Over the past few decades, Project Management has shifted from its roots in construction and defense into mainstream American business. However, many project managers' areas of expertise lie outside the perimeters of business, and most do not have the formal education in business, accounting, or finance required to take their skills to the next level. In order to succeed, today's project managers (PMs) who wish to soar to the top or remain at the helm of their profession need to have a comprehensive grasp of the business context within which they work. Providing a resourceful introduction to the interrelationships between finance, accounting, and Project Management, Project Management Accounting, Second Edition is designed to help PMs at various skill levels improve their business skills, provide advanced contributions to their organizations, and perform with greater proficiency.

Authors and industry experts Kevin Callahan, Gary Stetz, and Lynne Brooks combine their decades of Project Management experience and insights to provide professionals in the field with a 360-degree understanding of how costs interact with the general ledger. Through the authors' seasoned expertise, PMs are better equipped to assess all facets of a project with a broader understanding of the "big picture" to determine whether to continue as planned, find an alternative solution, or scrap the project altogether.

Rich with new content as well as many new case studies, this Second Edition of Project Management Accounting includes:

Updated information on Project Management and its link to Project Accounting

A new chapter on assessing risk when managing projects

How to determine the greatest tax/cost savings

Project Management in relation to a company's mission, objectives, and strategy

Project Management in an agile business

Coverage of agile Project Management as applied to software and technical projects

New, updated, and timely case studies

Sample checklists to help readers get started and apply concepts to their business

Project managers must make vital decisions every day that impact the schedule, costs, or resources committed to a given project. Project Management Accounting, Second Edition, provides the tools and skills to help PMs establish with greater certainty whether these costs should be capitalized or expensed to stay on budget and improve a company's bottom line.

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

In today's business world, we often hear the terms “strategic alignment” and “mission and objectives.” Usually these terms are used in phrases such as: “We must ensure that our business units are strategically aligned with our mission and objectives.” In many companies, large and small, it often seems that one area of a company does not know what is happening in other areas; in some cases, one area may even be working against other areas within the same company. Quite often there is a large gap between what the top levels of the organization are saying and what is happening at an operations level within the company.

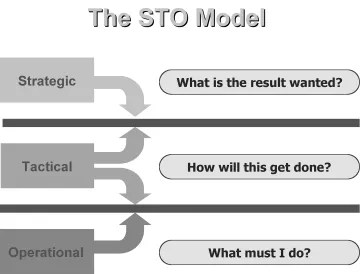

In our last book, The Essentials of Strategic Project Management, we spoke about the STO model.1 STO stands for strategic, tactical, and operational. These three levels of operation inherently have typical communication problems that many companies need to deal with (see Exhibit 1.1). Each level of the model represents a different level of a company. Strategic is the executive level, where decisions are made about the purpose and direction of the organization. Tactical is the management level of a company, where decisions are made as to how to carry out strategy. Operational is the lowest level of the company, and represents where people actually execute the work.

Exhibit 1.1 Strategic, Tactical, and Operational Model

Mission, Objectives, Strategy

In order to have a clearer understanding of what Mission, Objectives, and Strategy mean, we need to look at some definitions and examples. Mission, first of all, is a statement of the purpose for the company's existence. An example of a simple mission statement could be General Electric's: “We bring good things to life.” It is simple and easy to understand. Honeywell's mission statement is quite eloquent in its simplicity: “We are building a world that's safer and more secure, more comfortable and energy efficient, more innovative and productive.”

In each case, the company's reason for existence is stated clearly and simply, giving direction to all that the company does. The reality is, however, that carrying out that mission is usually much more complex than a simple statement. Problems arise when management is not able to turn a mission statement into action and employees do not understand how their work carries that statement forward. That situation is where mission is often confused with strategy.

Strategy consists of a series of concrete actions that a company performs in order to carry out the mission. Each concrete action is an Objective. The actions must support the mission of the company but must also adhere to good business principles. One of the fundamental responsibilities of a company is to create a return for its owners, whether they are a small group of investors or a large group of stockholders. There is always the responsibility to do this in an ethical manner, so that carrying out the mission and creating value are dual fundamental principles of any business. Even a not-for-profit company must create value; without the money, there is no mission.

An example of a Strategy that might correspond to Honeywell's Mission Statement might be to create a new line of home heating furnaces that are highly efficient and cut down on the amount of heating oil that is used to maintain the home's temperature. An Objective for that Strategy would be to carry out research into new technology for heating oil burners that are more efficient.

Problems arise in many companies when the mission is not understood at all levels, which brings us back to the STO model. When communication does not exist between the different levels of a company, mission cannot be translated into strategy and cannot be carried out by employees. Often the walls between levels exist, as illustrated in the STO model, not because of purposeful action or a desire to harm the company, but simply because no one at the firm has tried to bridge the gap or because someone has tried and failed.

