Author Peter Stimes's analysis of the investment process has long been inspired by some of the best minds in the world of finance, yet some of the ways in which he approaches this discipline are truly unique. In Equity Valuation, Risk, and Investment, Stimes shares his extensive expertise with you and reveals how practitioners can integrate and apply both the theory and quantitative analysis found in finance to the day-to-day decisions they must make with regard to important investment issues.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

The past century has seen amazing strides in the area of financial economics. In this span, brief by historical standards, we have seen the development of the idea of equities being valued on the basis of discounted cash flow streams to perpetuity. In short order, there followed measures of bond duration, principles of portfolio diversification, development of risk-based asset pricing models, and theories of capital structure and dividend strategy. In more recent years, we have welcomed the rigorous theory of option and other derivatives pricing and we have, as a profession, grappled with questions of just how efficient financial markets may (or may not) be. Our collective thoughts have also turned to the theoretical questions of how price and volatility series evolve over time. To shed light on these questions, some researchers have focused on econometrics and microeconomic theory, while others have looked to the areas of psychology, behavioral studies, and experimental economics.

The focus of this book is on equity valuation, risk, and investment. The admittedly ambitious goal is to integrate and apply the insights of these theories to the day-to-day decisions that need to be made by portfolio managers, investment strategists, securities analysts, corporate managers, regulators, policy makers, and, ultimately, their investment public constituency.

Right off the bat, however, we face the problem that the body of theory in this area of study is not unified. Specifically, there are gaps and often outright contradictions between and among the various disciplines and schools of thought. To make things worse, difficulties are not always just at the periphery or the frontiers of our subject.

It is into this arena that we investment professionals and individual investors are thrown. We do not have the luxury to bemoan the absence of a unified theory, nor can we postpone our decisions as we wait and hope for theoretical and empirical clarification. We have no choice; each day we must decide what to buy, sell, and hold; how much; and at what prices. And, not to decide . . . is still to decide.

THEORETICAL PRECISION OR THEORETICAL RESILIENCE?

In essence, we have to establish an operational analytical framework—or theory—that is consistent with the basic fundamental principles of modern finance, but that can operate in a world where there are still significant unsettled questions. The modeling approach undertaken in this work is therefore necessarily epistemologically modest.

By contrast, in recent years, the development of finance and investment theory has focused heavily in those areas where computational brute force, complicated mathematics, and reams of data have been able to produce results with a high degree of precision. The greatest beneficiaries of this study have been in the areas of derivatives valuation. Consequently, if we know the prices of individual securities, short-term interest rates, and the general characteristics of their respective volatilities and correlations, we can make highly accurate valuation estimates—relative to the underlying securities prices.

What we do not know with nearly the same degree of precision is why the underlying securities prices are what they are. In essence, the valuation of equities is a discipline where computational brute force, complicated mathematics, and reams of historical data do not necessarily produce a high degree of precision.

Our dilemma is that investment researchers seem to be inherently drawn to precision. (Call it an occupational hazard.) The question of why investment researchers are drawn so strongly to, say, derivatives research is reminiscent of the story of the drunk who lost his car keys down the block but searches for them at the corner under the streetlight. When asked why, he replies, “Because the light is better over here.” While the basic questions in our field relate to the valuation of primary securities, the “light”—that is, the precision—is “better over here” in the derivatives field.

On the bright side, however, I hope to show that integrating a little bit of accepted basic theory can go a long way toward obtaining robust results in a study of equity securities where contingency and human nature feature so prominently. What is necessarily sacrificed in the way of precision and elegance is balanced by resilient ballpark results.

Said differently, we find ourselves in circumstances similar to those of the ancient Roman engineers as they designed roads, bridges, and aqueducts. Although the systematic understanding of force, energy, fluid mechanics, and system dynamics was almost two millennia in their future, they were nevertheless able to make very effective use of the basic math and empirical observations that they did have.

