This book demystifies the developments and defines the buzzwords in the wide open space of digitalization and finance, exploring the space of FinTech through the lens of the financial services professional and what they need to know to stay ahead. With chapters focusing on the customer interface, payments, smart contracts, workforce automation, robotics, crypto currencies and beyond, this book aims to be the go-to guide for professionals in financial services and banking on how to better understand the digitalization of their industry.? The book provides an outlook of the impact digitalization will have in the daily work of a CFO/CRO and a structural influence to the financial management (including risk management) department of a bank.

Domande frequenti

Come faccio ad annullare l'abbonamento?

È semplicissimo: basta accedere alla sezione Account nelle Impostazioni e cliccare su "Annulla abbonamento". Dopo la cancellazione, l'abbonamento rimarrà attivo per il periodo rimanente già pagato. Per maggiori informazioni, clicca qui

È possibile scaricare libri? Se sì, come?

Al momento è possibile scaricare tramite l'app tutti i nostri libri ePub mobile-friendly. Anche la maggior parte dei nostri PDF è scaricabile e stiamo lavorando per rendere disponibile quanto prima il download di tutti gli altri file. Per maggiori informazioni, clicca qui

Che differenza c'è tra i piani?

Entrambi i piani ti danno accesso illimitato alla libreria e a tutte le funzionalità di Perlego. Le uniche differenze sono il prezzo e il periodo di abbonamento: con il piano annuale risparmierai circa il 30% rispetto a 12 rate con quello mensile.

Cos'è Perlego?

Perlego è un servizio di abbonamento a testi accademici, che ti permette di accedere a un'intera libreria online a un prezzo inferiore rispetto a quello che pagheresti per acquistare un singolo libro al mese. Con oltre 1 milione di testi suddivisi in più di 1.000 categorie, troverai sicuramente ciò che fa per te! Per maggiori informazioni, clicca qui.

Perlego supporta la sintesi vocale?

Cerca l'icona Sintesi vocale nel prossimo libro che leggerai per verificare se è possibile riprodurre l'audio. Questo strumento permette di leggere il testo a voce alta, evidenziandolo man mano che la lettura procede. Puoi aumentare o diminuire la velocità della sintesi vocale, oppure sospendere la riproduzione. Per maggiori informazioni, clicca qui.

The Impact of Digital Transformation and FinTech on the Finance Professional è disponibile online in formato PDF/ePub?

Sì, puoi accedere a The Impact of Digital Transformation and FinTech on the Finance Professional di Volker Liermann, Claus Stegmann, Volker Liermann, Claus Stegmann in formato PDF e/o ePub, così come ad altri libri molto apprezzati nelle sezioni relative a Business e Finanza. Scopri oltre 1 milione di libri disponibili nel nostro catalogo.

The financial sector and in particular the banks are in a state of upheaval. Haven’t they been continuously for the past twenty or thirty years? Digitalization as a megatrend with all its sub-aspects is hitting all industries and many of the templates for better business generation1 and cost optimization look quite similar across these industries.

What are the fundamental differences between the financial services sector and other industries? The business environment surrounding banks has the additional load of excessive regulation requirements and technology-driven competitors (fintech companies or GAFA2). Depending on the region, other challenges like geopolitical uncertainties, increasing credit risk driven by the end of a long economic cycle or a low-interest rate phase must be added to the business environment.

Before delving further into the details of the banking business environment, we would like to introduce you to the focus of this book, namely the impact on financial professionals. Does the storm taking place in the financial industry effect the financial or risk management department? Will the cacophony of “blockchain, fintech, AI, Zettabyte Era, RPA, …” spouted out by consultants, tech evangelists and other prophets affect the accountant and risk manager? The answer is yes, but to a different extent than other parts of a financial institution are affected.

In this introduction and the first part, we will be looking at aspects of digitalization and fintech companies in more detail to explain the impact on the financial industry. The second and main part of the book will illuminate those aspects from the perspective of a financial department and cover the bank management matters involved. Given the importance of regulation to the industry, we address the regtech dimension in part three. The final part summarizes new and different methods being applied within the environment of financial professionals as well as the technology and architecture considerations. The book ends with summary and outlook in the final chapter.

