![]()

Chapter 1

Introduction to Risk

The risk management department was one of the fastest growing areas in investment and commercial banks during the 1990s, and again after the crash of 2008. A string of high-profile banking losses and failures, typified by the fall of Barings Bank in 1995, highlighted the importance of risk management to bank managers and shareholders alike. In response to the volatile and complex nature of risks that they were exposed to, banks set up specialist risk management departments, whose functions included both measuring and managing risk. As a value-added function, risk management can assist banks not only in managing risk, but also in understanding the nature of their profit and loss, and so help increase return on capital. It is now accepted that senior directors of banks need to be thoroughly familiar with the concept of risk management. One of the primary tools of the risk manager is value-at-risk (VaR), which is a quantitative measure of the risk exposure of an institution. For a while VaR was regarded as somewhat inaccessible, and only the preserve of mathematicians and quantitative analysts. Although VaR is indeed based on statistical techniques that may be difficult to grasp for the layman, its basic premise can, and should, be explained in straightforward fashion, in a way that enables non-academics to become comfortable with the concept. The problem with VaR is that while it was only ever a measure, based on some strong assumptions, of approximate market risk exposure (it is unsuited to measuring risk exposure in the banking book), it suffers in the eyes of its critics in having the cachet of science. This makes it arcane and inaccessible, while paradoxically being expected to be much more accurate than it was ever claimed to be. Losses suffered by banks during the crash of 2007–08 were much larger than any of their VaR values, which is where the measure comes in for criticism. But we can leave that aside for now, and concentrate just on introducing the technicalities.

Later in the book we describe and explain the calculation and application of VaR. We begin here with a discussion of risk.

Defining Risk

Any transaction or undertaking with an element of uncertainty as to its future outcome carries an element of risk: risk can be thought of as uncertainty. To associate particular assets such as equities, bonds or corporate cash flows with types of risk, we need to define ‘risk’ itself. It is useful to define risk in terms of a risk horizon, the point at which an asset will be realised, or turned into cash. All market participants, including speculators, have an horizon, which may be as short as a half-day. Essentially then, the horizon is the time period relating to the risk being considered.

Once we have established a notion of horizon, a working definition of risk is the uncertainty of the future total cash value of an investment on the investor's horizon date. This uncertainty arises from many sources. For participants in the financial markets risk is essentially a measure of the volatility of asset returns, although it has a broader definition as being any type of uncertainty as to future outcomes. The types of risk that a bank or securities house is exposed to as part of its operations in the bond and capital markets are characterised below.

The Elements of Risk: Characterising Risk

Banks and other financial institutions are exposed to a number of risks during the course of normal operations. The different types of risk are broadly characterised as follows:

- Market risk – risk arising from movements in prices in financial markets. Examples include foreign exchange (FX) risk, interest rate risk and basis risk. In essence market risk applies to ‘tradeable’ instruments, ones that are marked-to-market in a trading book, as opposed to assets that are held to maturity, and never formally repriced, in a banking book.

- Credit risk – something called issuer risk refers to risk that a customer will default. Examples include sovereign risk, marginal risk and force majeure risk.

- Liquidity risk – this refers to two different but related issues: for a Treasury or money markets’ person, it is the risk that a bank has insufficient funding to meet commitments as they arise. That is, the risk that funds cannot be raised in the market as and when required. For a securities or derivatives trader, it is the risk that the market for assets becomes too thin to enable fair and efficient trading to take place. This is the risk that assets cannot be sold or bought as and when required. We should differentiate therefore between funding liquidity and trading liquidity whenever using the expression liquidity.

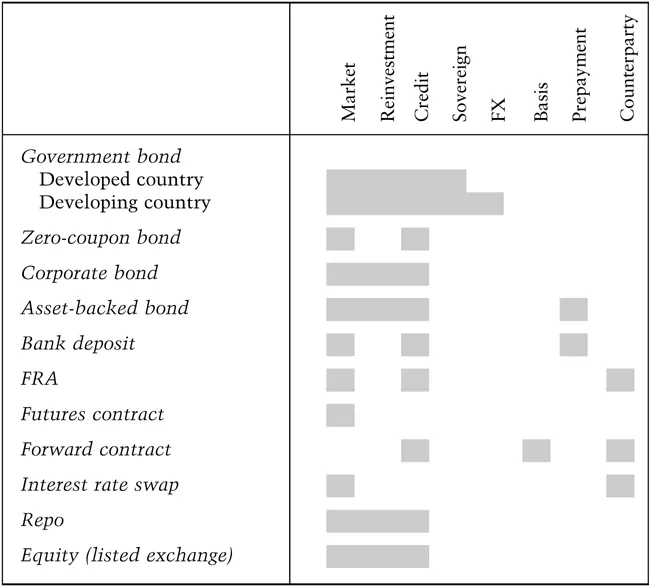

- Operational risk – risk of loss associated with non-financial matters such as fraud, system failure, accidents and ethics. Table 1.1 assigns sources of risk for a range of fixed interest, FX, interest rate derivative and equity products. The classification has assumed a 1-year horizon, but the concepts apply to any time horizon.

