![]()

PART I

Commonly Used Generally Accepted Accounting Principles

![]()

CHAPTER 1

Financial Statement Reporting: The Income Statement

The reporting requirements of the income statement, balance sheet, statement of changes in cash flows, and interim reporting guidelines must be carefully examined. Individuals preparing personal financial statements have to follow certain unique reporting requirements, as do those who are accounting for a partnership. Points to note are:

- Income statement preparation involves proper revenue and expense recognition. The income statement format is highlighted in this chapter along with the earnings per share computation.

- Balance sheet reporting covers accounting requirements for the various types of assets, liabilities, and stockholders’ equity.

- The statement of cash flows presents cash receipts and cash payments classified according to investing, financing, and operating activities. Disclosure is also provided for certain noncash investment and financial transactions. A reconciliation is provided between reported earnings and cash flow from operations.

- Interim financial reporting allows for some departures from annual reporting, such as the gross profit method to estimate inventory. The tax provision is based on the effective tax rate expected for the year.

- Personal financial statements show the worth of the individual. Assets and liabilities are reflected at current value in the order of maturity.

This chapter deals with the reporting requirements on the income statement. Chapter 2 deals with the balance sheet, and Chapter 3 covers the remaining statements.

IFRS Connection

The elements of financial statements are assets, liabilities, equity, income, and expenses.

Presentation of comparative financial statements is mandatory. Accordingly, the first statements must include at least one year of comparative information.

Personal financial statements are not specifically addressed by the International Financial Reporting Standards (IFRS).

Income Statement Format

With respect to the income statement, the certified public accountant (CPA)'s attention is addressed to:

- Income statement format

- Comprehensive income

- Extraordinary items

- Nonrecurring items

- Discontinued operations

- Revenue recognition methods

- Accounting for research and development costs

- Presentation of earnings per share

How are items on the income statement arranged?

In the preparation of the income statement, continuing operations are presented before discontinued operations.

Starting with income from continuing operations, the format of the income statement is:

Note

Earnings per share is shown on the income statement items as well.

Comprehensive Income

What is comprehensive income?

Comprehensive income is the change in equity occurring from transactions and other events with nonowners. It excludes investment (disinvestment) by owners.

What are the two components of comprehensive income?

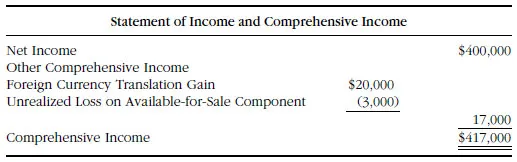

Comprehensive income consists of two components: net income and “other comprehensive income.” Net income plus “other comprehensive income” equals comprehensive income.

What does “other comprehensive income” include?

Per Accounting Standards Codification (ASC) 220-10-45-3, Comprehensive Income: Overall (Statement of Financial Accounting Standards [SFAS] FAS-130, Reporting Comprehensive Income), “other comprehensive income” includes:

- Foreign currency translation gain or loss

- Unrealized gain or loss on available-for-sale securities

- Change in market value of a futures contract that is a hedge of an asset reported at present value

How is comprehensive income reported?

ASC 220-10-45-3 has three acceptable options of reporting comprehensive income and its components. We present the best and most often used option, which is an income statement–type format:

The “other comprehensive income” items reported in the income statement are for the current-year amounts only. The total “other comprehensive income” for all the years is presented in the stockholders’ equity section of the balance sheet as “accumulated other comprehensive income.”

IFRS Connection

The statement of equity must not report the components of comprehensive income.

Extraordinary Items

What are extraordinary items?

Extraordinary items are those that are both unusual in nature and infrequent in occurrence.

- “Unusual in nature” means the event is abnormal and not related to the typical operations of the entity.

- “Infrequent in occurrence” means the transaction is not anticipated to take place in the foreseeable future, taking into account the corporate environment.

- The environment of a company includes consideration of industry characteristics, geographical location of operations, and extent of government regulation.

- Materiality is considered by judging the items individually and not in the aggregate. However, if items arise from a single specific event or plan, they should be aggregated.

Extraordinary items are shown net of tax between income from discontinued operations and net income.

What are some typical extraordinary items?

Extraordinary items include:

- Casualty losses

- Losses on expropriation of property by a foreign government

- Gain on life insurance proceeds

- Gain on troubled debt restructuring

- Loss from prohibition under a newly enacted law or regulation

Exception

Losses on receivables and inventory occur in the normal course of business and therefore are not extraordinary. Losses on receivables and inventory are extraordinary, however, if they relate to a casualty loss (e.g., earthquake) or governmental expropriation (e.g., banning of product because of a health hazard).

IFRS Connection

IFRS does not permit special reporting for extraordinary items.

Nonrecurring Items

What are nonrecurring items?

Nonrecurring items are items that are either unusual in nature or infrequent in occurrence. They are shown as a separate line item before tax in arriving at income from continuing operations. Example: The gai...