![]()

Part 1

Filing Basics

- Do You Have To File a 2011 Tax Return?

- Filing Tests for Dependents: 2011 Returns

- Where To File

- Filing Deadlines

- Choosing Which Tax Form To File

- Chapter 1 Filing Status

In this part, you will learn these income tax basics:

- Whether you must file a return

- When and where to file your return

- Which tax form to file

- What filing status you qualify for

- When filing separately is an advantage for married persons

- How to qualify as head of household

- How filing rules for resident aliens and nonresident aliens differ

- How to claim personal exemption deductions for yourself, your spouse, and your dependents.

Do You Have to File a 2011 Tax Return?

| If you are— | You must file if gross income is at least |

| Single | |

| Under age 65 | $ 9,500 |

| Age 65 or older on or before January 1, 2012 | 10,950 |

| Married and living together at the end of 2011 | |

| Filing a joint return—both spouses under age 65 | 19,000 |

| Filing a joint return—one spouse age 65 or older | 20,150 |

| Filing a joint return—both spouses age 65 or older | 21,300 |

| Filing a separate return (any age) | 3,700 |

| Married and living apart at the end of 2011 | |

| Filing a joint or separate return | 3,700 |

| Head of a household maintained for a child or other relative (1.12) | |

| Under age 65 | 12,200 |

| Age 65 or older on or before January 1, 2012 | 13,650 |

| Widowed in 2010 or 2009 and have a dependent child (1.11) | |

| Under age 65 | 15,300 |

| Age 65 or older on or before January 1, 2012 | 16,450 |

Marital status

For federal tax purposes, only a man and woman in a legal union as husband and wife are considered married. For 2011 returns, marital status is generally determined as of December 31, 2011. Thus, if you were divorced or legally separated during 2011, you are not considered married for 2011 tax purposes, and you must use the filing threshold for single persons unless you qualify as a head of household (1.12), or you remarried in 2011 and are filing a joint return with your new spouse.

If your spouse died in 2011 and you were living together on the date of death, use the filing threshold shown for married persons living together at the end of 2011. If you were not living together on the date of death, the $3,700 filing threshold applies, unless you remarried during 2011 and are filing jointly with your new spouse.

Age 65

Whether you are age 65 or older is generally determined as of the end of the year, but if your 65th birthday is on January 1, 2012, you are treated as being age 65 at the end of 2011.

Gross income

Gross income is generally all the income that you received in 2011, except for items specifically exempt from tax.

Include wages and tips (Chapter 2), self-employment income (Chapter 45), taxable scholarships (Chapter 33), taxable interest and dividends (Chapter 4), capital gains (Chapter 5), taxable pensions and annuities (Chapter 7), rents (Chapter 9), and trust distributions (Chapter 11). Home sale proceeds that are tax free (Chapter 29) and tax-free foreign earned income (Chapter 36) are considered gross income for purposes of the filing test.

Exclude tax-exempt interest (Chapter 4), tax-free fringe benefits (Chapter 3), qualifying scholarships (Chapter 33), and life insurance (Chapter 11). Also exclude Social Security benefits unless (1) you are married filing separately and you lived with your spouse at any time during 2011, or (2) 50% of net Social Security benefits plus other gross income and any tax-exempt interest exceeds $25,000 ($32,000 if married filing jointly). If 1 or 2 applies, the taxable part of Social Security benefits as determined in 34.3 is included in your gross income.

Other situations when you must file

Even if you are not required to file under the gross income tests, you must file a 2011 return if:

- You are self-employed and you owe self-employment tax because your net self-employment earnings for 2011 are $400 or more (Chapter 45), or

- You are entitled to a refund of taxes withheld from your wages (Chapter 26) or a refund based on any of these credits: the earned income credit for working families; the adoption credit (Chapter 25), the additional child tax credit (Chapter 25), or the American Opportunity credit (Chapter 38), or

- You owe any special tax such as alternative minimum tax (Chapter 23), IRA penalty (Chapter 8), household employment taxes (Chapter 38), and FICA on tips (Chapter 26), or

- You are a nonresident alien with a U.S. business or have tax liability not covered by withholding; see Form 1040NR.

Filing Tests for Dependents: 2011 Returns

The income threshold for filing a tax return is generally lower for an individual who may be claimed as a dependent than for a nondependent. You are a “dependent” if you are the qualifying child or qualifying relative of another taxpayer, and the other tests for dependents at 21.1 are met.

If, under the tests at 21.1, you may be claimed as a dependent by someone else, use the chart on this page to determine if you must file a 2011 return. Include as unearned income taxable interest and dividends, capital gains, pensions, annuities, unemployment compensation, taxable Social Security benefits, and distributions of unearned income from a trust. Earned income includes wages, tips, self-employment income, and taxable scholarships or fellowships (Chapter 33). Gross income is the total of unearned and earned income.

