The essential resource for fraud examiners around the globe

The International Fraud Handbook provides comprehensive guidance toward effective anti-fraud measures around the world. Written by the founder and chairman of the Association of Certified Fraud Examiners (ACFE), this book gives examiners a one-stop resource packed with authoritative information on cross-border fraud investigations, examination methodology, risk management, detection, prevention, response, and more, including new statistics from the ACFE 2018 Report to the Nations on Occupational Fraud and Abuse that reveal the prevalence and real-world impact of different types of fraud. Examples and detailed descriptions of the major types of fraud demonstrate the various manifestations examiners may encounter in organizations and show readers how to spot the "red flags" and develop a robust anti-fraud program.

In addition, this book includes jurisdiction-specific information on the anti-fraud environment for more than 35 countries around the globe. These country-focused discussions contributed by local anti-fraud experts provide readers with the information they need when conducting cross-border engagements, including applicable legal and regulatory requirements, the types and sources of information available when investigating fraud, foundational anti-fraud frameworks, cultural considerations, and more.

The rising global economy brings both tremendous opportunity and risks that are becoming increasingly difficult to manage. As a result, many jurisdictions are attempting to strengthen their anti-fraud environments — whether through stricter anti-bribery laws or more stringent risk management guidelines — but a lack of uniformity in legal rules and guidance can be challenging for organizations doing business abroad. This book helps examiners mitigate fraud in their own organizations, while taking the necessary steps to prevent potential legal exposure.

Understand the different types of fraud, their common elements, and their impacts across an organization

Conduct a thorough risk assessment and implement effective response and control activities

Learn the ACFE's standard investigation methodology for domestic and cross-border fraud investigations

Explore fraud trends and region-specific information for countries on every continent

As levels of risk increase and the risks themselves become more complex, the International Fraud Handbook gives examiners a robust resource for more effective prevention and detection.

Domande frequenti

Come faccio ad annullare l'abbonamento?

È semplicissimo: basta accedere alla sezione Account nelle Impostazioni e cliccare su "Annulla abbonamento". Dopo la cancellazione, l'abbonamento rimarrà attivo per il periodo rimanente già pagato. Per maggiori informazioni, clicca qui

È possibile scaricare libri? Se sì, come?

Al momento è possibile scaricare tramite l'app tutti i nostri libri ePub mobile-friendly. Anche la maggior parte dei nostri PDF è scaricabile e stiamo lavorando per rendere disponibile quanto prima il download di tutti gli altri file. Per maggiori informazioni, clicca qui

Che differenza c'è tra i piani?

Entrambi i piani ti danno accesso illimitato alla libreria e a tutte le funzionalità di Perlego. Le uniche differenze sono il prezzo e il periodo di abbonamento: con il piano annuale risparmierai circa il 30% rispetto a 12 rate con quello mensile.

Cos'è Perlego?

Perlego è un servizio di abbonamento a testi accademici, che ti permette di accedere a un'intera libreria online a un prezzo inferiore rispetto a quello che pagheresti per acquistare un singolo libro al mese. Con oltre 1 milione di testi suddivisi in più di 1.000 categorie, troverai sicuramente ciò che fa per te! Per maggiori informazioni, clicca qui.

Perlego supporta la sintesi vocale?

Cerca l'icona Sintesi vocale nel prossimo libro che leggerai per verificare se è possibile riprodurre l'audio. Questo strumento permette di leggere il testo a voce alta, evidenziandolo man mano che la lettura procede. Puoi aumentare o diminuire la velocità della sintesi vocale, oppure sospendere la riproduzione. Per maggiori informazioni, clicca qui.

International Fraud Handbook è disponibile online in formato PDF/ePub?

Sì, puoi accedere a International Fraud Handbook di Joseph T. Wells in formato PDF e/o ePub, così come ad altri libri molto apprezzati nelle sezioni relative a Negocios y empresa e Contabilidad internacional. Scopri oltre 1 milione di libri disponibili nel nostro catalogo.

In the world of commerce, organizations incur costs to produce and sell their products or services. These costs run the gamut: labor, taxes, advertising, occupancy, raw materials, research and development, and, yes, fraud and abuse. The latter cost, however, is fundamentally different from the former: the true expense of fraud and abuse is hidden, even if it is reflected in the profit-and-loss figures.

For example, suppose a company’s advertising expense is $1.2 million. But unknown to the company’s executives, the marketing manager is colluding with an outside ad agency and has accepted $300,000 in kickbacks to steer business to that firm. That means the true advertising expense is overstated by at least the amount of the kickbacks – if not more. The result, of course, is that $300,000 comes directly off the bottom line, out of the pockets of the investors and the workforce. Similarly, if a warehouse foreman is stealing inventory or an accounting clerk is skimming customer payments, the company suffers a loss – one it likely does not know about, but one that must be absorbed somewhere.

The truth is, fraud can occur in virtually any organization. If an organization employs individuals, at some point one or more of those individuals will attempt to lie, cheat, or steal from the company for personal gain. So this hidden cost – one that offers no benefit to the company and, in fact, causes numerous kinds of damage to the company even beyond the direct financial consequence – is one that all organizations, in all countries, in all industries, and of all sizes, will encounter. However, the risk of fraud is most significant – that is, it has the potential to cause the most damage – for organizations that are unaware of, ignore, or underestimate whether and how fraud can occur within their operations.

