The Black-Scholes-Merton option model was the greatest innovation of 20th century finance, and remains the most widely applied theory in all of finance. Despite this success, the model is fundamentally at odds with the observed behavior of option markets: a graph of implied volatilities against strike will typically display a curve or skew, which practitioners refer to as the smile, and which the model cannot explain. Option valuation is not a solved problem, and the past forty years have witnessed an abundance of new models that try to reconcile theory with markets.

The Volatility Smile presents a unified treatment of the Black-Scholes-Merton model and the more advanced models that have replaced it. It is also a book about the principles of financial valuation and how to apply them. Celebrated author and quant EmanuelDerman and Michael B. Miller explain not just the mathematics but the ideas behind the models. By examining the foundations, the implementation, and the pros and cons of various models, and by carefully exploring their derivations and their assumptions, readers will learn not only how to handle the volatility smile but how to evaluate and build their own financial models.

Topics covered include:

The principles of valuation

Static and dynamic replication

The Black-Scholes-Merton model

Hedging strategies

Transaction costs

The behavior of the volatility smile

Implied distributions

Local volatility models

Stochastic volatility models

Jump-diffusion models

The first half of the book, Chapters 1 through 13, can serve as a standalone textbook for a course on option valuation and the Black-Scholes-Merton model, presenting the principles of financial modeling, several derivations of the model, and a detailed discussion of how it is used in practice. The second half focuses on the behavior of the volatility smile, and, in conjunction with the first half, can be used for as the basis for a more advanced course.

Domande frequenti

Come faccio ad annullare l'abbonamento?

È semplicissimo: basta accedere alla sezione Account nelle Impostazioni e cliccare su "Annulla abbonamento". Dopo la cancellazione, l'abbonamento rimarrà attivo per il periodo rimanente già pagato. Per maggiori informazioni, clicca qui

È possibile scaricare libri? Se sì, come?

Al momento è possibile scaricare tramite l'app tutti i nostri libri ePub mobile-friendly. Anche la maggior parte dei nostri PDF è scaricabile e stiamo lavorando per rendere disponibile quanto prima il download di tutti gli altri file. Per maggiori informazioni, clicca qui

Che differenza c'è tra i piani?

Entrambi i piani ti danno accesso illimitato alla libreria e a tutte le funzionalità di Perlego. Le uniche differenze sono il prezzo e il periodo di abbonamento: con il piano annuale risparmierai circa il 30% rispetto a 12 rate con quello mensile.

Cos'è Perlego?

Perlego è un servizio di abbonamento a testi accademici, che ti permette di accedere a un'intera libreria online a un prezzo inferiore rispetto a quello che pagheresti per acquistare un singolo libro al mese. Con oltre 1 milione di testi suddivisi in più di 1.000 categorie, troverai sicuramente ciò che fa per te! Per maggiori informazioni, clicca qui.

Perlego supporta la sintesi vocale?

Cerca l'icona Sintesi vocale nel prossimo libro che leggerai per verificare se è possibile riprodurre l'audio. Questo strumento permette di leggere il testo a voce alta, evidenziandolo man mano che la lettura procede. Puoi aumentare o diminuire la velocità della sintesi vocale, oppure sospendere la riproduzione. Per maggiori informazioni, clicca qui.

The Volatility Smile è disponibile online in formato PDF/ePub?

Sì, puoi accedere a The Volatility Smile di Emanuel Derman, Michael B. Miller in formato PDF e/o ePub, così come ad altri libri molto apprezzati nelle sezioni relative a Business e Trading. Scopri oltre 1 milione di libri disponibili nel nostro catalogo.

Financial models in light of the great financial crisis.

The difficulties of option valuation.

An introduction to the volatility smile.

Financial science and financial engineering.

The purpose and use of models.

Introduction

Our primary aim in this book is to provide the reader with an accessible, not-too-sophisticated introduction to models of the volatility smile. Prior to the 1987 global stock market crash, the Black-Scholes-Merton (BSM) option valuation model seemed to describe option markets reasonably well. After the crash, and ever since, equity index option markets have displayed a volatility smile, an anomaly in blatant disagreement with the BSM model. Since then, quants around the world have labored to extend the model to accommodate this anomaly. Our main focus in this book will be the theory of option valuation, the study of the BSM model and its limitations, and a detailed introduction to the extensions of the BSM model that attempt to rectify its problems. Most of the book is devoted to these topics.

A secondary motivation for writing this book originates in the great financial crisis of 2007–2008, which began with the collapse of the mortgage collateralized debt obligation (CDO) market, whose structured credit products were valued using financial engineering techniques. When the crisis began, some pundits blamed the practice of financial engineering for the mortgage market's meltdown. Paul Volcker, whose grandson was a financial engineer, wrote the following paragraph as part of an otherwise sensible speech he gave in 2009:

A year or so ago, my daughter had seen . . . some disparaging remarks I had made about financial engineering. She sent it to my grandson, who normally didn't communicate with me very much. He sent me an email, “Grandpa, don't blame it on us! We were just following the orders we were getting from our bosses.” The only thing I could do was send him back an email, “I will not accept the Nuremberg excuse.”

