Student Solutions Manual to Accompany Loss Models: From Data to Decisions, Fourth Edition. This volume is organised around the principle that much of actuarial science consists of the construction and analysis of mathematical models which describe the process by which funds flow into and out of an insurance system.

Trusted by 375,005 students

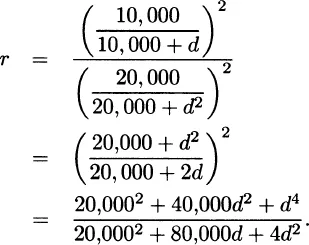

Access to over 1.5 million titles for a fair monthly price.

The solutions presented in this manual reflect the authors’ best attempt to provide insights and answers. While we have done our best to be complete and accurate, errors may occur and there may be more elegant solutions. Errata will be posted at the ftp site dedicated to the text and solutions manual: ftp://ftp.wiley.com/public/sci_tech_med/loss_models/

Should you find errors or would like to provide improved solutions, please send your comments to Stuart Klugman at [email protected].

CHAPTER 2

CHAPTER 2 SOLUTIONS

2.1 SECTION 2.2

2.1

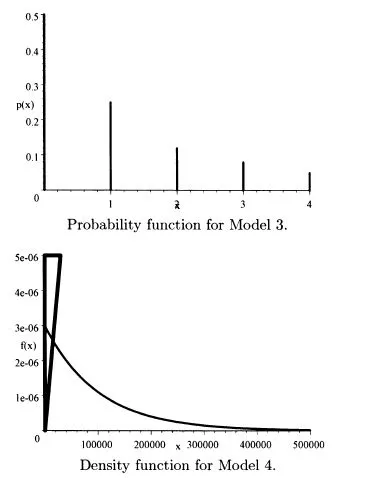

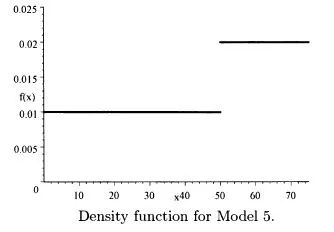

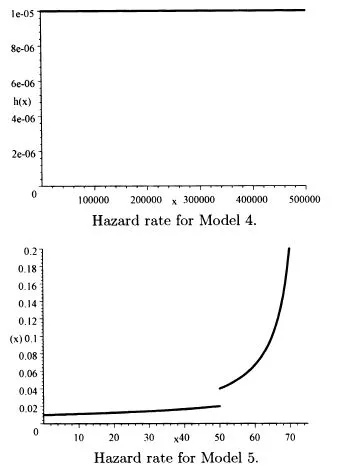

2.2 The requested plots follow. The triangular spike at zero in the density function for Model 4 indicates the 0.7 of discrete probability at zero.

2.3f′(x) = 4(1 + x2)–3 – 24x2(l + x2)–4. Setting the derivative equal to zero and multiplying by (1 + x2)4 give the equation 4(1 + x2) – 24x2 = 0. This is equivalent to x2 = 1/5. The only positive solution is the mode of

.

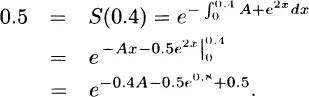

2.4 The survival function can be recovered as

Taking logarithms gives

and thus A = 0.2009.

2.5 The ratio is

From observation or two applications of L’Hôpital’s rule, we see that the limit is infinity.

CHAPTER 3

CHAPTER 3 SOLUTIONS

3.1 SECTION 3.1

3.1

3.2 For Model 1, σ2 = 3,333.33 – 502 = 833.33, σ = 28.8675.

For Model 2, σ2 = 4,000,000 – 1,0002 = 3,000,000, σ = 1,732.05.

and

are both infinite so the skewness and kurtosis are not defined.

For Model 3, σ2 = 2.25 – .932 = 1.3851, σ = 1.1769.

For Model 4, σ2 = 6,000,000,000 – 30,0002 = 5,100,000,000, σ = 71,414.

For Model 5, σ2 = 2,395.83 – 43.752 = 481.77, σ = 21.95.

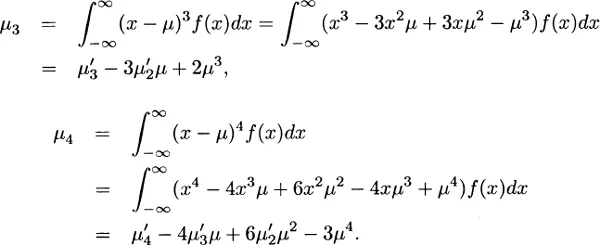

3.3 The Standard deviation is the mean times the coefficient, of Variation, or 4, and so the variance is 16. From (3.3) the second raw moment is 16 + 22 = 20. The third central moment is (using Exercise 3.1) 136 – 3(20)(2) + 2(2)3 = 32. The skewness is the third central moment divided by the cube of the Standard deviation, or 32/43 = 1/2.

3.4 For a gamma distribution the mean is αθ. The second raw moment is α(α + 1)θ2, and so the variance is αθ2. The coefficient of Variation is

/αθ = α–1/2 = 1. Therefore α = 1. The third raw moment is α(α + 1)(α + 2)θ3 = 6θ3. From Exercise 3.1, the third central moment is 6θ3 – 3(2θ2)θ + 2θ3 = 2θ3 and the skewness is 2θ3/(θ2)3/2 = 2.

3.5 For Model 1,

For Model 2,...

Table of contents

COVER

CONTENTS

TITLE PAGE

COPYRIGHT

1 INTRODUCTION

CHAPTER 2 SOLUTIONS

CHAPTER 3 SOLUTIONS

CHAPTER 4 SOLUTIONS

CHAPTER 5 SOLUTIONS

CHAPTER 6 SOLUTIONS

CHAPTER 7 SOLUTIONS

CHAPTER 8 SOLUTIONS

CHAPTER 9 SOLUTIONS

CHAPTER 10 SOLUTIONS

CHAPTER 11 SOLUTIONS

CHAPTER 12 SOLUTIONS

CHAPTER 13 SOLUTIONS

CHAPTER 14

CHAPTER 15

CHAPTER 16 SOLUTIONS

CHAPTER 17 SOLUTIONS

CHAPTER 18

CHAPTER 19

CHAPTER 20 SOLUTIONS

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Loss Models: From Data to Decisions, 4e Student Solutions Manual by Stuart A. Klugman,Harry H. Panjer,Gordon E. Willmot in PDF and/or ePUB format, as well as other popular books in Economics & Finance. We have over 1.5 million books available in our catalogue for you to explore.