1.2 Setting the Scene

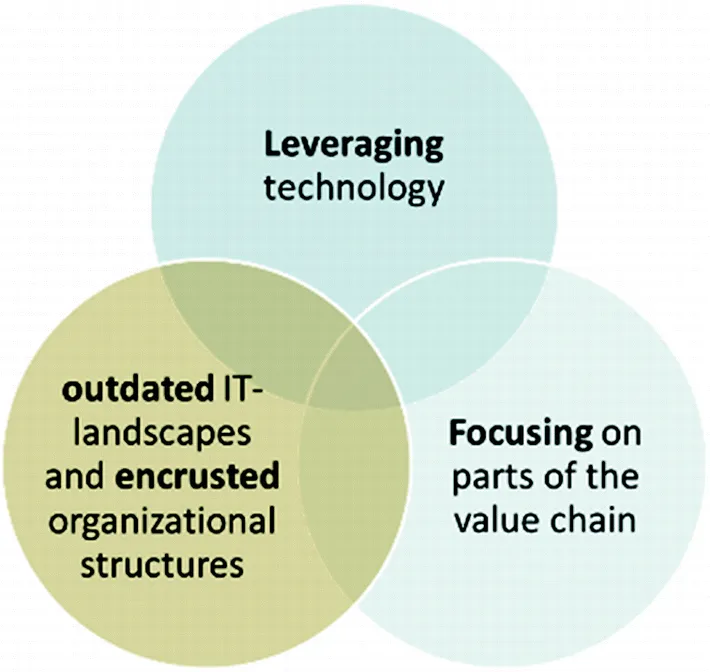

So again, why is digitalization affecting and frightening stakeholders in the financial industry differently than those in other industries? First of all, the competitors (fintech or technology companies) are by nature better in leveraging technology to decrease costs and satisfy customers. Secondly, most competitors focus only on parts of the value chain. Thirdly, the outdated IT landscapes and encrusted organizational structures in traditional banks prevent quick changes. And lastly, the scaling effect of digital business models poses an overwhelming threat.

When it comes to digitalizing business models , there is no guaranteed success if gone alone. Application programming interfaces (APIs) enable traditional banks to compete with new competitors along the entire value chain. The idea behind this consists of establishing a digital financial platform/ecosystem. This is referred to as platform banking, API-based banking or open banking. Platform banking is to some extent driven by the European Payment Services (PSD 2) Directive (EU) 2015/2366 (see The European Parliament and the Council of Union, 2015), which forces European banks to provide access to client’s payment data (naturally only with the client’s consent). Figo is a well-known example of such an API provider (see Figo GmbH, 2019). PSD 2 opens up business opportunities for new market participants, as it makes it much easier to switch banking service providers (Fig. 1).

Fig. 1

What can competitors do better?

Many of the traditional banks, however, have accepted this challenge and are doing well in adopting the strengths of their competitors. The gap in organizational flexibility is being closed using agile methods, albeit only to a minor extent. Technological advance is being absorbed to some extent by way of co-innovation, investment or copying the best parts. The competition is driving banks to rethink their core bands and competencies to focus and reshape their business model. However, outdated IT landscapes and legacy systems are slowing innovation and transformation.

Talk of leveraging technology leads to the question: What will drive the business models of banks in the future? In 2015, Lloyd C. Blankfein, CEO Goldman Sachs, called the company a “technology company” based on the fact that Goldman Sachs has 9000 programmers. David McKay CEO Royal Bank of Canada responded by saying, “If a bank thinks it is a tech company, then it is wrong. We are still business-to-consumer and business-to-business companies, trying to meet customer needs. Banks are using technology to anticipate those needs and meet them in a creative way, but we don’t derive our income from technology” (RBC CEO Dave McKay looks to stay ahead of technology, 2017) (Fig. 2).

Fig. 2

The path of benefit

With regard to technology, the cloud and various cloud strategies 3 require mention. The primary benefits of the cloud include scaling based on changing requirements (timing and changing resources) as well as the associated cost advantage and efficiency. The financial sector still has certain reservations regarding the cloud due to the sensitive data involved and the reputational impact a data leak would cause. Cloudera has an interesting approach to accompany clients from an on-premise environment to a private or public cloud in development over time.

Robert Solow stated in 1987, “You can see the computer age everywhere but in the productivity statistics” (Solow, 1987, July 12). A deeper look at digitalization’s impact on financial institutions could lead to a similar assessment today. The main question is: Do we serve the customer better by using this technology?

To a certain extent, Dan Ariely already summed up big data in 2013 in a way that could now be applied to AI, machine learning, deep learning and blockchain: “Big data is like teenage sex: everyone talks about it, nobody really knows how to do it, everyone thinks everyone else is doing it, so everyone claims they are doing it” (Ariely, 2013, January 6). Banks have to decide if their business model is technology or customer-centric. The latter will be the future!

Design thinking (Brown, 2008, June) puts the client first from the initial stages of the product development process. Concepts like Customer Journey (CJ) and Context Driven Banking (CDB) focus on being there for the customer at the right time.

Fintech companies and technology companies (GAFA) are by far more dynamic (in terms of organizational structure and innovation speed) than traditional financial institutions. Fintech companies are most successful in picking well-chosen parts of the value chain and providing better (i.e., cheaper or more convenient) services. However, these companies are restricted due to their limited capital. A bigger threat is posed by the GAFA companies due to their deep pockets and the ability to change the playing field of a whole industry, like Apple did with the music industry or Google with maps. The impact is already being felt in the payment context in the form of Apple Pay, Google Pay and Alipay.

1.3 Impact on Financial Professionals

Financial and risk management professionals can only contribute to the client-centric business models on a small scale. But they could be less restrictive on business than is currently the case. Financial and risk management have to become more dynamic, adoptable or, to use the digitalization buzzword, “agile.”

The cost saving aspect driven by optimization and automation up to automated decision-making, can significantly improve banks’ stability and agility. The templates for this do not differ much from those applicable to other industries.

The twofold impact of digitalization is illustrated in Fig. 3. Banks in Europe are suffer...