Comparing financial modelers to Nazi war criminals seems extreme, and indeed, since then, opinions about modelers' responsibility for the financial meltdown have become more nuanced. Spain and Ireland developed housing market bubbles that, unlike those in the United States, were not inflated by complex financially engineered products. Paul Krugman has suggested that the root cause of the crisis lay in the West's rapid withdrawal of capital from Asia after the currency crisis of 1998, leading Asian countries thereafter to concentrate on exporting, saving, and hoarding, which led them to provide cheap credit that fueled speculation. Other competing explanations abound. As with all complex human events, it's impossible to pinpoint a single cause.

Nevertheless, models did play a part in the development of the crisis. In the face of very low safe yields, badly engineered financial models were indeed used to tempt investors—at times misleadingly and deceptively—into buying structured CDOs that promised optimistically high yields. Though our expertise lies in models for option valuation rather than mortgage securities, we also wanted to write a book that illustrates how to be sensible about model building.

The Black-Scholes-Merton Model and Its Discontents

Stephen Ross of MIT, one of the inventors of the binomial option valuation model and the theory of risk-neutral valuation, once wrote: “When judged by its ability to explain the empirical data, option pricing theory is the most successful theory not only in finance, but in all of economics” (Ross 1987). But even this most successful of models is far from being perfect.

Finance academics tend to think of option valuation as a solved problem, of little current interest. But readers of this book who end up working as practitioners—on options trading desks in equities, fixed income, currencies, or commodities, as risk managers or controllers or model auditors—will find that the valuation of options isn't really a solved problem at all. Financial markets disrespect the traditional BSM formula even while they employ its flawed language to communicate with each other. Practitioners and traders who are responsible for coming up with the prices at which they are willing to trade derivative securities, especially exotic illiquid derivatives, grapple with appropriate valuation every day. They have to figure out how to amend the BSM model to cope with an actual market that violates its assumptions, and they have to keep finding new ways of doing so as the market modifies its behavior based on its experiences.

In this book we're going to focus on the BSM model and its discontents. In one sense the BSM model is a miracle: It lets you value, in a totally rational way, securities that before its existence had no plausible or defensible theoretical value at all. In the Platonic world of BSM—a world with normally distributed returns, geometric Brownian motion for stock prices, unlimited liquidity, continuous hedging, and no transaction costs—their model provides a method of dynamically synthesizing an option. It's a masterpiece of engineering in an imaginary world that doesn't quite exist, because markets don't obey all of its assumptions. It's a miracle, but it's only a model, and not reality.

Some of the BSM assumptions are violated in minor ways, some more dramatically. The assumption that you can hedge continuously, at zero transaction cost, is an approximation we can adjust for, as we will illustrate in later chapters. Skilled traders and quants do this with a mix of estimation and intuition every day. You can, for example, heuristically allow for transaction costs by adding some dollars to your option price, or some volatility points to the BSM formula. In that sense the model is robust—you can perturb it from its Platonic view of the world to approximate the messiness of actual markets.

Other BSM assumptions are violated in more significant ways. For example, stock prices don't actually follow geometric Brownian motion. They can jump, their distributions have fat tails, and their volatility varies unpredictably. Adjusting for these more significant violations is not always easy. We will tackle many of these difficulties in this book.

In the end, the BSM model sounds so rational, and has such a strong grip on everyone's imagination, that even people who don't believe in its assumptions nevertheless use it to quote prices at which they are willing to trade.

A Quick Look at the Implied Volatility Smile

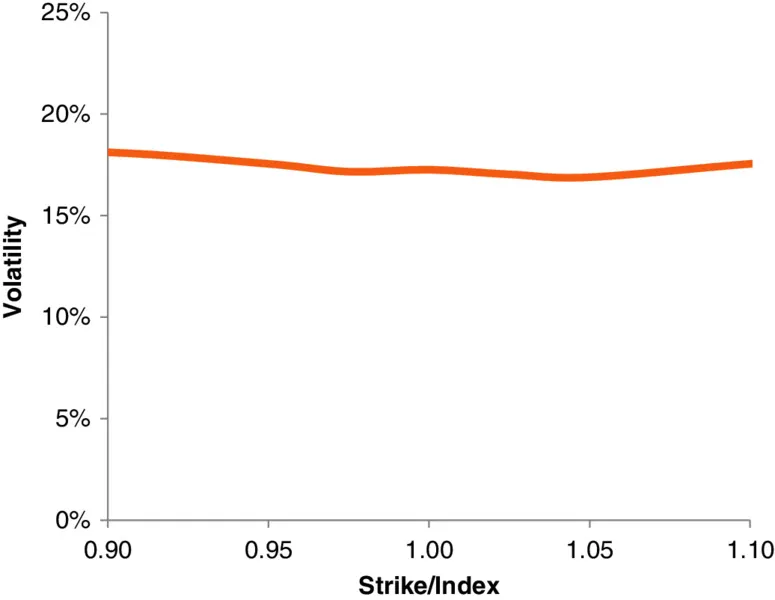

The BSM model assumes that a stock's future return volatility is constant, independent of the strike and time to expiration of any option on that stock. Were the model correct, a plot of the implied BSM volatilities for options with the same expiration over a range of strikes would be a flat line. Figure 1.1 shows what three-month equity index implied volatilities looked like before the Black Monday stock market crash of 1987.

