![]()

PART I

THE ART OF DIVIDEND INVESTING

![]()

CHAPTER 1

First Things First

We don’t receive wisdom; we must discover it for ourselves after a journey that no one can take for us or spare us.

—Marcel Proust

I am not a therapist, and this book is not a journey into navel gazing and self-discovery. That being said, you have to get this part right.

Investor psychology and sentiment play a significant role in how you approach investments and the investing process. In my experience the most successful investors have had an end goal in mind that they wanted to achieve, which necessarily dictated the majority of their investment decisions. This is not to say that you can’t be a successful investor without having a game plan mapped out, but understanding your motivation for putting your hard-earned money at risk in the markets can help you avoid taking unnecessary risks.

With that in mind, forgive my waxing philosophical for a moment. If September 11, 2001 has taught us anything, let’s hope it’s that life is precious and time is valuable. If you accept this premise as true, you would agree with me, then, that ideally, we should spend as much time as possible in this life to find and embrace our passions; those activities that make our hearts swell and our souls soar.

The reality though is that we don’t live in an ideal world. As human beings we have to spend a significant portion of our time providing for the practical necessities: food, clothing, housing, transportation, education, recreation, and medication. The means by which we acquire these necessities is called cash.

It’s All About the Cash

Generating sufficient cash to meet your needs will be a primary objective until you die. If you have loved ones you are responsible for, they will continue to need cash after you die.

During the employment years, you must make wages, salaries, and bonuses do double duty, providing for current needs while investing for the future. Optimally, the invested cash will generate sufficient interest, dividends, and capital appreciation to meet your future needs when your wages, salaries, and bonuses are no longer your primary sources of income. Your long-term challenge then will be to balance your cash flow between your current cash needs and your need to accumulate cash for the future. Your level of success in this endeavor can be positively impacted by a modicum of financial planning.

Financial planning is an excellent exercise and a useful tool to organize your financial activities and to create a disciplined structure. Although some practitioners can overwhelm you with the minutia, an understanding of your current cash flow and budget is sufficient to make some reasonable assumptions for a retirement budget. This information will provide a working framework for how much you need to save, the required rate of return on those savings to meet your goals, and how much insurance you need to protect yourself and your loved ones should you become disabled or die prematurely. Armed with that information and this book, you can accomplish the rest.

Technology has changed the world, our culture, and social mores. This new era of interconnectivity has accelerated the pace at which we receive information and process its applicability to our lives. By extension, the workplace and the work ethic have evolved as well. The time when one would choose a career track with one employer or within one industry from beginning to end has vanished. Second, third, and even fourth careers are now commonplace. Again, by extension, retirement or at least the concept of retirement has also evolved. The twentieth-century model of moving from employment to the golden years in pursuit of leisure has morphed into the reality that for many, whether by choice or necessity, a portion of the golden years now includes some form of continuing employment.

The recession and cyclical downturn in housing beginning in 2008 notwithstanding, the long-term economic reality is that historically the cost of living increases year after year. Unless your cash flow increases at the same rate as the cost of your expenditures, you will have to decide between spending on current needs and investing for future needs.

Barring a major depression or the end of the world, the cost of living and the average life span will most likely continue to increase. Assuming I am correct, you need to be prepared for the rising cost of the practical necessities for a greater amount of time. This is to say you are going to need a lot of cash. Granted, we all have unique circumstances and situations, so how we approach spending and investing will vary by the individual. Regardless of the myriad factors to consider, don’t just stick your head in the sand and hope for the best; hope is not a strategy for success.

The Importance of Planning

As an investment advisor, I have witnessed too frequently the stress and anxiety of investors who have underestimated their cash needs for retirement. Because retirement planning didn’t gain wide acceptance until the early nineties, too many waited to properly fund their 401(k) plans, IRAs, and after-tax investments and savings, and/ or they weren’t properly invested. I can’t tell you how many people have told me that they thought that Social Security would make up the difference. Although Social Security worked well when the demographics were more favorable, ensuring benefits for future recipients required changes in the system that were never instituted. Today we are faced with the prospect of a bankrupt program. Although there are voices that advocate long-needed reforms, I would suggest that there will not be any significant changes made to Social Security because it is politically too hot to handle. For the reader below 40 years of age this is unfortunate; I wouldn’t count on Social Security being available to supplement your retirement. Let’s all hope that I am very, very wrong.

