The Five Rules for Successful Stock Investing

"By resisting both the popular tendency to use gimmicks that oversimplify securities analysis and the academic tendency to use jargon that obfuscates common sense, Pat Dorsey has written a substantial and useful book. His methodology is sound, his examples clear, and his approach timeless."

--Christopher C. Davis Portfolio Manager and Chairman, Davis Advisors

Over the years, people from around the world have turned to Morningstar for strong, independent, and reliable advice. The Five Rules for Successful Stock Investing provides the kind of savvy financial guidance only a company like Morningstar could offer. Based on the philosophy that "investing should be fun, but not a game," this comprehensive guide will put even the most cautious investors back on the right track by helping them pick the right stocks, find great companies, and understand the driving forces behind different industries--without paying too much for their investments.

Written by Morningstar's Director of Stock Analysis, Pat Dorsey, The Five Rules for Successful Stock Investing includes unparalleled stock research and investment strategies covering a wide range of stock-related topics. Investors will profit from such tips as:

* How to dig into a financial statement and find hidden gold . . . and deception

* How to find great companies that will create shareholder wealth

* How to analyze every corner of the market, from banks to health care

Informative and highly accessible, The Five Rules for Successful Stock Investing should be required reading for anyone looking for the right investment opportunities in today's ever-changing market.

eBook - ePub

The Five Rules for Successful Stock Investing

Morningstar's Guide to Building Wealth and Winning in the Market

- English

- ePUB (mobile friendly)

- Available on iOS & Android

eBook - ePub

The Five Rules for Successful Stock Investing

Morningstar's Guide to Building Wealth and Winning in the Market

About this book

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Information

1

The Five Rules for Successful Stock Investing

IT ALWAYS AMAZES me how few investors—and sometimes, fund managers—can articulate their investment philosophy. Without an investing framework, a way of thinking about the world, you’re going to have a very tough time doing well in the market.

I realized this some years ago while attending the annual meeting of Berkshire Hathaway, the firm run by billionaire superinvestor Warren Buffett. I overheard another attendee complain that he wouldn’t be attending another Berkshire meeting because “Buffett says the same thing every year.” To me, that’s the whole point of having an investment philosophy and sticking to it. If you do your homework, stay patient, and insulate yourself from popular opinion, you’re likely to do well. It’s when you get frustrated, move outside your circle of competence, and start deviating from your personal investment philosophy that you’re likely to get into trouble.

Here are the five rules that we recommend:

1. Do your homework.

2. Find economic moats.

3. Have a margin of safety.

4. Hold for the long haul.

5. Know when to sell.

Do Your Homework

This sounds obvious, but perhaps the most common mistake that investors make is failing to thoroughly investigate the stocks they purchase. Unless you know the business inside and out, you shouldn’t buy the stock.

This means that you need to develop an understanding of accounting so that you can decide for yourself what kind of financial shape a company is in. For one thing, you’re putting your own money at risk, so you should know what you’re buying. More important, investing has many gray areas, so you can’t just take someone else’s word that a company is an attractive investment. You have to be able to decide for yourself because one person’s hot growth stock is another’s disaster waiting to happen. In Chapters 4 through 7, I’ll show you what you need to know about accounting and how to boil the analysis process down to a manageable level.

Once you have the tools, you need to take time to put them to use. That means sitting down and reading the annual report cover to cover, checking out industry competitors, and going through past financial statements. This can be tough to do, especially if you’re pressed for time, but taking the time to thoroughly investigate a company will help you avoid many poor investments.

Think of the time you spend on research as a cooling-off period. It’s always tempting when you hear about a great investment idea to think you have to act now, before the stock starts moving—but discretion is almost always the better part of valor. After all, your research process might very well uncover facts that make the investment seem less attractive. But if it is a winner and if you’re truly a long-term investor, missing out on the first couple of points of upside won’t make a big difference in the overall performance of your portfolio, especially since the cooling-off period will probably lead you to avoid some investments that would have turned out poorly.

Find Economic Moats

What separates a bad company from a good one? Or a good company from a great one?

In large part, it’s the size of the economic moat a company builds around itself. The term economic moat is used to describe a firm’s competitive advantage—in the same way that a moat kept invaders of medieval castles at bay, an economic moat keeps competitors from attacking a firm’s profits.

In any competitive economy, capital invariably seeks the areas of highest expected return. As a result, the most profitable firms find themselves beset by competitors, which is why profits for most companies have a strong tendency over time to regress to the mean. This means that most highly profitable companies tend to become less profitable as other firms compete with them.

Economic moats allow a relatively small number of companies to retain above-average levels of profitability for many years, and these companies are often the most superior long-term investments. Longer periods of excess profitability lead, on average, to better long-term stock performance.

