Implementing Models of Financial Derivatives is a comprehensive treatment of advanced implementation techniques in VBA for models of financial derivatives. Aimed at readers who are already familiar with the basics of VBA it emphasizes a fully object oriented approach to valuation applications, chiefly in the context of Monte Carlo simulation but also more broadly for lattice and PDE methods. Its unique approach to valuation, emphasizing effective implementation from both the numerical and the computational perspectives makes it an invaluable resource. The book comes with a library of almost a hundred Excel spreadsheets containing implementations of all the methods and models it investigates, including a large number of useful utility procedures. Exercises structured around four application streams supplement the exposition in each chapter, taking the reader from basic procedural level programming up to high level object oriented implementations. Written in eight parts, parts 1-4 emphasize application design in VBA, focused around the development of a plain Monte Carlo application. Part 5 assesses the performance of VBA for this application, and the final 3 emphasize the implementation of a fast and accurate Monte Carlo method for option valuation. Key topics include: ?Fully polymorphic factories in VBA; ?Polymorphic input and output using the TextStream and FileSystemObject objects; ?Valuing a book of options; ?Detailed assessment of the performance of VBA data structures; ?Theory, implementation, and comparison of the main Monte Carlo variance reduction methods; ?Assessment of discretization methods and their application to option valuation in models like CIR and Heston; ?Fast valuation of Bermudan options by Monte Carlo. Fundamental theory and implementations of lattice and PDE methods are presented in appendices and developed through the book in the exercise streams. Spanning the two worlds of academic theory and industrial practice, this book is not only suitable as a classroom text in VBA, in simulation methods, and as an introduction to object oriented design, it is also a reference for model implementers and quants working alongside derivatives groups. Its implementations are a valuable resource for students, teachers and developers alike. Note: CD-ROM/DVD and other supplementary materials are not included as part of eBook file.

Trusted by 375,005 students

Access to over 1 million titles for a fair monthly price.

This is an introductory part. Initial chapters introduce the Monte Carlo method in outline form, and discuss levels of program design.

Chapter 1 discusses the Monte Carlo method in abstract terms. It presents some of the mathematics lying behind the Monte Carlo methods that are later operationalized in code. It presents different evolution methods and data representation issues, but there is no actual coding.

Chapter 2 discusses issues in application design, setting the scene for the elaborations that follow. It briefly outlines the structure of an application that is developed through the first parts of the book.

In Chapter 3 we start to code up. This chapter constructs a purely procedural version of the Monte Carlo application. This has the properties of being utterly transparent but useless in practice; its faults are dissected and removed in subsequent chapters. Chapter 4 improves the application by introducing error handling. It also starts to move tentatively towards an object-oriented approach to programming by introducing a user-defined type to hold data in.

At this stage the application is still completely procedural. By the end of this part we will have gone about as far as it is sensible to go without using objects. Objects are introduced in Part II.

Chapter 1

The Monte Carlo Method

The Monte Carlo method is very widely used in the market as a valuation tool. It is used, through choice or necessity, with path-dependent options and in models with more than one or two state variables. It may be used in preference to PDE or tree methods, even in situations where these methods could work well, simply because of its generality and its robustness in contexts where a portfolio of options is being valued (rather than a single option at a time).

We start by rapidly reviewing the standard derivative valuation framework, and show how Monte Carlo works as a valuation method. Then we outline some of the factors that contribute to the design and implementation of a Monte Carlo valuation application. These are explored in greater detail as we progress through the book.

Standard references for option valuation and theory, at various levels, are Hull (2008), Joshi (2003), and Wilmott (1998). A much more advanced mathematical treatment is Musiela and Rutkowski (1997). Very good references for the Monte Carlo method are Glasserman (2004), Jäckel (2002), Dagpunar (2007) and McLeish (2005).

1.1 THE MONTE CARLO VALUATION METHOD

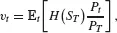

Suppose that in the market there is a European style option on an asset with value St at time t, with payoff H(ST) at its maturity time T, for some payoff function H :

→

. Write O = (T, H) for this option. Suppose that the asset value is modelled as a stochastic process S = (St)t≥0, St ε

+. For a European call option Oc we have Oc = (T,

) where

= (S − X)+ for a strike price X.

The value vt of the option at time t ≤ T is given by the fundamental pricing equation (Harrison and Kreps (1979)).

(1.1)

where P = (Pt)t≥0 is the process followed by a numeraire Pt, and

t takes expectations at time t (with respect to an underlying filtration

= (

t)t ≥ 0 of which little else will be said). Equation (1.1) assumes that processes are specified under the pricing measure with respect to Pt, so that St/Pt is a martingale.

In this book we investigate simulation methods for computing (1.1), and are not so concerned with where (1.1) comes from. For instance, unless otherwise stated, we shall assume that processes are specified under the pricing measure, and we do not general...

Table of contents

Cover

Half Title page

Title page

Copyright page

Dedication

Preface

Part I: A Procedural Monte Carlo Method in VBA

Part II: Objects and Polymorphism

Part III: Using Files with VBA

Part VI: Polymorphic Factories in VBA

Part V: Performance Issues in VBA

Part VI: Variance Reduction in the Monte Carlo Method

Part VII: The Monte Carlo Method: Convergence and Bias

Part VIII: Valuing American Options by Simulation

Afterword

Appendices

VBA, Modelling, and Computing Glossary

Abbreviations

Coding, Notational, and Typographical Conventions

Index to Code

Index to Spreadsheets

Index to Implementations

Index to Library Functions

Bibliography

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.4M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Implementing Models of Financial Derivatives by Nick Webber in PDF and/or ePUB format, as well as other popular books in Business & Finance. We have over one million books available in our catalogue for you to explore.