In this fully revised and updated Second Edition of Fixed Income Analysis, readers will be introduced to a variety of important fixed income analysis issues, including the general principles of credit analysis, term structure and volatility of interest rates, and valuing bonds with embedded options.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

• describe the basic features of a bond (e.g., maturity, par value, coupon rate, bond redeeming provisions, currency denomination, issuer or investor granted options).

• describe affirmative and negative covenants.

• identify the various coupon rate structures, such as fixed rate coupon bonds, zero-coupon bonds, step-up notes, deferred coupon bonds, floating-rate securities.

• describe the structure of floating-rate securities (i.e., the coupon formula, interest rate caps and floors).

• define accrued interest, full price, and clean price.

• describe the provisions for redeeming bonds, including the distinction between a nonamortizing bond and an amortizing bond.

• explain the provisions for the early retirement of debt, including call and refunding provisions, prepayment options, and sinking fund provisions.

• differentiate between nonrefundable and noncallable bonds.

• explain the difference between a regular redemption price and a special redemption price.

• identify embedded options (call option, prepayment option, accelerated sinking fund option, put option, and conversion option) and indicate whether each benefits the issuer or the bondholder.

• explain the importance of options embedded in a bond issue.

• identify the typical method used by institutional investors to finance the purchase of a security (i.e., margin or repurchase agreement).

SUMMARY OVERVIEW

• A fixed income security is a financial obligation of an entity (the issuer) who promises to pay a specified sum of money at specified future dates.

• Fixed income securities fall into two general categories: debt obligations and preferred stock.

• The promises of the issuer and the rights of the bondholders are set forth in the indenture.

• The par value (principal, face value, redemption value, or maturity value) of a bond is the amount that the issuer agrees to repay the bondholder at or by the maturity date.

• Bond prices are quoted as a percentage of par value, with par value equal to 100.

• The interest rate that the issuer agrees to pay each year is called the coupon rate; the coupon is the annual amount of the interest payment and is found by multiplying the par value by the coupon rate.

• Zero-coupon bonds do not make periodic coupon payments; the bondholder realizes interest at the maturity date equal to the difference between the maturity value and the price paid for the bond.

• A floating-rate security is an issue whose coupon rate resets periodically based on some formula; the typical coupon formula is some reference rate plus a quoted margin.

• A floating-rate security may have a cap, which sets the maximum coupon rate that will be paid, and/or a floor, which sets the minimum coupon rate that will be paid.

• A cap is a disadvantage to the bondholder while a floor is an advantage to the bondholder.

• A step-up note is a security whose coupon rate increases over time.

• Accrued interest is the amount of interest accrued since the last coupon payment; in the United States (as well as in many countries), the bond buyer must pay the bond seller the accrued interest.

• The full price (or dirty price) of a security is the agreed upon price plus accrued interest; the price (or clean price) is the agreed upon price without accrued interest.

• An amortizing security is a security for which there is a schedule for the repayment of principal.

• Many issues have a call provision granting the issuer an option to retire all or part of the issue prior to the stated maturity date.

• A call provision is an advantage to the issuer and a disadvantage to the bondholder.

• When a callable bond is issued, if the issuer cannot call the bond for a number of years, the bond is said to have a deferred call.

• The call or redemption price can be either fixed regardless of the call date or based on a call schedule or based on a make-whole premium provision.

• With a call schedule, the call price depends on when the issuer calls the issue.

• A make-whole premium provision sets forth a formula for determining the premium that the issuer must pay to call an issue, with the premium designed to protect the yield of those investors who purchased the issue.

• The call prices are regular or general redemption prices; there are special redemption prices for debt redeemed through the sinking fund and through other provisions.

• A currently callable bond is an issue that does not have any protection against early call.

• Most new bond issues, even if currently callable, usually have some restrictions against refunding.

• Call protection is much more absolute than refunding protection.

• For an amortizing security backed by a pool of loans, the underlying borrowers typically have the right to prepay the outstanding principal balance in whole or in part prior to the scheduled principal payment dates; this provision is called a prepayment option.

• A sinking fund provision requires that the issuer retire a specified portion of an issue each year.

• An accelerated sinking fund provision allows the issuer to retire more than the amount stipulated to satisfy the periodic sinking fund requirement.

• A putable bond is one in which the bondholder has the right to sell the issue back to the issuer at a specified price on designated dates.

• A convertible bond is an issue giving the bondholder the right to exchange the bond for a specified number of shares of common stock at a specified price.