Identifying economic moats is such a critical part of the investing process that we’ll devote an entire chapter—Chapter 3—to learning how to analyze them. Here’s a quick preview. The key to identifying wide economic moats can be found in the answer to a deceptively simple question: How does a company manage to keep competitors at bay and earn consistently fat profits? If you can answer this, you’ve found the source of the firm’s economic moat.

Have a Margin of Safety

Finding great companies is only half of the investment process—the other half is assessing what the company is worth. You can’t just go out and pay whatever the market is asking for the stock because the market might be demanding too high a price. And if the price you pay is too high, your investment returns will likely be disappointing.

The goal of any investor should be to buy stocks for less than they’re really worth. Unfortunately, it’s easy for estimates of a stock’s value to be too optimistic—the future has a nasty way of turning out worse than expected. We can compensate for this all-too-human tendency by buying stocks only when they’re trading for substantially less than our estimate of what they’re worth. This difference between the market’s price and our estimate of value is the margin of safety.

Take Coke, for example. There’s no question that Coke had a solid competitive position in the late 1990s, and you can make a strong argument that it still does. But folks who paid 50 times earnings for Coke’s shares have had a tough time seeing a decent return on their investment because they ignored a critical part of the stock-picking process: having a margin of safety. Not only was Coke’s stock expensive, but even if you thought Coke was worth 50 times earnings, it didn’t make sense to pay full price—after all, the assumptions that led you to think Coke was worth such a high price might have been too optimistic. Better to have incorporated a margin of safety by paying, for example, only 40 times earnings in case things went awry.

Always include a margin of safety into the price you’re willing to pay for a stock. If you later realize you overestimated the company’s prospects, you’ll have a built-in cushion that will mitigate your investment losses. The size of your margin of safety should be larger for shakier firms with uncertain futures and smaller for solid firms with reasonably predictable earnings. For example, a 20 percent margin of safety would be appropriate for a stable firm such as Wal-Mart, but you’d want a substantially larger one for a firm such as Abercrombie & Fitch, which is driven by the whims of teen fashion.

Sticking to a valuation discipline is tough for many people because they’re worried that if they don’t buy today, they might miss the boat forever on the stock. That’s certainly a possibility—but it’s also a possibility that the company will hit a financial speed bump and send the shares tumbling. The future is an uncertain place, after all, and if you wait long enough, most stocks will sell at a decent discount to their fair value at one time or another. As for the few that just keep going straight up year after year—well, let’s just say that not making money is a lot less painful than losing money you already have. For every Wal-Mart, there’s a Woolworth’s.

One simple way to get a feel for a stock’s valuation is to look at its historical price/earnings ratio—a measure of how much you’re paying for every dollar of the firm’s earnings—over the past 10 years or more. (We have 10 years’ worth of valuation data available free on Morningstar.com, and other research services have this information as well.) If a stock is currently selling at a price/earnings ratio of 30 and its range over the past 10 years has been between 15 and 33, you’re obviously buying in at the high end of historical norms.

To justify paying today’s price, you have to be plenty confident that the company’s outlook is better today than it was over the past 10 years. Occasionally, this is the case, but most of the time when a company’s valuation is significantly higher now than in the past, watch out. The market is probably overestimating growth prospects, and you’ll likely be left with a stock that underperforms the market over the coming years.

We’ll talk more about valuation in Chapters 9 and 10, so don’t worry if you’re still wondering how to value a stock. The key thing to remember for now is simply that if you don’t use discipline and conservatism in figuring out the prices you’re willing to pay for stocks, you’ll regret it eventually. Valuation is a crucial part of the investment process.

Hold for the Long Haul

Never forget that buying a stock is a major purchase and should be treated like one. You wouldn’t buy and sell your car, your refrigerator, or your DVD player 50 times a year. Investing should be a long-term commitment because short-term trading means that you’re playing a loser’s game. The costs really begin to add up—both the taxes and the brokerage costs—and create an almost insurmountable hurdle to good performance.

If you trade frequently, you’ll rack up commissions and other expenses that, over time, could have compounded. Every $1 you spend on commissions today could have been turned into $5.60 if you had invested that dollar at 9 percent for 20 years. Spend $500 today and you could be giving up more than $2,800 20 years hence.

But that’s just the beginning of the story because frequent trading also dramatically increases the taxes you pay. And whatever amount you pay in taxes each year is money that can’t compound for you next year.

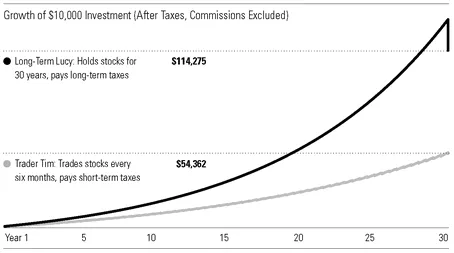

Let’s look at two hypothetical investors to see what commissions, trading, and taxes can do to a portfolio. Long-Term Lucy is one of those old-fashioned fuddy-duddies who like to buy just a few stocks and hang on to them for a long time, and Trader Tim is a gunslinger who likes to get out of stocks as soon as he’s made a few bucks (see Figure 1.1).

