The most comprehensive and authoritative review of B-School fundamentals—from top accounting and finance professors

For years, the Portable MBA series has tracked the core curricula of leading business schools to teach you the fundamentals you need to know about business-without the extreme costs of earning an MBA degree. The Portable MBA in Finance and Accounting covers all the core methods and techniques you would learn in business school, using real-life examples to deliver clear, practical guidance on finance and accounting. The new edition also includes free downloadable spreadsheets and web resources.

If you're in charge of making decisions at your own or someone else's business, you need the best information and insight on modern finance and accounting practice. This reliable, information-packed resource shows you how to understand the numbers, plan and forecast for the future, and make key strategic decisions. Plus, this new edition covers the effects of Sarbanes-Oxley, applying ethical accounting standards, and offers career advice.

• Completely updated with new examples, new topics, and full coverage of topical issues in finance and accounting—fifty percent new material • The most comprehensive and authoritative book in its category • Teaches you virtually everything you'd learn about finance and accounting in today's best business schools

Whether you're thinking of starting your own business or you already have and just need to brush up on finance and accounting basics, this is the only guide you need.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Gail was applying for a bank loan to start her new business: Nutrimin, a retail store selling nutritional supplements, vitamins, and herbal remedies. She described her concept to Hal, a loan officer at the bank.

Hal: How much money will you need to get started?

Gail: I estimate $80,000 for the beginning inventory, plus $36,000 for store signs, shelves, fixtures, counters, and cash registers, plus $24,000 working capital to cover operating expenses for about two months. That’s a total of $140,000 for the start-up.

Hal: How are you planning to finance the investment of $140,000 for the start-up?

Gail: I can put in $100,000 from my savings, and I’d like to borrow the remaining $40,000 from the bank.

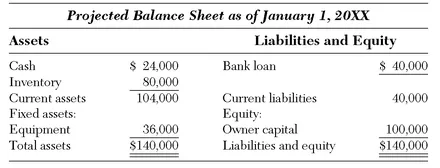

Hal: Suppose the bank lends you $40,000 on a one-year note, at 15% interest, secured by a lien on the inventory. Let’s put together projected financial statements from the figures you gave me. Your beginning balance sheet would look like what you see on the computer screen:

Nutrimin

The left side shows Nutrimin’s investment in assets. It classifies the assets into “current” (which means turning into cash in a year or less) and “noncurrent” (not turning into cash within a year). The right side shows how the assets are to be financed: partly by the bank loan and partly by your equity as the owner.

Gail: Now I see why it’s called a “balance sheet.” The money invested in assets must equal the financing available—it’s like two sides of the same coin. Also, I see why the assets and liabilities are classified as “current” and “noncurrent”—the bank wants to see if the assets turning into cash in a year or less will provide enough cash to repay the one-year bank loan. Well, in a year there should be cash of $104,000. That’s enough cash to pay off more than twice the $40,000 amount of the loan. I guess that guarantees approval of my loan!

Hal: We’re not quite there yet. We need some more information. First, tell me: How much do you expect your operating expenses will be?

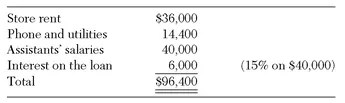

Gail: For year 1, I estimate as follows:

Hal: We also have to consider depreciation on the store equipment. It probably has a useful life of 10 years. So each year it depreciates 10% of its cost of $36,000. That is $3,600 a year for depreciation. So operating expenses must be increased by $3,600 a year from $96,400 to $100,000. Now, moving on, how much do you think your sales will be this year?

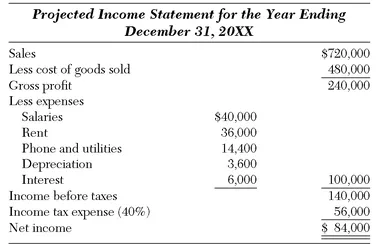

Gail: I’m confident that sales will be $720,000 or even a little better. The wholesale cost of the items sold will be $480,000, giving a markup of $240,000—which is 33

% on the projected sales of $720,000.

Hal: Excellent! Let’s organize this information into a projected income statement. We start with the sales, and then deduct the cost of the items sold to arrive at the gross profit. From the gross profit we deduct your operating expenses, giving us the income before taxes. Finally we deduct the income tax expense in order to get the famous “bottom line,” which is the net income. Here is the projected income statement shown on my computer screen:

Nutrimin

Gail, this looks very good for your first year in a new business. Many business start-ups find it difficult to earn income in their first year. They do well just to limit their losses and stay in business. Of course, I’ll need to carefully review all your sales and expense projections with you, in order to make sure that they are realistic. But first, do you have any questions about the projected income statement?

Gail: I understand the general idea. But what does “gross profit” mean?

Hal: It’s the usual accounting term for sales less the amount that your suppliers charged you for the goods that you sold to your customers. In other words, it represents your markup from the wholesale cost you paid for goods to the price for which you sold those goods to your customers. It is called “gross profit” because your operating expenses have to be deducted from it. In accounting, the word gross means “before deductions.” For example, “gross sales” means sales before deducting goods returned by customers. Sales after deducting goods returned by customers are referred to as “net sales.” In accounting, the word net means “after deductions.” So, “gross profit” means income before deducting operating expenses. By the same token, “net income” means income after deducting operating expenses and income taxes. Now, moving along, we are ready to figure out your projected balance sheet at the end of your first year in business. But first, I need to ask you: How much cash do you plan to draw out of the business as your compensation?