PRACTICAL DIFFICULTIES AS WELL

It should go without saying that theoretical concerns are naturally compounded by practical difficulties. After all, everyday observation of human nature indicates that we have pronounced and consistent cognitive difficulties in dealing with (1) nonlinear relationships, (2) the simultaneous impact of multiple variables, and (3) interactions among multiple variables. These cognitive difficulties have been systematically studied since the pathbreaking work in the 1970s by Amos Tversky and Daniel Kahneman in the application of behavioral psychology to economics. Such cognitive difficulties have also been recognized in the field of experimental economics pioneered by Vernon Smith.1

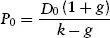

A simple example demonstrates the nature of these difficulties. We utilize the familiar Gordon constant dividend growth model. Its simple representation is

(1.1)

where

P0 = price of a common stock at initial time zero

D0 = current annualized dividend rate at initial time zero

g = constant annualized growth rate of dividends to perpetuity

k = annualized discount rate (or alternatively, internal rate of return, or annualized expected return) to perpetuity

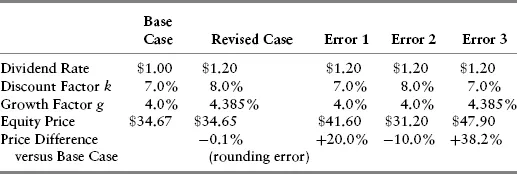

Let us hypothesize an unleveraged company with these characteristics: annualized dividend rate of $1.00 per share, a growth factor of 4% per year, and an annualized discount rate of 7.0% per year. Plugging these values into equation (1.1) produces a common equity value of $34.67.

Let us further imagine that company management decides to leverage the capital structure, forecasting that doing so will permit an increase in expected earnings and dividends per common share but also necessarily bring about an increased volatility of earnings and equity values. As a result, the discount factor must also rise.

Finally, management is assumed to increase the common dividend rate by 20%, which will detract somewhat from the long-term dividend growth factor2 but which will still permit a new growth rate of 4.385%, given the increase in debt leverage.

In a transparent, efficient capital market, the particular management recapitalization cannot, in and of itself, impact the valuation of common equity. In fact, an 8.0% annualized discount rate, together with a $1.20 revised dividend rate and a 4.385% growth factor, results in a share price of $34.65. (This is essentially an unchanged price, adjusted for rounding.)

Table 1.1 demonstrates the types of cognitive errors often made by investors that do not simultaneously reflect the impact of all the underlying valuation factors.

TABLE 1.1 Sensitivity of Valuation Estimates to Cognitive Errors

Under the heading Error 1, the investment analyst or investor has reflected the higher dividend rate but has not correctly accounted for a higher discount factor and growth rate. As a result, the estimated equity price overstates the correct price by the 20% dividend rate change. Under Error 2, the discount factor is correctly reflected, but the analyst/investor has not properly reflected that higher leverage also produces a higher expected long-term growth factor. As a result, the equity price is underestimated by 10.0%. The last column shows a case where the analyst/investor properly captures the higher growth factor due to leveraging but fails to make the proper adjustment to the discount factor to account for higher prospective earnings and price volatility. As a result, Error 3 overestimates the price by 38.2%.

Basically, even if there is an existing, accepted standard for equity valuation, cognitive mistakes by market participants can create highly different valuation assessments. As participants attempt to reconcile these differences in the capital markets through buying and selling, the results likely would be manifested as excessive volatility and/or long lag times between news events and the eventual arrival at a fully agreed-upon market consensus price that is consistent with the underlying fundamentals.

OVERVIEW OF OUR ANALYSIS

To grapple with both theoretical and practical concerns, the discussion in this book starts with the valuation of default-free debt securities, both traditional and inflation-protected bonds. This framework allows us to enhance traditional models of unleveraged equities including variations of the Franchise Value analysis introduced by Martin Leibowitz. (The key insight in this area—and simple math—depends on the concept of real or inflation-adjusted annuities.) The next step is to introduce leverage in the context of Merton Miller’s seminal 1977 article “Debt and Taxes.”