As mentioned in the preface, senior project managers have their roots in many different areas of expertise, but the great majority do not come out of finance or accounting. At the same time, in order to advance within an organization, project managers need to acquire knowledge beyond their areas of expertise. The first step toward advancement is to become proficient in project management knowledge and skills in order to have the flexibility to move beyond those areas of expertise.

After becoming a proficient project manager, continued experience in project management helps project managers attain senior status. After years of managing larger and more complex projects, senior project managers often aspire to making greater contributions to their organizations. One way to do this is by gaining expertise in finance and accounting, thereby enabling them to view the organization from a different perspective and to make a greater contribution to it.

In this chapter, we review the project management phases from the perspectives of various project management deliverables and processes with an eye to related finance and accounting issues. This review serves as an introduction to how finance and accounting is related to project management and can serve to help an organization perform projects in a manner that supports sound financial and accounting management. As we review each project management phase, we discuss the questions for finance and accounting implied in that phase and indicate which chapter in this book contains pertinent information.

Information Collection

Information collection is a crucial element in project management, finance, and accounting. Collecting the correct information is crucial for project success. We conduct our review of the project management phases according to the project management documents that are created during each phase of a project:

Initiation: Project charter

Planning: Work breakdown structure, project schedule, project budget and cash flow, resource plan, procurement plan, quality plan, risk response plan

If the project is for an external client, there may be a request for proposal and corresponding proposal and a contract or some other agreement for services.

Project Execution and Control: Status reports and dashboards.

In the remainder of this section, we look to each of these documents for information that is important to understanding the financial health of the project.

Project Initiation

The project charter contains high-level information about the project, including deliverables, stakeholders, and, in particular, the definition of success for the project. That definition ought to include a description of the financial success of the project and how it will be measured. This definition provides the guidelines by which project performance may be judged.

During initiation, the first questions concerning finance and accounting are broached. For example, does the project align with the organization's strategy, in particular the financial strategy? Does the project deliver a product or service that is compatible with the goals and objectives of the organization? Will the project create value that is within the required return that the organization's financial strategy and owners or shareholders require? Often project sponsors ask what a project's return on investment (ROI) will be. In fact, project managers can increase their contribution to the organization not only by understanding a project's ROI but also by understanding in detail how that return will be delivered, over what period of time, and at what cost to the organization.

For example, let's say that a project will have a 10 percent ROI. However, if that return is over a 10-year span at 1 percent annually, it probably would not be considered as valuable as a project that will return 10 percent annually for 10 years. But even a 10 percent return over 10 years would not be very interesting if the organization's cost of capital is 15 percent. In addition, if the project is considered very risky, then the organization may require a 20 percent annual return.

Financial levers—ways in which the finances of a company can be adjusted—are explained in Chapter 2. There are additional illustrations in Chapter 3. The case study in Chapter 7 gives specific examples of how portfolio management can require criteria based on the financial strategy of the organization.

Project Planning

Work Breakdown Structure and Project Schedule

The Work Breakdown Structure (WBS) contains a description of each deliverable that makes up the final project deliverable along with the tasks that must be performed in order to create each deliverable. Each task also has a description that defines the inputs, outputs, materials, and resources required to complete the task. The task description also defines how long each resource must work to complete the task as well as how much of each material is required.

The project schedule arranges each task in its proper order of execution and indicates the order in which the tasks must be done. The project schedule also defines task dependencies, that is, which tasks must be completed before other tasks may begin. Based on these calculations, project managers know when tasks must be carried out and what the end date for the project is, as well as what its critical path will be.

Understanding how much work must be performed is crucial to creating the project budget. During execution, one of the elements of project control is collecting information about how each task is executed. If managers do not have an accurate measurement of the expenditure of resources and materials, then they cannot determine the actual cost of a project or understand how the project is performing ...

Table of contents

Cover

Content

Title Page

Copyright

Dedication

Preface

Acknowledgments

Chapter 1: Project Management and Accounting

Chapter 2: Finance, Strategy, and Strategic Project Management

Chapter 3: Accounting, Finance, and Project Management

Chapter 4: Cost

Chapter 5: Project Financing

Chapter 6: Project Revenue and Cash Flows

Chapter 7: Creating the Project Budget

Chapter 8: Risk Assessment

About the Web Site

Index

End User License Agreement

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Project Management Accounting by Kevin R. Callahan,Gary S. Stetz,Lynne M. Brooks in PDF and/or ePUB format, as well as other popular books in Betriebswirtschaft & Betriebliches Rechnungswesen. We have over 1.5 million books available in our catalogue for you to explore.