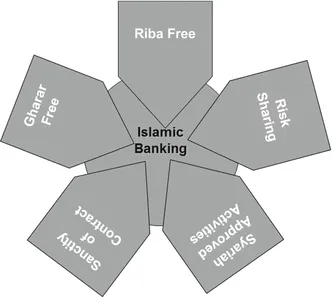

This new Act has defined the Islamic banking business transactions thoroughly. From these definitions, we can summarize that Islamic financial institutions are institutions that are based on Syariah principles . This shall include but not be limited to the following Islamic principles:

- 1.The avoidance of riba (in the broad sense of unjustified increase or interest );

- 2.Prohibition of gharar (uncertainty, risk , speculation);

- 3.Focus on halal (religiously permissible) activities; and

- 4.More generally the quest for justice , and other ethical and religious goals.

In essence, Islamic banking operations are based on Islamic principles for financial transactions, that is, risk-sharing and prohibition of products and services having riba and profit- and loss-sharing are major features, ensuring justice and equity in the economy.

1.2 Islamic Banking Objectives

The primary objective of establishing Islamic banks is to spread economic prosperity within the framework of Islam by promoting and fostering Islamic principles in the business sector. Key objectives are listed below:

- 1.Offer Financial Services: Islamic banking statutes and laws are strictly in line with Syariah principles for financial transactions, where riba and gharar are all identified as un-Islamic. The thrust is toward financing on risk-sharing and strict focus on halal activities. The focus is on offering banking transactions adhering to Syariah principles and avoiding conventional interest-based banking transactions.

- 2.Facilitate Stability in Money Value: Islam recognizes money as a means of exchange and not as a commodity, where there should be a price for its use. Hence, riba-free system leads to stability in the value of money to enable the medium of exchange to be a reliable unit of account.

- 3.Economic Development: Islamic banking fosters economic development through utilities like Musharakah , Mudharabah, and so on, with a unique profit- and loss-sharing principle. This establishes a direct and close relationship between the bank’s return on investment and the successful operation of the business by the entrepreneurs, which in turn leads to the economic development of the country.

- 4.Optimum Resources Allocation: Islamic banking optimizes allocation of scarce resources through investment of financial resources into projects that are considered to be the most profitable, religiously permissible, and are beneficial to the economy.

- 5.Equitable Distribution of Resources: Islamic banking ensures equitable distribution of income and resources among the participating parties—the bank, the depositors , and the entrepreneurs—with its profit-sharing approach which is one of a kind.

- 6.Optimist Approach: Profit-sharing principle encourages banks to go for projects with long-term gains instead of short-term gains. This leads the banks to conduct proper studies before getting into projects, which safeguards both the banks’ and investors’ interests in total. High returns distributed to shareholders maximize the social benefits and bring prosperity to the economy.

1.3 Islamic Banking Principles

The best known feature of Islamic banking is fairness through the sharing of profit and loss and the prohibition of riba . The principles for Islamic banking are listed below:

- Prohibition of RibaRiba is strictly prohibited under Islam and is considered as haram (non-permissible). Islam prohibits Muslims from taking or giving riba regardless of the purpose for which such loans are made and regardless of the rates at which interest rate is charged. Islam allows only one kind of loan and that is Qardhul Hassan (benevolent loan ) whereby the lender does not charge any interest or additional amount over the money lent. Traditional Muslim jurists have construed this principle so strictly that according to one commentator ‘this prohibition applies to any advantage or benefits that the lender might secure out of the qard (loan) such as riding the borrower’s mule, eating at his table, or even taking advantage of the shade of his wall’. The principle derived from the quotation emphasizes that direct or indirect benefits are prohibited.

- Equity ParticipationRiba is prohibited in Islam. Therefore, supplier...