The only book on the market specifically designed to help audit staff stay ahead of inspectors

This comprehensive, practical, and theoretical guide covers the key ISAs that underpin audit methodologies and the recently revised ISAs that cause practitioners the most concern. It is designed to enhance auditors' understanding of critical ISAs, reducing their dependence on methodologies to mediate and explain ISA requirements. Using plenty of examples, the book helps audit staff learn to tailor audit methodologies and remove redundancies, as well as form high-quality judgments with a thorough grounding in ISA to serve in discussions with file reviewers and audit inspectors.

Features practical examples that appeal to auditors with technical responsibilities

Covers key topics such as smaller audits, management override of controls, documenting judgments, and dealing with accounting estimates and written presentations

Ideal for practitioners in companies and accounting firms, as well as auditing students

Includes access to a companion website with constantly updating ISAs and case studies

Mixing theory with practical examples, Core Auditing Standards for Practitioners provides experienced audit staff with key ISA-related information they need to succeed.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

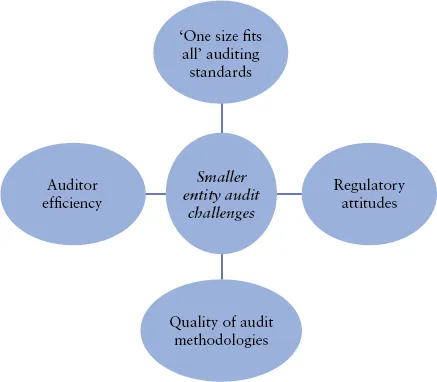

There is a bigger difference between smaller entity audits and larger ones than ISAs imply. Such audits are not given a great deal of coverage by standard-setters or regulators but practitioners know that they can be difficult to perform efficiently. Some practitioners are very comfortable with them; others are not, for a number of reasons. There are issues with the auditing standards themselves, which are supposed to accommodate audits of all sizes but whose length and complexity can cause problems. There are issues with the way auditors apply them – particularly if auditors are not familiar with them, with the way regulators approach them – which needs to be constructive, and with the quality of audit methodologies on which auditors are heavily reliant. Figure 1.1 summarises the challenges facing auditors of smaller entities.

Figure 1.1

Audit exemption in some jurisdictions has taken a very large number of entities out of the audit net, but there are still many that, for a variety of reasons, are required or chose to have an audit. In many jurisdictions, there remain well-established mandatory audit requirements for all entities, regardless of size.

1.1.1 One-size-fits-all auditing standards

ISAs are written to accommodate larger, more complex entities, as well as smaller ones. The rights and wrongs of this are a moot point but, for the foreseeable future, this is very unlikely to change. Auditors of smaller entities will continue to need to filter out the irrelevant standards and requirements. There are frequent references to internal control systems, for example. Some of these references are important – in understanding the design and implementation of the system, for example – but many are not, particularly where a substantive approach is taken. Auditors cannot, unfortunately, simply ignore all references to internal controls, even if they do take a wholly substantive approach.

1.1.2 Auditor efficiency

The issue is not exclusively one of size. Complexity is also relevant. Some smaller entity audits can be complex – entities operating in the biomedical or financial services sector, for example – and some larger entities can be relatively straightforward if they simply shift large volumes of manufactured goods, for example. Generally though, smaller entities are less complex than larger ones. A smaller entity should be easier to understand, it should be more straightforward to assess the risk of error, and audit procedures to detect those errors should be easier to design and perform. Just as importantly though, there is much less room for inefficient auditing where smaller, less complex entities are concerned, simply because of fee constraints.

This means that firms need to be clear about how they apply ISAs to smaller audits, and they need to be particularly clear about what does not need to be done and what can be done more simply on smaller audits by comparison with larger audits. It also means that some practitioners are finding it harder than ever to justify conducting just one or two audits.

1.1.3 Regulatory attitudes

Regulator behaviour drives auditor behaviour and if regulators take a compliance approach and get bogged down in the detail, auditors follow suit. The regulatory approach to audits of all sizes varies enormously. Some regulators take the view that they have been appointed to police auditor behaviour and impose sanctions where auditors fail to comply with the rules. They keep their distance from the auditors they regulate. Others take the view that they and the auditors they regulate have congruent goals in terms of improved audits, and that their job is to help auditors improve audit quality and only impose sanctions as a last resort. Both are valid approaches and most regulators fall somewhere in-between these two extremes. Auditors the world over complain that regulators are overly concerned with compliance with the detail of auditing standards, and that they pay insufficient attention to the bigger picture. Regulators point out the fact that documented evidence of compliance with ISAs is also necessary. They are both right.

