An industry leader candidly examines the role of investment leadership in portfolio management

Investment Leadership & Portfolio Management provides a top down analysis of successful strategies, structures, and actions that create an environment that leads to strong macro investment performance and rewarding investor outcomes. By examining how to manage and lead an investment firm through successful investment decision-making processes and actions, this book reveals what it will take to succeed in a radically changed investment landscape. From firm governance and firm structure-for single capability, multi-capability, and investment and product firms-to culture, strategy, vision, and execution, authors Brian Singer, Barry Mandinach, and Greg Fedorinchik touch upon key topics including the differences between leading and managing; investment philosophy, process, and portfolio construction; communication and transparency; and ethics and integrity.

Leadership issues in investment firms are a serious concern, and this book addresses those concerns

Details the strong correlation between excellence in investment leadership and excellence in portfolio management

Written by a group of experienced professionals in the field, including the Chairman of the CFA Institute Board of Governors

Understanding how to operate in today's dynamic investment environment is critical. Investment Leadership & Portfolio Management contains the insights and information needed to make significant strides in this dynamic arena.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

CHAPTER 1 Characteristics of Successful Asset Management Firms

Generally speaking, employees and clients of asset management firms are looking for rewarding, long-term relationships with superior organizations. While newspapers and other media outlets provide frequent, often daily, scorecards of asset manager investment performance, determining superiority is difficult, requiring a long period of analysis. What does it mean to be superior? Identifying, understanding and implementing the characteristics of superior investment management firms is the key objective of this book.

Throughout this book we will relate a number of observations, some general and some very specific about various investment management firms. We will point to qualities of these firms that we, or those we interviewed, identified as positive or generally negative or disadvantageous. We are not however making recommendations for or against investing with these firms. The due diligence required to make such recommendations is beyond the scope of this book. We will simply use these firms as examples to identify and discuss the qualities that our research has identified as important for success.

Every investment firm performs two basic functions: the business function (marketing and client relations) and the investment function. We refer to firms that focus most energy on the business function generally as “product-driven” and those that focus most energy on the investment function generally as “investment-driven.” These two functions often operate at cross purposes. Superior investment performance tends to attract assets from clients seeking attractive returns. This in turn may encourage product proliferation that feeds the business beast but undermines the sustainability of investment performance. A very small number of firms are built on a foundation that harmonizes the two functions. Vanguard is a product-driven firm with a low-cost business model. It delivers superior investment performance by distributing “passive” investment vehicles and avoiding the highfees of actively managed vehicles. We say “passive” in quotations, because the overwhelming majority of passive vehicles are benchmarked against active indexes. It might be more appropriate to call this activity “index fund” investing. Deciding which index fund to invest in is an active decision. However, once invested in an index fund, the fund itself employs a rule-based active strategy. The rules may include capitalization, credit rating or style tilt, among others. Unless the index comprises the entire capital market, it is active. Regardless, following market nomenclature, we use “passive” and “active” in the more pedestrian sense. Passive strategies are those with close adherence to any benchmark or index. Active strategies, by most definitions, are those that take positions different from such an index with the goal of producing an attractive risk/return profile relative to the index.

Superior investment performance through active management is, on average, not compensated. After fees, active management, in general, is negatively compensated. Further, the skill required to add value through active investing is very hard to identify. Finally, finding the skilled managers who do exist is a daunting task. Vanguard is a safer alternative for those without the knowledge, experience, or resources—the vast majority of investors—to identify investment skill. This is not to say that index funds come without risk. Understanding the basic risk characteristics of various asset classes and index funds, or relying on an experienced advisor, remains a prerequisite to investing in any investment vehicle, active or passive. Despite the fact that we characterize Vanguard as a product-driven firm, John (Jack) Bogle, Vanguard’s founder, speaks to the importance of client outcomes by admonishing the industry to prioritize stewardship over salesmanship. He deserves credit for undertaking this important endeavor and executing with excellence.

Capital Group is an active, investment-driven firm whose business model revolves around the delivery of superior long-term client outcomes. As Charles Ellis points out in Capital: The Story of Long Term Investment Excellence, “Capital Group, especially the American Funds mutual fund subsidiary, puts sound investing well ahead of sales or marketing in every business decision.”1 Charley goes so far as to say that Capital is paternalistic in its relationship with clients and potential clients. If an investment product is very salable, but not in the best interest of potential investors, then Capital will not sell the product. Capital has earned a reputation of operating in the best interest of current and prospective clients.

Why do some investment-driven and product-driven firms provide successful long-term employee and client relationships while others do not? It is impossible to provide a recipe for success, but it is possible to identify certain characteristics of successful firms. We identify five critical aspects of asset management firms that we believe significantly influence superiority and success:

Strong culture

Limited size and complexity

Clear governance of the business and investment functions

We surveyed investors, spoke with industry leaders, and drew upon our collective experiences with multiple product- and investment-driven firms to assess the importance of each characteristic in determining superiority and success. Each is covered in detail below.

