With so much emphasis on calls (especially covered calls) many traders overlook the tremendous hedging and profit potential of the put. The Amazing Put demonstrates the many strategies based on the put option, including the risk hedge, a long put (often a long-term, or LEAPS put) that freezes market risk at the put's strike (minus its premium); and the short uncovered put, which has market risk identical to the covered call.

The author methodically lays out the case for using puts wisely, both as a cash generator with low risk, and as a risk hedge to reduce or eliminate market risk in equity positions. Every options trader will benefit from exploring these strategies, and novices will gain a starting point in developing a program to enhance their stock portfolio.

Michael C. Thomsett is a market expert, author, speaker, and coach. His many books include Stock Market Math, Candlestick Charting, and Options, Tenth Edition.

1 The Flexible Nature of Options: Risks for All Levels

Are you investing in companies or in the prices of their stock? A lot of emphasis is placed on the difference between “value” and “growth,” but perhaps a more important distinction should be made between what you invest in. If you follow the fundamentals, you are probably investing in the company; if you are a technician, your interest is in the stock and its price movement.

In either case, buying and selling stock is not the only alternative you have. In fact, the volatility of the market, by itself, makes the case that just using a buy-and-hold strategy is very high-risk when markets are volatile. All you need to do is to compare prices of some of the best-known companies between the end of 2007 and 2008 to see what a disastrous market that 12 months was. This included 28 out of 30 stocks on the Dow Jones Industrial Average, which all lost value.1

In the bull market between 2016 and 2018, the DHIA increased over 8,000 points from the 2016 election onward. Most DJIA stocks also grew. Only 13 months after the election, 8 Dow Stocks soared more than 50%, as shown in Table 1.1.2

Table 1.1:Eight best-performing Dow Stocks.

Company

% growth

American Express

50.4%

McDonald’s

52.2

Home Depot

53.3

J.P. Morgan

55.7

Apple

55.8

UnitedHealth

57.1

Caterpillar

88.3

Boeing

108.6

The point is that strong markets—either bearish or bullish—tend to change valuation significantly, often in a short period of time. The table reflects only 13 months of the market. In any strong markets, options—both calls and puts—can be used as hedging vehicles to reduce and even eliminate market risks. Options, when used to hedge, are vastly different than stocks.

When you buy shares of stock, you enter into a rigid contract. You pay money for shares, which either increase or decrease in value. You are entitled to dividends if the company has declared and paid them. And if you own common stock, you have the right to vote on corporate matters put forth by the board of directors. The stock remains in existence for as long as you want to continue owning shares, and you have the right to sell those shares whenever you wish.

With options, the contract is different. An option controls 100 shares of stock but costs much less. However, holding an option grants no voting rights and no dividends (unless you also own the stock). You can close an option position at any time you want on listed options on stock. But perhaps the most important distinction between stock and options is that options have only a finite life. They expire at a specified date in the future. After expiration, the option is worthless. It must be closed or exercised before expiration to avoid losing all its value. You exercise a put by selling 100 shares at the fixed strike price; and you exercise a call by buying 100 shares at the fixed strike price.

Key Point: Stock and option terms are quite different, including indefinite versus finite lives, dividends, and voting rights.

Options, in general, contain specific terms defining their value and status. These terms include the type of option (put or call), the underlying security, the strike price, and expiration date. Every option’s terms are distinct; listed option terms cannot be changed or exchanged other than by closing one option and replacing it with another.

Terms of Options

The terms of each option contract define it and set value (known as premium) for each option contract. These terms are:

Type of Option

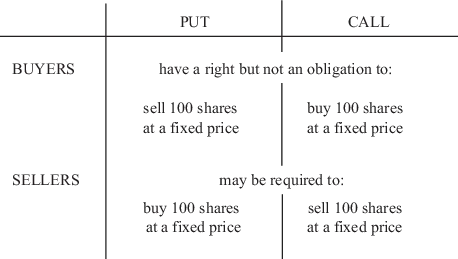

There are two kinds of options, puts and calls. A put grants its owner the right, but not the obligation, to sell 100 shares of a specific underlying security, at a fixed strike price, and before the specified expiration date. A seller of a put may be obligated to buy 100 shares at the fixed strike price, which occurs when the market value of stock is lower than the put’s strike price.

