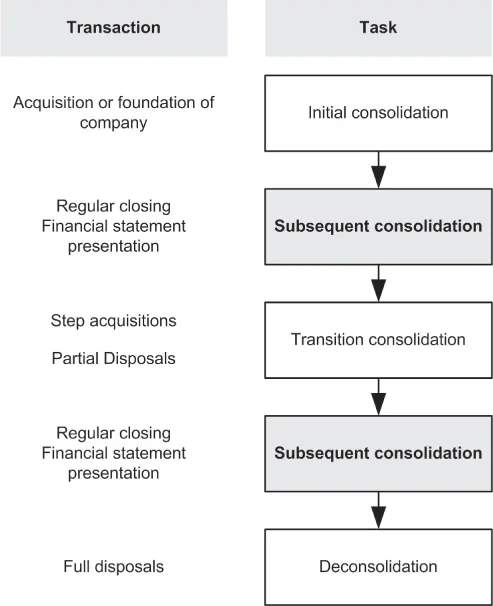

The new International Financial Reporting Standards (IFRS) 10, 11, and 12 are changing group accounting for many businesses. As business becomes increasingly global, more and more firms will need to transition using the codes and techniques described in Principles of Group Accounting under IFRS. This book is a practical guide and reference to the standards related to consolidated financial statements, joint arrangements, and disclosure of interests. Fully illustrated with a step-by-step case study, Principles of Group Accounting under IFRS is equally valuable as an introductory text and as a reference for addressing specific issues that may arise in the process of consolidating group accounts.

The new international standards will bring about significant changes in group reporting, and it is essential for accountants, auditors, and business leaders to understand their implications. Author Andreas Krimpmann is an internationally recognized authority on the transition from GAAP to IFRS, and this new text comes packaged with GAAP/IFRS comparison resources that will help make the changes clear. Other bonus resources include an Excel-based consolidation tool, checklists, and a companion website with the latest information. Learn about:

- Definitions, requirements, processes, and transition techniques for IFRS 10, 11, and 12 covering group level accounting

- Practical implementation strategies demonstrated through a clear case study of a midsize group

- Key concepts related to consolidated financial statements, joint ventures, management consolidation, and disclosure of interests

- Comparisons between GAAP and IFRS to clarify the required changes for international firms

Whatever stage of the consolidation process you are in, you will appreciate the professional perspective in Principles of Group Accounting under IFRS.