![]()

PART I

Credit Risk and Credit Derivative Instruments

Credit risk is the risk of loss arising from the inability of a borrower to make interest and/or principal repayments on a loan. Anyone who has lent funds to a borrower that is not considered as default risk-free is exposed to a certain level of credit risk. While credit risk has been a factor for investor concern ever since the development of capital markets, it has received considerable attention among market participants since the 1990s. This attention has taken the form of ever more sophisticated methods of measuring credit risk and managing credit risk. It is the latter that is the backdrop to the instruments discussed in this book. An understanding of the former is necessary, therefore we will begin with a look at credit risk and credit risk measurement.

Credit derivatives are important tools that are used in the managing and hedging of credit risk, and also for trading and investing in credit, as we shall see. All credit derivatives are instruments, financial contracts in fact, that enable credit risk on a particular named asset or borrowing entity, the reference entity, to be transferred from one party to another. In essence, one party is buying protection on the reference entity from the counterparty, who is selling credit protection. The buyer pays a premium to the seller during the life of the credit derivative contract in return for receiving credit protection. The seller agrees to pay the buyer a pre-specified amount under certain conditions of default, or upon a restructuring event.

We begin with a look at credit risk and risk measurement. After our introduction to the concept of credit risk, we look in detail at all the important credit derivative instruments, their description, application and pricing. The main instruments are credit default swaps, total return swaps and credit-linked notes. Although all these instruments achieve the same end-goal of transferring credit risk exposure from a protection buyer to a protection seller, there are subtle differences between them. Credit-linked notes are fundamentally different to the other two types, as they are funded credit derivatives as opposed to unfunded ones. We explain this shortly. An instrument developed much earlier, the asset swap, is nowadays considered to be a credit derivative as well, so we also look at this product.

THE CONCEPT OF SYNTHETIC INVESTMENT

If one stops to consider it, banks have been ‘selling protection’ on their customers ever since they began formally borrowing and lending in the Italian city-states during the Middle Ages. Let’s think about it.

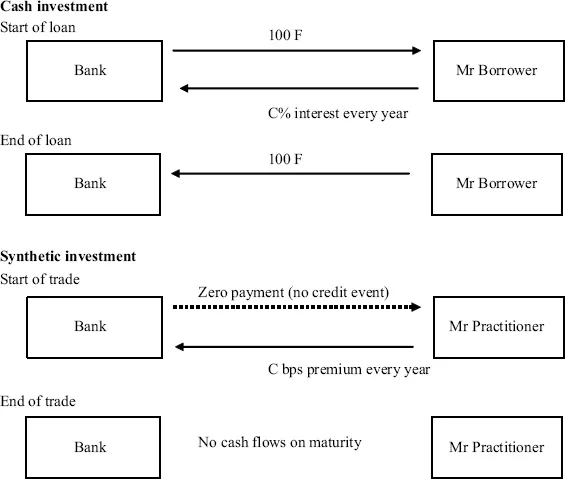

Cash Investment

A Bank lends 100 florins to Mr Borrower for a period of five years, who agrees to pay interest of C% per year each year until loan expiry, at which point he will return the original 100 florins. This is shown at Figure 1. We assume that Mr Borrower does not default on payment of both interest and principal. The net gain to Bank after the five years is the interest of C each year, which after five years will be 5C. (We have ignored funding costs here.)

Synthetic Investment

A Bank sells protection on Mr Borrower to Mr Practitioner for a period of five years, who agrees to pay C basis points premium per year each year until trade expiry. This is also shown at Figure 1. We assume that Mr Borrower does not go into bankruptcy, liquidation or administration during the five years, and that Mr Practitioner keeps up the premium payments until expiry.

The net gain to Bank after the five years is the CDS premium of C each year, which after five years will be 5C. Note that Mr Borrower is not involved in this transaction at all, as we see in Figure 1. It is between Bank and Mr Practitioner.