Forms of market risk

Market risk reflects the uncertainty as to an asset's price when it is sold. Market risk is the risk arising from movements in financial market prices. Specific market risks will differ according to the type of asset under consideration:

- Currency risk – this arises from exposure to movements in FX rates. A version of currency risk is transaction risk, where currency fluctuations affect the proceeds from day-to-day transactions.

- Interest rate risk – this arises from the impact of fluctuating interest rates and will directly affect any entity borrowing or investing funds. The most common exposure is simply to the level of interest rates but some institutions run positions that are exposed to changes in the shape of the yield curve. The basic risk arises from revaluation of the asset after a change in rates.

- Equity risk – this affects anyone holding a portfolio of shares, which will rise and fall with the level of individual share prices and the level of the stock market.

- Other market risk – there are residual market risks which fall in this category. Among these are volatility risk, which affects option traders, and basis risk, which has a wider impact. Basis risk arises whenever one kind of risk exposure is hedged with an instrument that behaves in a similar, but not necessarily identical manner. One example would be a company using 3-month interest rate futures to hedge its commercial paper (CP) programme. Although eurocurrency rates, to which futures prices respond, are well correlated with CP rates, they do not invariably move in lock step. If CP rates moved up by 50 basis points but futures prices dropped by only 35 basis points, the 15-bps gap would be the basis risk in this case.

Other risks

- Liquidity risk – in banking, this refers to the risk that a bank cannot raise funds to refinance loans as the original borrowing becomes past due. It is sometimes also referred to as rollover risk. In other words, it refers to the risk of an inability to continue to raise funds to replace maturing liabilities. There is also another (related) liquidity risk, which refers to trading liquidity. This is the risk that an asset on the balance sheet cannot be sold at a previously perceived fair value, or cannot be sold at all, and hence experiences illiquidity.

- Credit risk – the risk that an obligor (the entity that has borrowed funds from you) defaults on the loan repayments.

- Counterparty risk – all transactions involve one or both parties in counterparty risk, the potential loss that can arise if one party were to default on its obligations. Counterparty risk is most relevant in the derivatives market, where every contract is marked-to-market daily and so a positive MTM is taken to the profit & loss (P&L) account. If the counterparty defaults before the contract has expired, there is risk that the actual P&L will not be realized. In the credit derivatives market, a counterparty that has sold protection on the third-party reference name on the credit derivative contract and which subsequently defaults will mean the other side to the trade is no longer protected against the default of that third party.

- Reinvestment risk – if an asset makes any payments before the investor's horizon, whether it matures or not, the cash flows will have to be reinvested until the horizon date. Since the reinvestment rate is unknown when the asset is purchased, the final cash flow is uncertain.

- Sovereign risk – this is a type of credit risk specific to a government bond. Post 2008, there is material risk of default by an industrialised country. A developing country may default on its obligation (or declare a debt ‘moratorium') if debt payments relative to domestic product reach unsustainable levels.

- Prepayment risk – this is specific to mortgage-backed and asset-backed bonds. For example, mortgage lenders allow the homeowner to repay outstanding debt before the stated maturity. If interest rates fall prepayment will occur, which forces reinvestment at rates lower than the initial yield.

- Model risk – some financial instruments are heavily dependent on complex mathematical models for pricing and hedging. If the model is incorrectly specified, is based on questionable assumptions or does not accurately reflect the true behaviour of the market, banks trading these instruments could suffer extensive losses.

Risk estimation

There are a number of different ways of approaching the estimation of market risk. The key factors determining the approach are the user's response to two questions:

- Can the user accept the assumption of normality – is it reasonable to assume that market movements follow the normal distribution? If so, statistical tools can be employed.

- Does the value of positions change linearly with changes in market prices? If not (as is typical for option positions where market movements are not very small), simulation techniques will be more useful.

Were the answers to both questions to be ‘yes’ then we could be comfortable using standard measures of risk such as duration and convexity (these concepts are covered later). If the answers are ‘no’ then we are forced to use scenario analysis combined with simulation techniques. If, as is more likely, the answer to the first question is ‘yes’ and the second ‘no’, then a combination of statistical tools and simulation techniques will be required.

For most banks and securities houses the portfolio will almost certainly behave in a non-linear manner because that is the nature of financial markets. Hence, a combination of statistical tools and simulation is likely to be the most effective risk measurement approach. The scenarios used in simulations are often a mixture of observed rate and price changes from selected periods in the past, and judgement calls by the risk manager. The various alternative methods are examined in Chapter 3.

Risk Management

The risk management function grew steadily in size and importance within commercial and investment banks during the 1990s. Risk management departments exist not to eliminate the possibility of all risk, should such action indeed be feasible or desirable; rather, to control the frequency, extent and size of such losses in such a way as to provide the minimum surprise to senior management and shareholders.

Risk exists in all competitive business although the balance between financial risks of the type described above and general ...