![]()

Part I

The Continuous Theory of Partial Differential Equations

![]()

Chapter 1

An Introduction to Ordinary Differential Equations

1.1 INTRODUCTION AND OBJECTIVES

Part I of this book is devoted to an overview of ordinary and partial differential equations. We discuss the mathematical theory of these equations and their relevance to quantitative finance. After having read the chapters in Part I you will have gained an appreciation of one-factor and multi-factor partial differential equations.

In this chapter we introduce a class of second-order ordinary differential equations as they contain derivatives up to order 2 in one independent variable. Furthermore, the (unknown) function appearing in the differential equation is a function of a single variable. A simple example is the linear equation

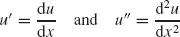

In general we seek a solution u of (1.1) in conjunction with some auxiliary conditions. The coefficients a, b, c and f are known functions of the variable x. Equation (1.1) is called linear because all coefficients are independent of the unknown variable u. Furthermore, we have used the following shorthand for the first- and second-order derivatives with respect to x:

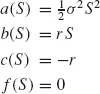

We examine (1.1) in some detail in this chapter because it is part of the Black–Scholes equation

where the asset price S plays the role of the independent variable x and t plays the role of time. We replace the unknown function u by C (the option price). Furthermore, in this case, the coefficients in (1.1) have the special form

In the following chapters our intention is to solve problems of the form (1.1) and we then apply our results to the specialised equations in quantitative finance.

1.2 TWO-POINT BOUNDARY VALUE PROBLEM

Let us examine a general second-order ordinary differential equation given in the form

where the function f depends on three variables. The reader may like to check that (1.1) is a special case of (1.5). In general, there will be many solutions of (1.5) but our interest is in defining extra conditions to ensure that it will have a unique solution. Intuitively, we might correctly expect that two conditions are sufficient, considering the fact that you could integrate (1.5) twice and this will deliver two constants of integration. To this end, we determine these extra conditions by examining (1.5) on a bounded interval (a, b). In general, we discuss linear combinations of the unknown solution u and its first derivative at these end-points:

We wish to know the conditions under which problem (1.5), (1.6) has a unique solution. The full treatment is given in Keller (1992), but we discuss the main results in this section. First, we need to place some restrictions on the function f that appears on the right-hand side of equation (1.5).

Definition 1.1. The function f(x, u, v) is called uniformly Lipschitz continuous if

where K is some constant, and x, ut, and v are real numbers.

We now state the main result (taken from Keller, 1992).

Theorem 1.1. Consider the function f(x; u, v) in (1.5) and suppose that it is uniformly Lipschitz continuous in the region R, defined by:

Suppose, furthermore, that f has continuous derivatives in R satisfying, for some constant M,

and, that

Then the boundary-value problem (1.5), (1.6) has a unique solution.

This is a general result and we can use it in new problems to assure us that they have a unique solution.

1.2.1 Special kinds of boundary condition

The linea...