Incorporate the Benefits of Activity-Based Costing into the Efficiencies of Your SAP R/3 System

Given SAP's dominance in the enterprise resource planning (ERP) market, many companies and their managers encounter SAP AG applications in some form or another. Many of these organizations have recognized the value of utilizing Activity-Based Costing/Management concepts to perform more accurate cost assignments or drive performance initiatives. Managers are then faced with trying to determine how Activity-Based Costing can be incorporated into the SAP environment. The 123s of ABC in SAP is the first book of its kind designed to help business managers understand the capabilities of the SAP R/3 business application to support Activity-Based Costing, Management, and Budgeting.

Divided into three parts-the conceptual foundation, the capabilities of SAP ABC, and integration with other tools-the book provides readers with the following:

* An explanation of how Activity-Based Costing can be used with SAP

* Helpful hints for implementing ABC into SAP

* Insights into the most common difficulties and potential solutions when implementing ABC into SAP

* Summary tables that highlight key decisions to be made, implementation hints, and organizational challenges

* Detailed descriptions of SAP software applications to support the Activity-Based Costing approach as well as the integration of SAP R/3 with Oros software

* Examples of the tandem usage of Resource Consumption Accounting with Activity-Based Costing

eBook - ePub

The 123s of ABC in SAP

Using SAP R/3 to Support Activity-Based Costing

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

The 123s of ABC in SAP

Using SAP R/3 to Support Activity-Based Costing

PART ONE

LAYING THE FOUNDATION

1

COST MANAGEMENT: A BRIEF HISTORY AND THE CONVERGENCE OF PHILOSOPHIES

Since the mid-1980s, the business community in the United States has been challenging the value of management accounting data as a support tool to business decision making. The conclusion: Management accounting as it has existed since the industrial revolution is no longer sufficient in the new more complex business world. Early management accounting served the community well for a long time. As long as the primary costs in an organization could be accurately traced to products with labor hours, or perhaps machine time, management accounting had fine tools in place. As soon as this paradigm in the cost structure changed, so did the quality of cost information. In the current marketplace, the simplistic standard cost flow has become obsolete and has been replaced with the need for more comprehensive and meaningful information.

NEED FOR CHANGE

This story has been told in countless articles and books; customers want choice, in terms of services and product permutations. These choices drive complexity and complexity drives overhead, which, in turn, negatively impacts the ability of traditional managerial accounting to satisfy managerial information needs. Combine these issues with the rise of automation and the e-marketplace, and the dilemma of the accounting world is apparent. Certainly in the future complexity will only increase. The authors of the book Blur: The Speed of Change in the Connected Economy stated, “products and services are merging, buyers sell and sellers buy. Neat value chains are messy economic webs.”1 How can the accounting profession transform itself to address this relatively new and continuously changing complexity? The quest started around the early 1950s, and the struggle to convert accounting data into strategic decision support information still continues. No longer can the business community be complacent with old cost management methodologies. New and improved philosophies have come into play, or perhaps a convergence of philosophies. Two factors surfaced in the early 1980s that had a direct impact on management accounting. The first was the emergence of the personal computer and the accompanying decentralization of computing power. The second was the emergence of Activity-Based Costing (ABC).

Technology Evolves and Facilitates Change

With the change in the business environment pushing for transformation from one direction, rapid development in technology enabled change from yet another. The growth in personal computing power suddenly enabled an accounting workforce to go beyond the focus of basic transaction reporting. With the enabling technology, the accounting community suddenly had the ability to process data in ways previously never imaginable, and management starting seeing a glimmer of light. This decentralization of computing power, for better or for worse, provided accountants with a critical enabler to convert their traditional management accounting role into a truly analytical one. Management accountants and operations management could finally put their heads together with the power of the personal computer and begin to model the organization; thus the accountant’s role shifted from being a glorified bookkeeper to a strategic decision support position.