Figure 1.1 Tim turns over his portfolio every six months, incurring a 35% short-term capital gains tax. Lucy’s gains are taxed at only 15% thanks to her buy-and-hold strategy, and more of her money compounds over a longer time. Source: Morningstar, Inc.

Lucy invests $10,000 in five stocks for 30 years at a 9 percent rate of return and then sells the investment and pays long-term capital gains of 15 percent. Tim, meanwhile, invests the same amount of money at the same rate of return but trades the entire portfolio twice per year, paying 35 percent short-term capital gains taxes on his profits and reinvesting what’s left. We’ll give them both a break and not charge them any commissions for now.

After 30 years, Lucy has about $114,000, while Tim has less than half that amount—only about $54,000. As you can see, letting your money compound without paying Uncle Sam every year makes a huge difference, even ignoring brokerage fees.

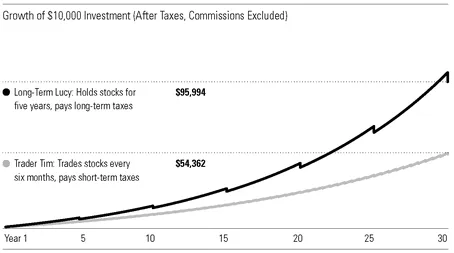

And since holding a single stock for 30 years may not be realistic, let’s consider what happens if Lucy sells her entire portfolio every five years, reinvesting the proceeds each time. In this case, she winds up with about $96,000—which is not much less than $114,000 and is still much more than Tim’s $54,000 (see Figure 1.2).

These examples look at just the tax impact of frequent trading—things look even worse for the traders once we factor in commissions. If we assume that Tim and Lucy pay $15 per trade, Tim nets only about $31,000 after 30 years and Lucy nets $93,000, again assuming she holds her stocks for five years (see Figure 1.3).

Figure 1.2 Lucy decreases her holding period to 5 years from 30 years, but the benefit of lower taxes and a longer compounding period still nets her significantly more than Tim. Source: Morningstar, Inc.

The real-world costs of taxes and commissions can take a big bite out of your portfolio. Extending your average holding period from six months to five years yields about $62,000 in extra investment returns. Lucy gets a lavish reward for her patience, don’t you think?

One final thought: To match Lucy’s $93,000 portfolio value, Tim would need to generate returns of around 14 percent each year instead of 9 percent. That’s the true cost of frequent trading in this example—about five percentage points per year. So, if you really think that churning your portfolio will get you five extra percentage points of performance each year, then trade away. If, like the rest of us, you were taught some humility by the bear market, be patient—it’ll pay off.

Know When to Sell

Ideally, we’d all hold our investments forever, but the reality is that few companies are worth holding for decades at a stretch—and few investors are savvy enough to buy only those companies. Knowing when it’s appropriate to bail out of a s...

Table of contents

- Title Page

- Copyright Page

- Foreword

- Acknowledgments

- Introduction

- Chapter 1 - The Five Rules for Successful Stock Investing

- Chapter 2 - Seven Mistakes to Avoid

- Chapter 3 - Economic Moats

- Chapter 4 - The Language of Investing

- Chapter 5 - Financial Statements Explained

- Chapter 6 - Analyzing a Company—The Basics

- Chapter 7 - Analyzing a Company—Management

- Chapter 8 - Avoiding Financial Fakery

- Chapter 9 - Valuation—The Basics

- Chapter 10 - Valuation:—Intrinsic Value

- Chapter 11 - Putting It All Together

- Chapter 12 - The 10-Minute Test

- Chapter 13 - A Guided Tour of the Market

- Chapter 14 - Health Care

- Chapter 15 - Consumer Services

- Chapter 16 - Business Services

- Chapter 17 - Banks

- Chapter 18 - Asset Management and Insurance

- Chapter 19 - Software

- Chapter 20 - Hardware

- Chapter 21 - Media

- Chapter 22 - Telecom

- Chapter 23 - Consumer Goods

- Chapter 24 - Industrial Materials

- Chapter 25 - Energy

- Chapter 26 - Utilities

- Appendix

- Recommended Readings

- Morningstar Resources

- Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

- Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

- Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go.

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Five Rules for Successful Stock Investing by Pat Dorsey in PDF and/or ePUB format, as well as other popular books in Personal Development & Personal Finance. We have over 1.5 million books available in our catalogue for you to explore.