Undoubtedly there are some readers who are proactive and better prepared, who embraced retirement planning early on by funding a 401(k), an IRA, and after-tax investments. By design or by luck, some will have invested well and will be on track; others won’t be so lucky. If you are unsure about where you stand, don’t guess. If you need help, engage a fee-based financial planner. Your tax preparer or attorney should have some ready references. Whether you go it alone or require some assistance, however, just make sure you get it done. Knowing what you need and when you will need it is critical to the investment process. When it comes to your future, don’t be afraid to ask questions.

In my experience, few people have the answers to these questions off the top of their heads. It isn’t that they aren’t capable, but most people prefer to concentrate on activities they find more attractive. I understand that perspective because most people naturally gravitate to what most interests them. Some of us are butchers, others are bakers, and many are candlestick makers. So I say again, don’t guess; find out what you’ll need so you get your goals and objectives in focus, and then we can help you with the rest.

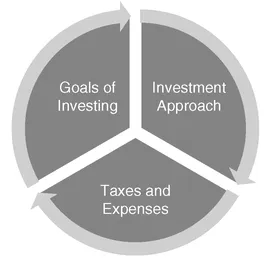

If you know what your goals and objectives are, you are well on your way to achieving investment success. At the end of the day, successful investing is realized by three activities: know the end goal(s) of why you are investing; use an investment approach that makes sense to you and can generate returns sufficient to meet your goals; and, keep an eye on taxes and expenses.

The three activities, shown in Figure 1.1, are nothing more than being mindful about your investments and investment decisions. You put thought and consideration into other critical areas of your life, why shouldn’t you do the same about your investments? Think of it this way: By entertaining some mindful decision-making about your investments, you just might eliminate any fears and anxiety you may have about your financial future. How’s that for a payoff?

As stated previously, little has changed in human nature. The two base emotions of fear and greed are still the most difficult challenges most investors face. The fear of losing money on a poor investment is equaled only by the fear of losing money on a lost opportunity; both are directly attributable to a lack of good information. Making mindful, long-term investment decisions is almost impossible without good information.

It is ironic that, in the Information Age, the average investor suffers from information deprivation. On a certain level this seems absurd, considering the number of investment newsletters, magazines, and periodicals in publication; the financial shows with which the radio waves are congested;, and the content of cable television, offering more content around the clock than anyone can possibly assimilate. Well, yes, all of these sources are readily available. But so what? The answer lies not in how much information is available but in how much is important. The investing public doesn’t suffer from a lack of information; they suffer from a lack of relevant information.

Figure 1.1 Mindful Investment Decisions

Our Purpose

As the editor of an investment newsletter I don’t wish to come off as self-serving or hypocritical, but there are two critical elements to understand about this point: content and purpose. At Investment Quality Trends we produce all of our content internally for the purpose of helping the subscriber to make well-informed investment decisions. At inception we decided that to remain independent and completely objective we would accept no outside advertising. Therefore, our revenues are based solely on subscriptions. That fact necessitates that our content must fulfill subscribers’ needs for information that results in good investment decisions and profits, which results in continued subscriptions.

By comparison, much of the mainstream financial media is big business beholden to shareholders who expect its company to generate big revenues. Like all publicly traded companies, the sole function is to generate a profit, just like any other business in America. The means by which big media produces its profits is by advertising revenues. Advertising revenues are based on the number of people—the audience—that medium reaches. To encourage people to read, listen to, or view their medium, they have to create interest and grab the audience’s attention.

Unfortunately, the means by which the audience’s interest is grabbed isn’t necessarily useful information. And, when questionable information is distributed by sources that are thought to be highly knowledgeable and dependable, it only compounds the problem.

On the other hand the information that will work for the audience isn’t always commercially attractive or appealing. So, in wanting to be entertained, much of the investing public gravitates toward information that is the equivalent of nutritionally empty fast food, and then they wonder why they are suffering from malnutrition. The tragedy i...