Along with the benefits of increased computing power and decentralization came some less desirable results. First, the power to easily generate results on new dimensions often simply satisfied a whim merely to “spin” data. In order to get to the new dimensions and analytical views, tremendous effort was expended to merge financial and operational data into a usable format to work with and model these new views. This was particularly true of ABC models in the 1980s and 1990s. With information gathering and formatting taking such a significant effort, the quality and integrity of the data, let alone its timeliness, usually went unchallenged. Second, to accommodate the significant data-gathering effort, simplifications in modeling and gross organizational assumptions had to be made. These assumptions usually were frozen at a point in time, making the best analysis a stand-alone snapshot of the company at a selected point in time. Because these factors made the model almost instantly out of date, most organizations seriously doubted even the best analytical intentions.

Another effect on the technology lever of change is the impact of enterprise resource planning (ERP) software. ERP systems potentially span the entire corporate organization. An ERP vision incorporates the whole organization under one information technology roof. With ERP, the world of accounting can be integrated with operations and logistics. Full use of an ERP software eliminates most of the previous issues mentioned; simplification of the model, spinning data, merging data, and questions of quality. Rather than focusing on data collection and conversion, the data are available on a real-time basis. This one system can contain large amounts of organizational data, opening a window from accounting to other areas in the organization previously separated in silos. ERP software is utilized to integrate management statistics with financial data to finally get a fuller and timelier picture of the organization.

Even with advancements in technology in terms of raw computing power or the benefits of an integrated system solution, the underlying cost philosophy was, and still is, under attack. The following historical review provides details on the nature of the attack and the solutions proposed.

Evolution of Cost Management in the United States

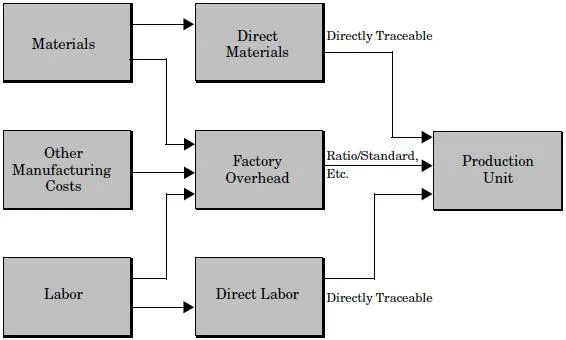

Traditional Cost Management The traditional world of management accounting was quite simple. The focus was on manufacturing as a whole and the ability to trace a cost to a finished good. Analysis of the results was clearly secondary to valuation. Cost could be analyzed and evaluated by converting the manufacturing costs of the company into three major pools:

- Direct material

- Direct labor

- Factory overhead

Since the nature of early production consisted primarily of easily traceable direct costs, the allocation of the indirect costs (i.e., indirect labor, factory overhead, indirect materials) was a simple ratio of either the direct labor or the direct materials, whichever represented the best tracing tool. (See Exhibit 1.1.)

Exhibit 1.1 Traditional Cost Allocations

In this simplistic traditional cost environment, other nonmanufacturing costs were rarely considered in the equation. Once the “direct” cost no longer represented the majority of the cost in the assignment, the traditional methodology started to show cracks in assignment logic. High-volume products began being overcosted and low-volume products were undercosted. The direct cost relationship becomes further limited as the cost focus shifts from the cost of production to the cost of services packaged with the product. These service costs most likely were not even considered in the previous costing equation. Costs such as postproduction support, sales services, and so on have quickly become a growing area in most companies. Companies that lead in today’s marketplace differentiate themselves from their competition not only in the products they produce but the customer services they provide. Therefore, the fastest-growing category of cost for many organizations has nothing to do with the direct costs of production but rather factory overhead and cost to serve the customers. The ABC philosophy was ge...

Table of contents

- Cover

- Title page

- Copyright

- Preface

- Acknowledgments

- Part One: Laying the Foundation

- Part Two: SAP R/3 Integrated Activity-Based Costing

- Part Three: Beyond SAP R/3 Integrated Activity-Based Costing

- Glossary

- Index

- EULA

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The 123s of ABC in SAP by Dawn J. Sedgley,Christopher F. Jackiw in PDF and/or ePUB format, as well as other popular books in Business & Managerial Accounting. We have over 1.5 million books available in our catalogue for you to explore.