The risk is also evolving due to changes in technology, globalization, regulatory environments, and other factors. These changes can present challenges to those charged with preventing, detecting, investigating, and responding to fraud. Nonetheless, the concepts behind fraud remain timeless – the perpetrators seek to trick victims out of financial or other resources for personal gain. As a result, the foundational concepts in fighting fraud are still effective.

WHAT IS FRAUD?

The term fraud is commonly used to encompass a broad range of schemes: employee embezzlement, identity theft, corrupt government officials, cybercrimes, fraud against the elderly, health care schemes, loan fraud, bid rigging, credit card skimming, counterfeit goods, and dozens of others. While the range of schemes that fall under the umbrella of fraud is extensive, a general definition and an understanding of the common elements of these schemes are useful in preventing and detecting these acts.

Fraud can be generally defined as any crime for gain that uses deception as its principal modus operandi. Consequently, fraud includes any intentional or deliberate act to deprive another of property or money by guile, deception, or other unfair means. As such, all types of fraud have the following common elements:

A material false statement (i.e., a misrepresentation)

Knowledge that the statement was false when it was uttered (i.e., intent)

The victim’s reliance on the false statement

Damages resulting from the victim’s reliance on the false statement

Components of Fraud

An act of fraud normally involves three components, or steps:

The act

The concealment

The conversion

To successfully perpetrate a fraud, offenders generally must complete all three steps: they must commit the act, conceal the act, and convert the proceeds for their personal benefit or the benefit of another party.

The Act

The fraud act is normally the theft or deception – the action that leads to the gain the perpetrator is seeking.

The Concealment

Once the perpetrator accomplishes the act, the individual typically makes efforts to conceal it. Concealment is a cornerstone of fraud. As opposed to traditional criminals, who make no effort to conceal their crimes, fraud perpetrators typically take steps to keep their victims ignorant. For example, in the case of the theft of cash, falsifying the balance in the cash account would constitute concealment. Although some individuals commit fraud without attempting to conceal it (e.g., taking cash from a register drawer with no attempt to cover the theft), fraud investigations generally uncover such schemes quickly, reducing the perpetrator’s chances of repeating the offense and increasing the likelihood of being caught.

The Conversion

After completing and concealing the fraudulent act, the perpetrator must convert the ill-gotten gains for the individual’s own benefit or the benefit of another party. In the case of the theft of petty cash, conversion generally occurs when the perpetrator deposits the funds into the individual’s own account or makes a purchase with the stolen funds.

WHAT FACTORS LEAD TO FRAUD?

Individuals and groups perpetrate frauds to obtain money, property, or services; to avoid payment or loss of services; or to secure personal or business advantage. However, most people who commit fraud against their employers are not career criminals. In fact, the vast majority are trusted employees who have no criminal history and who do not consider themselves to be lawbreakers. So the question is: What factors cause these otherwise normal, law-abiding individuals to commit fraud?

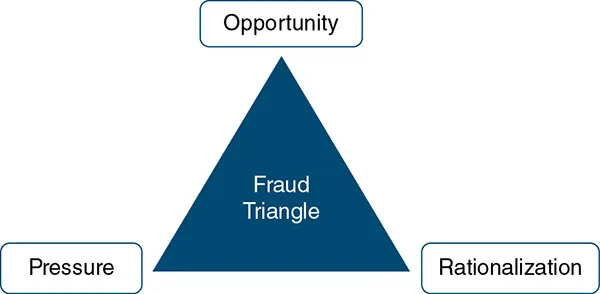

The Fraud Triangle

The best and most widely accepted model for explaining why people commit fraud is the Fraud Triangle. (See Exhibit 1.1.) Dr. Donald Cressey, a criminologist whose research focused on embezzlers (whom he called trust violators), developed this model.

Exhibit 1.1The Fraud Triangle

According to Cressey, three factors must be present at the same time for an ordinary person to commit fraud:

Pressure

Perceived opportunity

Rationalization

Pressure

The first leg of the Fraud Triangle represents pressure. This is what motivates the crime in the first place. The individuals might have a financial problem they are unable to solve through legitimate means, so they begin to consider committing an illegal act, such as stealing cash or falsifying a financial statement. The pressure can be personal (e.g., too deep in personal debt) or professional (e.g., job or business in jeopardy).

Examples of pressures that commonly lead to fraud include:

Inability to pay one’s bills

Drug or gambling addiction

Need to meet earnings forecast to sustain investor confidence

Need to meet productivity targets at work

Desire for status symbols, such as a bigger house or nicer car

Opportunity

The second leg of the Fraud Triangle is opportunity, sometimes referred to as perceived opportunity, which defines the method by which an individual can commit the crime. The person must see some way to use (abuse) a position of trust to solve a financial problem with a low perceived risk of getting caught.

It is critical that fraud perpetrators believe they can solve their problem in secret. Many people commit white-collar crimes to maintain their social status. For instance, they might steal to conceal a drug p...