File for Refund of Withholdings

Even if you are not required to file a return under the income tests on this page, you should file to obtain a refund of federal tax withholdings.

For married dependents, the filing requirements in the chart assume that the dependent is filing a separate return and not a joint return (Chapter 1). Generally, a married person who files a joint return may not be claimed as a dependent by a third party who provides support.

If you are the parent of a dependent child who had only investment income subject to the “kiddie tax” (24.3), you may elect to report the child’s income on your own return for 2011 instead of filing a separate return for the child; see 24.5 for the election rules.

For purposes of the following chart, a person is treated as being age 65 (or older) if his or her 65th birthday is on or before January 1, 2012. Blindness is determined as of December 31, 2011.

File a Return for 2011 If You Are a—

Single dependent. Were you either age 65 or older or blind?

- No. You must file a return if any of the following apply.

- Your unearned income was over $950.

- Your earned income was over $5,800.

- Your gross income was more than the larger of—

- $950, or

- Your earned income (up to $5,500) plus $300.

- Yes. You must file a return if any of the following apply.

- Your unearned income was over $2,400 ($3,850 if 65 or older and blind).

- Your earned income was over $7,250 ($8,700 if 65 or older and blind).

- Your gross income was more than the larger of—

- $2,400 ($3,850 if 65 or older and blind), or

- Your earned income (up to $5,500) plus $1,750 ($3,200 if 65 or older and blind).

Married dependent. Were you either age 65 or older or blind?

- No. You must file a return if any of the following apply.

- Your unearned income was over $950.

- Your earned income was over $5,800.

- Your gross income was at least $5 and your spouse files a separate return and itemizes deductions.

- Your gross income was more than the larger of—

- $950, or

- Your earned income (up to $5,500) plus $300.

- Yes. You must file a return if any of the following apply.

- Your unearned income was over $2,100 ($3,250 if 65 or older and blind).

- Your earned income was over $6,950 ($8,100 if 65 or older and blind).

- Your gross income was at least $5 and your spouse files a separate return and itemizes deductions.

- Your gross income was more than the larger of—

- $2,100 ($3,250 if 65 or older and blind), or

- Your earned income (up to $5,500) plus $1,450 ($2,600 if 65 or older and blind).

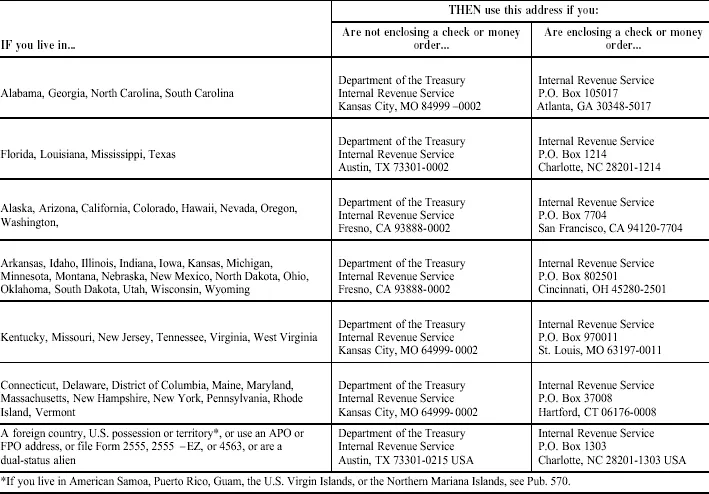

Where to File

If you filed a paper return for 2010 and also are filing a paper return for 2011, you may have to mail your return to a different address this year, as the IRS has changed the filing address for several locations; see the table below. Include your complete return address and if you are enclosing numerous attachments with your return, make sure that you include enough postage.

Check your tax form instructions and the e-Supplement at jklasser.com for any late changes.

Where Do You File Form 1040?

If you file Form 1040A or Form 1040EZ, see the note below the table.

Filing Form 1040A or 1040EZ? If you live in any of the 50 states or the District of Columbia, and are not enclosing a payment with your Form 1040A or 1040EZ, you can use the address shown above for Form 1040 (middle column) except you must change the last four digits of the zip code. The last four digits of the zip code for Form 1040A are 0015 and for Form 1040EZ they are 0014, instead of 0002 for Form 1040.

If you are enclosing a check or money order with your Form 1040A or 1040EZ, then, regardless of where you live, use the same IRS address and zip code as shown above for Form 1040 in the right column of the table.

Also use the same address and zip code shown ...