• The presence of embedded options makes the valuation of fixed income securities complex and requires the modeling of interest rates and issuer/borrower behavior in order to project cash flows.

• An investor can borrow funds to purchase a security by using the security itself as collateral.

• There are two types of collateralized borrowing arrangements for purchasing securities: margin buying and repurchase agreements.

• Typically, institutional investors in the bond market do not finance the purchase of a security by buying on margin; rather, they use repurchase agreements.

• A repurchase agreement is the sale of a security with a commitment by the seller to repurchase the security from the buyer at the repurchase price on the repurchase date.

• The borrowing rate for a repurchase agreement is called the repo rate and while this rate is less than the cost of bank borrowing, it varies from transaction to transaction based on several factors.

PROBLEMS

1. Consider the following two bond issues.

Bond A: 5% 15-year bond

Bond B: 5% 30-year bond

Neither bond has an embedded option. Both bonds are trading in the market at the same yield.

Which bond will fluctuate more in price when interest rates change? Why?

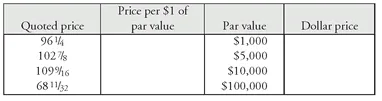

2. Given the information in the first and third columns, complete the table in the second and fourth columns:

3. A floating-rate issue has the following coupon formula:

1-year Treasury rate + 30 basis points with a cap of 7% and a floor of 4.5%

The coupon rate is reset every year. Suppose that at the reset date the 1-year Treasury rate is as shown below. Compute the coupon rate for the next year:

1-year Treasury rate

Coupon rate

First reset date

6.1%

?

Second reset date

6.5%

?

Third reset date

6.9%

?

Fourth reset date

6.8%

?

Fifth reset date

5.7%

?

Sixth reset date

5.0%

?

Seventh reset date

4.1%

?

Eighth reset date

3.9%

?

Ninth reset date

3.2%

?

Tenth reset date

4.4%

?

4. An excerpt from the prospectus of a $200 million issue by Becton, Dickinson and Company 7.15% Notes due October 1, 2009:

OPTIONAL REDEMPTION We may, at our option, redeem all or any part of the notes. If we choose to do so, we will mail a notice of redemption to you not less than 30 days and not more than 60 days before this redemption occurs. The redemption price will be equal to the greater of: (1) 100% of the principal amount of the notes to be redeemed; and (2) the sum of the present values of the Remaining Scheduled Payments on the notes, discounted to the redemption date on a semiannual basis, assuming a 360-day year consisting of twelve 30-day months, at the Treasury Rate plus 15 basis points.

a. What type of call provision is this?

b. What is the purpose of this type of call provision?

5. An excerpt from Cincinnati Gas & Electric Company’s prospectus for the 10 1/8% First Mortgage Bonds due in 2020 states,

The Offered Bonds are redeemable (though CG&E does not contemplate doing so) prior to May 1, 1995 through the use of earnings, proceeds from the sale of equity securities and cash accumulations other than those resulting from a refunding operation such as hereinafter described. The Offered Bonds are not redeemable prior to May 1, 1995 as a part of, or in anticipation of, any refunding operation involving the incurring of indebtedness by CG&E having an effective interest cost (calculated to the second decimal place in accordance with generally accepted financial practice) of less than the effective interest cost of the Offered Bonds (similarly calculated) or through the operation of the Maintenance and Replacement Fund.

What does this excerpt tell the investor about provisions of this issuer to pay off this issue prior to the stated maturity date?

6. An assistant portfolio manager reviewed the prospectus of a bond that will be issued next week on January 1 of 2000. The call schedule for this $200 million, 7.75% coupon 20-year issue specifies the following:

The Bonds will be redeemable at the option of the Company at any time in whole or in part, upon not fewer than 30 nor more than 60 days’ notice, at the following redemption prices (which are expressed in percentages of principal amount) in each case together with accrued interest to the date fixed for redemption:

If redeemed during the 12 months beginning January 1, provided, however, that prior to January 1, 2006, the Company may not redeem any of the Bonds pursuant to such option, d...

Table of contents

Title Page

Copyright Page

PART I - LEARNING OUTCOMES, SUMMARY OVERVIEW, AND PROBLEMS

PART II - SOLUTIONS

ABOUT THE CFA PROGRAM

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Fixed Income Analysis Workbook by Frank J. Fabozzi in PDF and/or ePUB format, as well as other popular books in Business & Investments & Securities. We have over 1.5 million books available in our catalogue for you to explore.