A call is the opposite. If you buy a call, you have the right, but not the obligation, to buy 100 shares of a specific underlying security, at a fixed strike price, and before the specified expiration date. A seller of a call may be obligated to sell 100 shares at the fixed strike price, which occurs when the market value of stock is higher than the call’s strike price.

Key Point: Holders of long positions are not obligated to exercise, but their positions give them leveraged control over 100 shares of stock per contract.

The rights and obligations of option buys and sellers are summarized in Figure 1.1.

Source: Prepared by author.

Figure 1.1: Option rights and obligations.

Put values rise if the underlying security’s share price falls. This occurs because the fixed strike price does not change; the lower the current price of the stock, the more valuable the right to sell 100 shares at the higher strike price. For a call, the value rises when the underlying security price increases; the higher the current price of the stock, the more valuable the right to buy 100 shares at the lower strike price.

For example, if you buy a put with a strike price of 35 and the stock’s market value falls to $28 per share, you gain a 7-point advantage. You can sell 100 shares of stock at the strike price of $35, or $700 higher than the current market value of the stock. If you buy a call with a strike price of $40 and the stock’s market value rises to $44 per share, your call grants you the right to buy 100 shares at the strike price of $40, or $400 below current market value.

These basic attributes of options form the rationale for all strategies. These may consist of one or more option positions, short or long, or combinations of various kinds. For example, options may be used to hedge stock position risks; they may be built with combinations of call with call, call with put, or put with put in a variety of long or short positions and employing one or many different strike prices. The strategic possibilities are endless and provide hedging and insurance for many positions and in many kinds of markets.

Underlying Security

The underlying security may be 100 shares of stock, an index, or a futures position. This book limits examples to options on stock, which are the most popular in the options market and the most likely kind of underlying security most people will use for option trading. The underlying cannot be changed. Once you open a long or short option position, it is tied to the underlying and will gain or lose value based on the direction the stock moves.

Key Point: Every option position relates to a specific underlying security, and this is not transferable.

The underlying may have a narrow trading range, or it may be volatile. The degree of price volatility in the underlying (market risk) also affects option premium values. The greater the volatility, the greater the value of the option. This volatility premium, also called extrinsic value, will change as the expiration date approaches; but for longer-term options, the volatility of the underlying is a significant portion of total premium value. The attributes of the underlying are essential for judging the value of options. It is a mistake to determine which options to buy or sell based solely on their current value; the quality of a company on a fundamental basis, as well as the price volatility of its stock (or its technical risk attributes) must be compared and judged to make an informed trade decision.

Strike Price

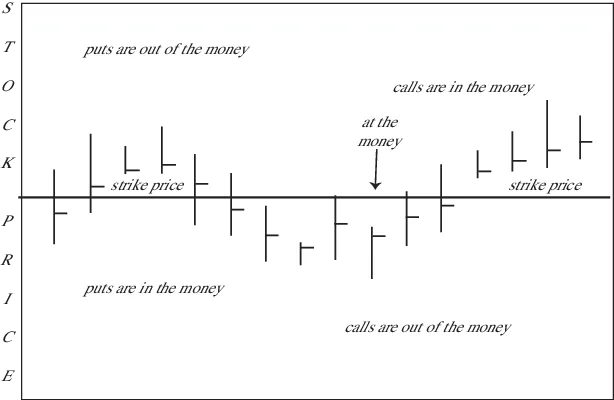

Strike price is the fixed price at which an option can be exercised. The strike price determines total option value. The proximity between strike and the current value of each share of stock determines whether premium value is growing or shrinking. When a put’s strike is higher than the current market value of the underlying stock, it is in the money; and when a call’s strike is lower than the current market value of the underlying stock, it is also in the money. If the stock’s price moves above the put’s strike or below the call’s strike, then the option is out of the money. If stock share price and the option’s strike price are the same, the option is at the money.