With the basic framework then in mind, we are able to calibrate the model intuitively to observable real-world results by utilizing U.S. data on aggregate corporate capital investment and profitability. We will find this to be useful in dealing with difficulties encountered in any or all of (1) valuing high-growth companies, (2) evaluating the impact of common stock buybacks and other leveraged recapitalizations, and (3) assessing mergers/acquisitions.

In addition to selected case studies, we test the model cross-sectionally at several points in time for a robust sample of common equities. Doing this will help us draw inferences about expected returns in general and draw specific inferences regarding market efficiency and portfolio management.

To complete the analysis, we extend the model in a probabilistic way to deal with questions of performance attribution and, ultimately, the degree of investment risk. This latter analysis produces interesting and useful results with regard to volatility, correlations, and portfolio allocation.

The model presented in this book has the advantage of being able, at least conceptually—and to a rough degree, practically—to evaluate each of the key valuation factors separately. In contrast, in the traditional dividend discount model, the discount rate, the growth rate, the dividend rate, and leverage are all interrelated in complex and often nonintuitive ways.

Our expositional model has been heavily shaped by the writings of Benjamin Graham, particularly the classic Security Analysis. As a result, this work is likely to be useful more to the practitioner than to the scholarly community. Where possible, I have tried throughout to present the arguments and discussion in three different forms: textual, pictorial, and mathematical. Much of the math must be included in the textual part of the exposition. However, the more formal mathematical treatment is relegated to appendices and footnotes for those who desire to pursue the topic with greater rigor.

I have benefited in my study of other fields from the historical background of how different theories have developed. This is in contrast to the formal treatment that typifies mathematics and physical sciences. For example, once I understood the historical development of set theory, the discussion of what rigorously defines a mathematical function made sense. In cont...

Table of contents

Cover

Contents

Title

Copyright

Dedication

Foreword

Preface

About the Author

Chapter 1: Introduction

Chapter 2: Inflation-Protected Bonds as a Valuation Template

Chapter 3: Valuing Uncertain, Perpetual Income Streams

Chapter 4: Valuing a Leveraged Equity Security

Chapter 5: Case Studies in Valuation During the Recent Decade

Chapter 6: Treatment of Mergers and Acquisitions

Chapter 7: A Fair Representation? Broad Sample Testing over a 10-Year Market Cycle

Chapter 8: Price Volatility and Underlying Causes

Chapter 9: Constructing Efficient Portfolios

Chapter 10: Selecting among Efficient Portfolios and Making Dynamic Rebalancing Adjustments

Chapter 11: How Did We Arrive Here Historically? Where Might We Go Prospectively?

Appendix A: Mathematical Review of Growth Rates for Earnings, Dividends, and Book Value per Share

Appendix B: Sustainable and Nonsustainable Inflation Rates

Appendix C: Deriving the “Equity Duration” Formula

Appendix D: Traditional Growth/Equity Valuation Formula

Appendix E: Adjustments Required to the Traditional Growth/Equity Valuation Formula to Preserve Inflation Neutrality

Appendix F: Brief Recapitulation of the Miller 1977 Capital Structure Irrelevance Theorem

Appendix G: Time Series Charts of Unleveraged, Inflation-Adjusted Discount Rate Estimates

Appendix H: Comparison of Volatility of Pretax and After-Tax Income

Appendix I: Relationship between Observed Price-to-Earnings (“P/E”) Ratios and Nominal Interest Rates

Appendix J: Additional Background on Mathematical Optimization Subject Constraint Conditions

Appendix K: Derivation of Asset Class Covariances

Appendix L: Expected Return and Variance/Covariance Inputs Underlying Portfolio Examples

Bibliography

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Equity Valuation, Risk, and Investment by Peter C. Stimes in PDF and/or ePUB format, as well as other popular books in Business & Valuation. We have over 1.5 million books available in our catalogue for you to explore.