![]()

Chapter 1

Introduction: Pensions in Perspective

1.1. Pension issues

1.1.1. The challenge

The future of our pension systems is clearly one of the main economic challenges for the world in the coming decades. In the vast majority of countries, collective pension schemes have been created by states as well as by private companies or professional organizations. These systems can use very different tools, techniques, funding approaches or legal forms.

From a historical point of view, the concept of an organized pension institution is relatively new in human evolution and can be seen essentially as a creation of the 20th Century. Of course for centuries, societies have accepted the idea of solidarity between generations and the fact that at a given age people must stop working and then receive other forms of income to survive. But in the traditional way of life, this solidarity was guaranteed by familial or tribal assistance without need of complicated collective systems. For instance, it was common, in this context, to have families with 3 (or even 4) different generations living together in the same house and sharing a global income. At the same time, the mean longevity was not as important and the number of retirement years was limited in general.

The emergence and development of pension schemes in our modern societies can essentially be explained by two factors:

– the “individual approach” of life: our modern world tends to replace large “multi–generational” families by an individual model where each person is assumed to be self–supporting, before and after retirement age. As a consequence, personal pension planning, including social security pensions and other incomes, becomes a necessity for everyone;

– the “longevity syndrome”: longevity has increased extraordinarily in recent decades and nothing indicates that a stopping or reversing of this phenomenon could occur in the next few years. In the past it was usual to retire at 65 and then have a life expectancy of only a few years. Nowadays, and in the near future, in a lot of countries, it will be quite common for all of us to hope to survive until after 85!

This longevity evolution is a major driving force in motivating the development of various pension schemes under different forms. But at the same time it induces a huge challenge in terms of financial sustainability. Indeed, for the first time in history, we can simultaneously observe two major demographic evolutions: a continuous increase in longevity leading to an expected increase in the proportion of retirees and a decrease of fertility rates leading to a decrease of active workers.

As a consequence, we will live in increasingly ageing societies, with fewer contributors and more beneficiaries.

1.1.2. Some figures

In order to give a global view of the importance of the pension challenge and its worldwide coverage, we present some international demographical and financial figures [OEC 11].

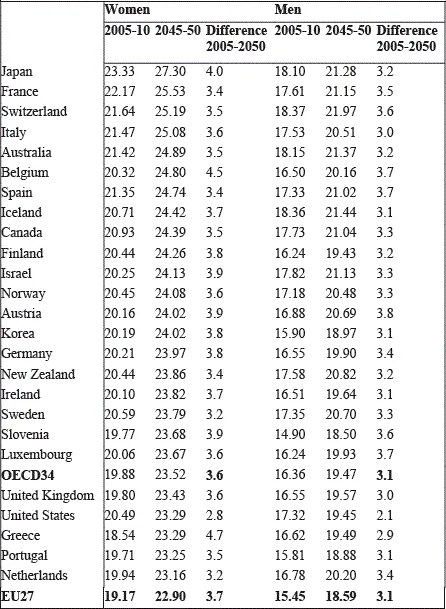

1.1.2.1. Longevity at 65

The following table compares in various countries, for men and women, the life expectancy at 65 in 2005 and that projected for 2050. It shows that everywhere our longevity is expected to continue increasing in the coming years by more than 3 years. For the OECD34, a man aged 65 in 2045 is expected to survive until 84 (88 for a woman).

1.1.2.2. Fertility rates

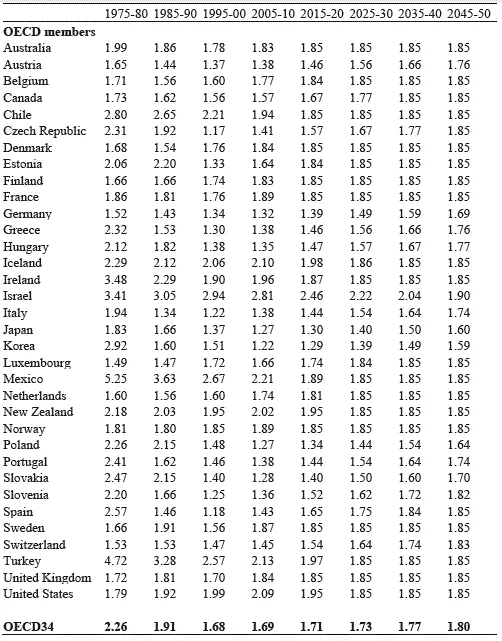

The following table compares, in various countries, the evolution of the fertility rate between 1975 and 2050. It illustrates the persistent low level of this rate (less than 2.1, which is often seen as the necessary rate in order to guarantee the strict renewal of the population). For OECD34, this rate is expected to stay around 1.7.

Total fertility rates. 1975–2050

1.1.2.3. Public pension expenditure

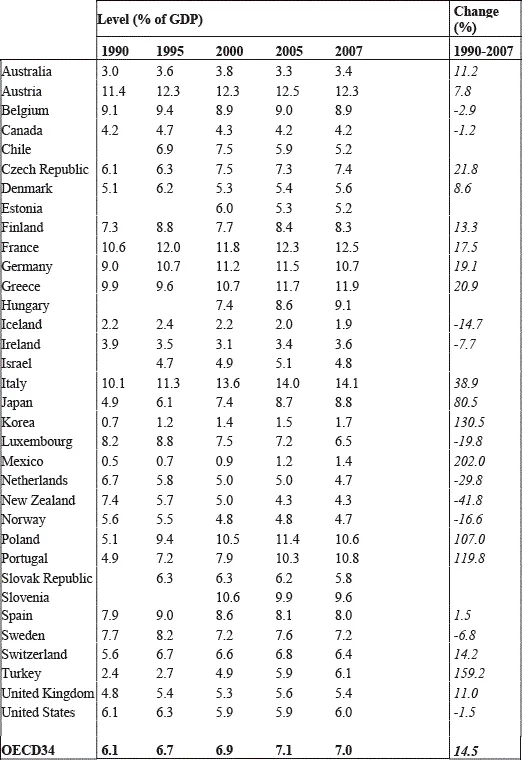

The following table compares, in various countries, the evolution of the public pension expenditure between 1990 and 2007 (in % of the GDP). Absolute levels and evolutions can be quite different from one country to another, depending on the importance of social security and the eventual financial measures already taken by some states (for instance Sweden or Luxemburg). But from a global point of view, the increasing trend seems to be clear. For OECD34, nowadays public pension expenditures represent 7% of the GDP.

1.1.2.4. Assets of pension funds

The following table gives the pension assets (in % of the GDP and in USD) for 2009, in various countries. These figures illustrate the importance of the pension fund assets invested in the financial markets. For OECD34, these assets represent two–thirds of the GDP.

...