Key Point: The proximity between strike price and current market value of the underlying determines the premium values of every option.

These relationships between strike of the option and current value of the underlying security is referred to as moneyness; this is summarized in Figure 1.2.

Source: Prepared by author.

Figure 1.2: Option moneyness.

Expiration Date

An option’s expiration date is fixed and cannot be changed. It occurs after the third Friday of the expiration month. Standard listed options expire up to eight months out, and the longer-terms option (LEAPS, or Long-term Equity Anticipation Securities) expires up to 30 months away.

The time to expiration determines how options are valued. The longer the time, the greater the portion of an option’s premium known as time value. It may be quite high when options have many months to go before they expire, but as expiration nears, the decline in time value accelerates. By expiration day, time value falls to zero.

Key Point: The fact that options expire means value is also finite; unlike stock, every option becomes worthless as soon as the expiration date has passed.

For option buyers, time is a problem. If you buy an option with a long time until the expiration date, you will have to pay for that time in higher premium; if expiration will occur soon, premium is lower but the rapid decline in time value makes it difficult to create a profit. Three-quarters of all options expire worthless, making the point that it is very difficult to beat the odds simply by speculating in long puts or calls.

In comparison, option sellers (those who sell options rather than buying them) have an advantage in the nature of time value. Because it declines as expiration approaches, short positions are more likely to be profitable. Short sellers go through a process of sell-hold-buy rather than the traditional long position, which involves the process of buy-hold-sell. The more decline in an option’s premium, the more profitable the short position. Expiration is a benefit to option sellers and a problem for option buyers.

Valuation of Options

Every option has an overall value, known as its premium. But the total premium consists of three specific parts: intrinsic value, time value, and extrinsic value. The first two are quite easy to understand, but extrinsic value is where all the variations are going to be found. For example, if you look at two stocks with the same market value and with options for the same strike and expiration, you are still going to find differences in those option premiums. The reasons are explained by extrinsic value.

Intrinsic Value

The option’s intrinsic value is easy to understand. It is the point value equal to the option’s in-the-money level. For example, a 30 put has three points of intrinsic value when the underlying stock is at $27 per share ($30 − $27 = $3). If the stock’s value is higher than the put’s strike, there is no intrinsic value.

Key Point: Intrinsic value is equal to the number of points between strike price and current market value above (for a call) or below (for a put).

A call has intrinsic value whenever the underlying stock is higher than the call’s strike. For example, if the strike is 45 and the current value of the underlying is $51 per share, the call has six points of intrinsic value ($51 − $45 = $6).

Intrinsic value will always track with the underlying stock’s price movement. ...

Table of contents

Title Page

Copyright

Contents

Introduction to the Second Edition: Managing and Exploiting Volatility

1 The Flexible Nature of Options: Risks for All Levels

2 Puts, the Other Options: The Overlooked Risk Hedge

3 Profit-taking Without Selling Stock: An Elegant Solution

4 Swing Trading with Puts: Long and Short or Combined with Calls

5 Put Strategies for Spreads: Hedging for Profit

6 Put Strategies for Straddles: Profits in Either Direction

7 Puts in the Ratio Spread: Altering the Balance

8 Puts as Part of Synthetic Strategies: Playing Stocks Without the Risk

9 Puts in Contrary Price Run-Ups: Safe Counter-plays During Bear Markets

10 Uncovered Puts to Create Cash Flow: Rising Markets and Reversal Patterns

11 Uncovered Puts in Recovery: An Essential Strategy to Offset Loss

12 Puts and Risk: A Range of Risk Levels and a Conservative Trading Goal

Glossary

Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Amazing Put by Michael C. Thomsett in PDF and/or ePUB format, as well as other popular books in Business & Investments & Securities. We have over 1.5 million books available in our catalogue for you to explore.