Gail: My present job pays $76,000 a year. I’d like to keep the same standard of compensation in my new business this coming year.

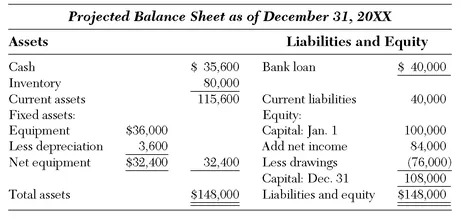

Hal: Let’s see how that works out after we’ve completed the projected balance sheet at the end of year 1. Here it is on my computer screen:

Nutrimin

Gail, let’s go over this balance sheet together. It has changed, compared to the balance sheet as of January 1. On the “Liabilities and Equity” side of the balance sheet, the net income of $84,000 has increased capital to $184,000 (because earning income adds to the owner’s capital), and deducting drawings of $76,000 has reduced capital to $108,000 (because drawings take capital out of the business). On the “Assets” side, notice that the equipment now has a year of depreciation deducted, which writes it down from the original $36,000 to a net (there’s that word “net” again) $32,400 after depreciation. The equipment had an expected useful life of 10 years, now reduced to a remaining life of nine years. Last, but not least, notice that the cash has increased by only $11,600 from $24,000 at the beginning of the year to $35,600 at year-end. This leads to a problem: The bank loan of $40,000 is due for repayment on December 31. But there is only $35,600 of cash available on December 31. How can the loan be paid off when there is not enough cash to do so?

Gail: I see the problem. But I think it’s bigger than just paying off the loan. The business will also need to keep about $25,000 cash on hand to cover two months’ operating expenses and income taxes. So, with $40,000 to repay the loan, plus $25,000 for operating expenses, the cash requirements add up to $65,000. But there is only $35,600 cash on hand. This leaves a cash shortage of almost $30,000 ($65,000 less $35,600). Do you think that will force me to cut down my drawings by $30,000, from $76,000 to $46,000? Here I am, opening my own business, and it looks as if I have to go back to what I was earning five years ago!

Hal: That’s one way to do it. But here’s another way that you might like better. After your suppliers get to know you, and do business with you for a few months, you can ask them to open credit accounts for Nutrimin. If you get the customary 30-day credit terms, then your suppliers will be financing one month’s inventory. That amounts to one-twelfth of your $480,000 annual cost of goods sold, or $40,000. This $40,000 will more than cover the cash shortage of $30,000.

Gail: That’s a perfect solution! Now, can we see how the balance sheet would look in this case?

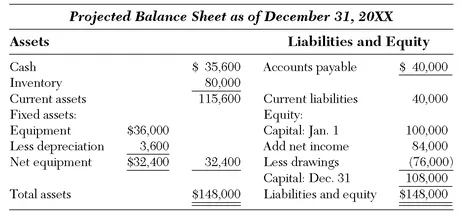

Hal: Sure. When you pay off the bank loan, it vanishes from the balance sheet. It is replaced by accounts payable of $40,000. Then the balance sheet looks like this:

Nutrimin

Now the cash position looks a lot better. But it hasn’t been entirely solved: there is still a gap between the accounts payable of $40,000 and the cash of $35,600. So, you will need to cut your drawings by about $5,000 in year 1. But that’s still much better than the cut of $30,000 that had seemed necessary before. In year 2, the bank loan will be gone, so the interest expense of $6,000 will be saved. Then you can use $5,000 of this savings to restore your drawings back up to $76,000 again.

Gail: That’s good news. I’m beginning to see how useful projected financial statements are for business planning. Can we look at the revised projected balance sheet now?

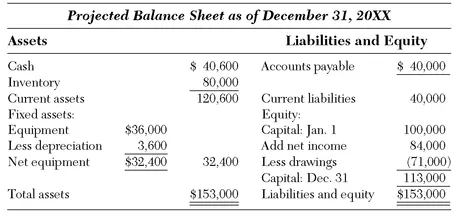

Hal: Of course. Here it is:

Nutrimin

As we see, cash is increased by $5,000 to $40,600—which is sufficient to pay the accounts payable of $40,000. Drawings are decreased by $5,000 to $71,000, which provided the $5,000 increase in cash.

Gail: Thanks. That makes sense. I really appreciate everything you’ve taught me about financial statements.

Hal: I’m happy to help. But there is one more financial statement to discuss. A full set of financial statements consists of more than the balance sheet and the income statem...

Table of contents

Title Page

Copyright Page

List of Downloadable Materials

Syllabus

Preface

Acknowledgements

About the Contributors

Part I - Financial Accounting

Part II - Financial Management

Part III - Business Entities

Part IV - Management Accounting

Part V - Planning and Strategy

Part VI - Advanced Topics

Glossary

Index

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Portable MBA in Finance and Accounting by Theodore Grossman,John Leslie Livingstone in PDF and/or ePUB format, as well as other popular books in Business & Management. We have over 1.5 million books available in our catalogue for you to explore.