Figure 1.1 Representative S&P 500 Implied Volatilities prior to 1987

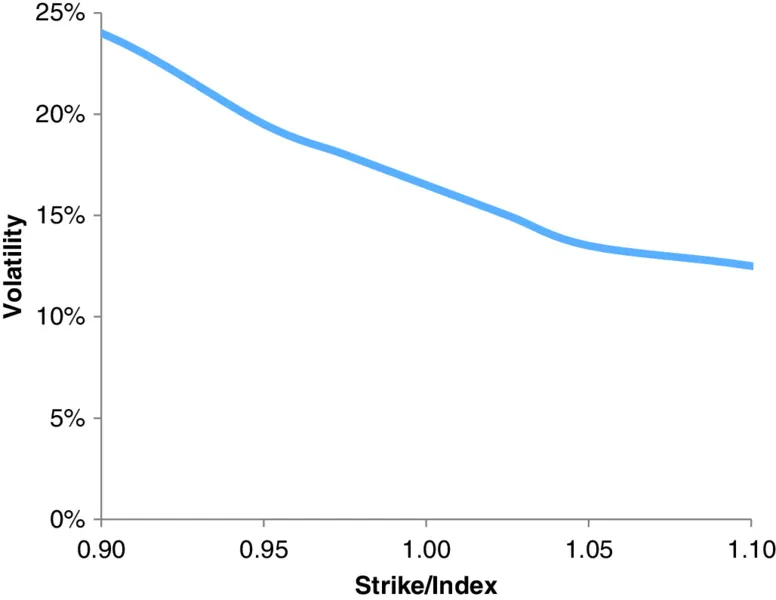

Prior to the crash, therefore, the BSM model seemed to describe the option market rather well, at least with respect to variation in strikes. Figure 1.2 shows typical three-month implied volatilities after the crash of 1987. Even though all the options used to generate the smile were written on the same underlier, each option had a different implied volatility. This is inconsistent with the BSM model, which assumes that implied volatility is a forecast of actual volatility, for which there can be only one value. You can think of options as metaphorical photographs of the stock's future volatility, taken from different angles or elevations. While photographs of a building taken from different points might look different, the actual size of a building remains the same. In a similar way, if the BSM model were truly reliable, the implied volatility of the stock would be the same, no matter which option you chose to view it with. The option price is derived from the stock price, but the stock's volatility should not depend on the option.

Figure 1.2 Representative S&P 500 Implied Volatilities after 1987

Though the smile appeared most dramatically in equity index option markets after the 1987 crash, there had always been a slight smile in currency option markets, a smile in the literal sense that the implied volatilities as a function of strike resembled one:

. As depicted in Figure 1.2, the equity “smile” is really more a skew or a smirk, but practitioners have persisted in using the word smile to describe the relationship between implied volatilities and strikes, irrespective of the actual shape. The smile's appearance after the 1987 crash was clearly connected with the visceral shock upon discovering, for the first time since 1929, that a giant market could suddenly drop by 20% or more in a day. Market participants immediately drew the conclusion that an investor should pay more for low-strike puts than for high-strike calls.

Since the crash of 1987, the volatility smile has spread to most other option markets (currencies, fixed income, commodities, etc.), but in each market it has taken its own characteristic form and shape. Traders and quants in every product area have had to model the smile in their own market. At many firms, not only does each front-office trading desk have its own particular smile models, but the firm-wide risk management group is likely to have its own models as well. The modeling of the volatility smile is likely one of the largest sources of model risk within finance.

No-Nonsense Financial Modeling

During the past 20 years there has been a tendency for quantitative finance and asset pricing to become increasingly formal and axiomatic. Many textbooks postulate mathematical axioms for finance and then derive the consequences. In this book, though, we're studying financial engineering, not mathematical finance. The ideas and the models are at least as important as the mathematics. The more math you know, the better, but math is the syntax, not the semantics. Paul Dirac, the discoverer of the Dirac equation who first predicted the existence of antiparticles, had a good point when he said:

I am not interested in proofs, but only in what nature does.

—Paul Dirac

About Theorems and Laws

Mathematics requires axioms and postulates, from which mathematicians then derive the logical consequences. In geometry, for example, Euclid's axioms are meant to describe self-evident relationships of parts of things to the whole, and his postulates further describe supposedly self-evident properties of points and lines. One Euclidean axiom is that things that are equal to the same thing are equal to each other. One Euclidean postulate, for example, is that it is always possible to draw a straight line between any two points.

Euclid's points and lines are abstracted from those of nature. When you get familiar enough with the abstractions, they seem almost tangible. Even more esoteric abstractions—infinite-dimensional Hilbert spaces that form the mathematical basis of quantum mechanics, for example—seem real and visualizable to mathematicians. Nevertheless, ...