This illustration is a bit cheeky but it makes the point. The return for Bank of 5C is identical in each case. So Bank can decide between cash and synthetic investment; in theory the return will be identical. In terms of net cash flow, the end-result actually is identical if the price associated with Mr Borrower’s credit risk is C. The only difference is that the cash trade is funded while the CDS trade is unfunded. Bank has to find 100 florins to lend to Mr Borrower, but doesn’t need to find any cash to invest in Mr Borrower via Mr Practitioner.

Of course, if there is a credit event, then Bank will have to find 100 florins. So we need to consider the event of default. Before we do, let’s make it a bit more real . . .

Real-world Application

If we convert the bond investment to an asset swap that pays LIBOR + X basis points (bps), the interest basis of the bond has changed from fixed coupon to floating coupon. It is now conceptually identical to the synthetic (credit default swap) premium of X bps.

In the cash market, we assume that the investor has funding cost of LIBOR-flat, so that the 100 it borrows to buy the bond with costs it LIBOR-flat in funding. The net return to the investor is X. For the synthetic investor, who has no funding cost (it does not borrow any cash as it is not buying a bond), the net return is X bps.

Let us now allow for a default or ‘credit event’.

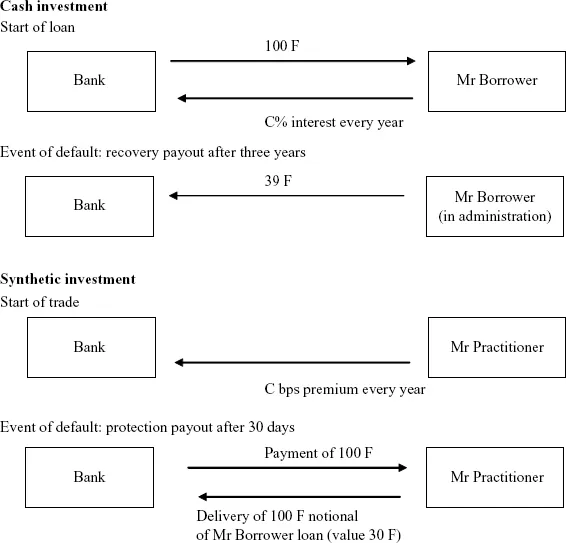

Cash Investment

At the beginning of year 3, Mr Borrower is declared bankrupt and defaults on his debt to Bank. The Bank falls in line with the other creditors, and after three years receives a payout from the administrators of 39 cents on the florin.

After five years, Bank has therefore received 2C in interest, but lost 61 florins of capital, a substantial loss.

Synthetic Investment

At the beginning of year 3, Mr Borrower is declared bankrupt and immediately Bank pays 100 florins to Mr Practitioner. In return, Mr Practitioner delivers to Bank 100 florins nominal of a loan that Mr Borrower took out from A N Other Bank. This loan has some residual value to Bank, at the time it is valued at 30 cents on the florin so Bank records a capital loss of 70 florins, a substantial loss.

After three years the Mr Borrower loan that Bank is holding is valued at 39 cents on the florin, so Bank recovers 9 florins of the loss it booked three years ago. Hence, after five years Bank has received 2C in interest, but lost 61 florins of capital, a substantial loss. The illustrations are shown in Figure 2 above.

The point we are making is that funded and unfunded investments are identical on a net-net basis, in theory anyway, and involve taking credit risk exposure in Mr Borrower’s name. The price of this risk is C%, and reflects what the market thinks of the credit quality of Mr Borrower. Of course there are some technical differences, not least the introduction of another counterparty, Mr Practitioner. But from the point of view of Bank, both trades are in essence identical; or at least have identical objectives. And the synthetic trade actually has some advantages for the investor, principally with regard to the fact that no funding is required. The counterparty risk to Mr Practitioner (principally his ability to keep up premium payments) can be viewed as a disadvantage, although there are ways to mitigate this.

![]()

CHAPTER 1

Credit Risk

Credit risk emerged as a significant risk management issue during the 1990s. In increasingly competitive markets, banks and securities houses began taking on greater credit risk from this period onwards. W...