1.1.4 The quality of audit methodologies

Methodologies are critical. A good auditor will perform a good audit even with a mediocre methodology, and a poor auditor a poor audit even with a good methodology, but a good quality, up-to-date methodology makes a substantial qualitative difference to most audits. The availability and quality of methodologies varies. Some methodologies are provided by professional bodies, some are provided by training consortia and some are commercially available. Many are tied into paper-based or electronic audit systems. One problem for firms that have embedded poor quality methodologies, or methodologies that have deteriorated over time, is that they cannot contemplate the logistics involved in a major overhaul, or replacing the methodology, rather than simply patching it up. Going forward though, firms may well get better at keeping systems up to date, with the increased involvement of younger people with better quality IT skills who are more accustomed and less resistant to constant change.

1.2 WHAT THE REGULATORS SAY

Regulators should recognise that smaller entity audits are different. In particular, they need to recognise that smaller entity audit documentation can be significantly simpler. Regulatory observations on specific aspects of the conduct of smaller entity audits are provided in each section of this publication, but there are a few common strands to the observations made by regulators everywhere. Auditors:

who perform high quality risk assessments sometimes need to align these better with the work they actually perform;

often perform a good audit but fail to document what they have done;

sometimes try to cut corners and avoid the requirements of ISAs by making inappropriate assumptions in areas such as materiality and related party transactions;

fail to challenge management assumptions in areas such as accounting estimates, and accept management explanations too readily without questioning them.

Many of the observations above are not exclusive to smaller entity audits, but it remains the case that all regulators are clear that all audits, large or small, complex or simple, should be performed to the same standard, using the same ISAs.

1.3 WHAT PRACTITIONERS SAY

Some practitioners have understandable concerns about ISAs. ISAs do not always seem appropriate for the audit of smaller entities. Significant effort is sometimes required to interpret and adapt ISAs to make smaller audits cost-effective and there are different views among practitioners about whether it is possible to perform smaller audits efficiently. Not very surprisingly, those who make their living out of them, and do more of them, seem to have a more positive approach.

Practitioners who do achieve a degree of efficiency in small entity audits tend to use good quality audit methodologies specifically designed for smaller entity audits, or have taken the bolder step of developing their own methodologies.

Bought-in methodologies that try to address the audit of a wide range of entities do not always scale down easily. The very best methodologies for smaller audits tend to be written in-house, by firms. This is not always possible, but firms with poor bought-in systems that derive a significant proportion of their revenue from audit clients, and who intend to stay in that market, may do well to consider developing their own methodology. At the very least they might consider commissioning one, adapted to the firm’s needs. Staff experienced in performing efficient smaller audits may not be the right staff to write the methodologies but they can certainly be used to provide input to the staff selected to perform the development work. Staff performing the development work may be a mix of junior staff who have a detailed and up-to-date knowledge of ISAs, any IT specialists, and senior staff and partners who have the experience to adapt ISAs to smaller audits.

1.4 WHAT THE STANDARDS SAY

Rightly or wrongly, there is no ‘smaller entity ISA’. Standard-setters have repeatedly made it clear that they believe that ‘an audit is an audit’, meaning that all audits, regardless of size, must be performed under the same standards.

The IAASB’s staff Q&A Applying ISAs proportionality with the size and complexity of an entity1 brings together many of the smaller entity-specific references in the application material in ISAs, under headings such as:

‘How might the work effort in an SME audit differ from that in a larger entity audit?’; and

‘Does the auditor have to comply with all ISAs when performing the audit of an SME?’

At the end of the day though, ISAs do not include much specifically directed at smaller entities, hence the need for books such as these.

Proportionality

Draft EC legislation and many other regulatory documents increasingly refer to ‘proportionality’, and the ‘proportionate application’ of ISAs to smaller entity audits. It is easier to say what this does not mean than what it does.

The proportionate application of ISAs does not mean that auditors can:

ignore relevant ISAs or ISA requirements;

make arbitrary decisions such as ‘materiality i...

Table of contents

Cover

Contents

Title

Copyright

Introduction

Chapter 1: Smaller Entity Audits

Chapter 2: Materiality

Chapter 3: Related Parties

Chapter 4: Get This Right and the Rest Falls into Place: Understanding the Entity and Assessing Risk

Chapter 5: Really Efficient Audits: What Sort of Evidence Do I Really Need?

Chapter 6: Fraud

Chapter 7: Communications with Those Charged with Governance

Chapter 8: Group Audits

Chapter 9: Other Things Good Auditors Need to Know About ISAs

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Core Auditing Standards for Practitioners by Katharine Bagshaw,John Selwood in PDF and/or ePUB format, as well as other popular books in Business & Auditing. We have over 1.5 million books available in our catalogue for you to explore.