This chapter, and much of the book, argues that unifying culture among a team of individuals from diverse backgrounds and educations is indispensable to the long-term, sustainable success of asset management organizations. Due to its importance, we begin with a discussion of culture and follow with a major challenge to its survivability—the allure of size—and to critical contributors to its sustenance: strong governance, capable leadership, and integrity.

YOU CAN TAKE THE BOY OUT OF THE CULTURE, BUT YOU CAN’T TAKE THE CULTURE OUT OF THE BOY

The culture of a firm is defined by the total set of shared and socially transmitted attitudes, values, aspirations, behaviors and practices of its employees. Superior asset management firms, whether product-driven or investment-driven, exude strong and positive cultures.

Consider two very different firms, both with strong and long-standing cultures. Vanguard’s culture is one that includes cost-consciousness and client outcomes. Its Internet home page states, “Investment costs count: Keep more of what you earn. The average mutual fund charges six times as much as Vanguard does.” Vanguard’s desire to deliver strong client outcomes is enshrined in its structure; mutual fund clients are owners of the firm.

Jack Bogle espouses the interests of Vanguard’s clients through the delivery of a range of low-cost investment vehicles. Jack is noted for his frugality. When an individual joins Vanguard, there is no question of the firm’s strong culture. Prospective employees know that if they are hired, they are unlikely to be jetting around the world in private jets or vacationing on yachts any time in the near future.

Some shrug off the importance of a strong and positive culture as having no place in the hardened, individualist world of investment professionals.This sentiment is unwise. While culture involves much more than just legal behavior, the U.S. legal system does not support the bravado of these investment professionals. The U.S. Department of Justice says, “A corporation is directed by its management and management is responsible for a corporate culture in which criminal conduct is either discouraged or tacitly encouraged.”2 The guidelines for determining culpability direct judges to evaluate whether the culture encourages ethical conduct. The upper echelon of asset management firms should not be cavalier about the cultures that they promote.

Cowardice asks the question - is it safe? Expediency asks thequestion - is it politic? Vanity asks the question - is it popular? And there comes a time when one must take a position that is neither, safe, or politic, nor popular; but one must take it because it is right.

—Dr. Martin Luther King, Jr.

A strong culture does not arise from just the encouragement of legal behavior; it comprises positive values, attitudes, and performance. However, the backbone of a strong culture in any organization is its values. In 1963, Thomas J. Watson Jr., the former CEO of IBM, wrote of the firm’s core values (beliefs) in the booklet A Business and Its Beliefs:

I believe the real difference between success and failure in a corporation can very often be traced to the question of how well the organization brings out the great energies and talents of its people. What does it do to help these people find common cause with each other? . . . And how can it sustain this common cause and send of direction through the many changes which take place from one generation to another? . . . [I think the answer lies] in the power of what we call beliefs and the appeal these beliefs have for its people.... I firmly believe that any organization, in order to survive and achieve success, must have a sound set of beliefs on which it premises all its policies and actions. Next, I believe that the most important single factor in corporate success is faithful adherence to those beliefs.3

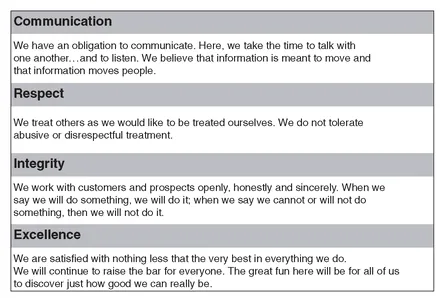

If values are so important, why do they seem to be the same, or at least very similar, for most firms? Moreover, firms of limited integrity often espouse positive values while ostensibly functioning free from their influence. This is no more clearly demonstrated than by reviewing the values of the now defunct firm, Enron Corporation. Enron collapsed after a long-term pattern of unethical and illegal behavior was uncovered. Figure 1.1 displays Enron’s values.

FIGURE 1.1 Enron Corporation’s Statement of Corporate Values

Source:www.enron.com (circa 1999)

Including the word “integrity” in Enron’s values would be comical had its behaviors not destroyed the lives of so many employees and investors. The firm ...

Table of contents

Cover

Table of Contents

Preface

CHAPTER 1: Characteristics of Successful Asset Management Firms

CHAPTER 2: Building a Cathedral

CHAPTER 3: Building a Meritocracy Understanding

CHAPTER 4: Investment Philosophy and Process

CHAPTER 5: Investment Process in an Evolving World

CHAPTER 6: Communication for Superior Client Outcomes

CHAPTER 7: Where are the Clients’ Yachts?

CHAPTER 8: Final Thoughts

Bibliography

About the Authors

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Investment Leadership and Portfolio Management by Brian D. Singer,Greg Fedorinchik in PDF and/or ePUB format, as well as other popular books in Business & Investments & Securities. We have over 1.5 million books available in our catalogue for you to explore.