In 2002, I found a website that charged a small monthly fee to give information on properties in foreclosure. This website tracked lenders who filed foreclosure proceedings against homeowners more than 60 days behind on their mortgage payments. I quickly learned that many investors, like myself, would send a letter of interest to homeowners who were in pre-foreclosure stage in order to see if a deal could be worked out to buy the home before the property was foreclosed by the bank and sold at auction.

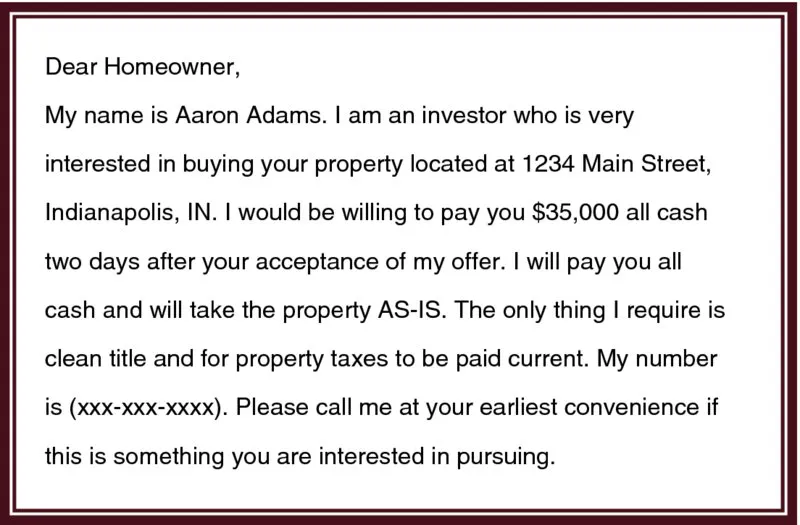

I wracked my brain trying to think of a way to distinguish my letters from the ones other investors sent to homeowners in pre-foreclosure. I decided the best method would be to attempt to contact the homeowners personally. If I could connect with them, I could convince them to work with me in selling their homes.

Three Stages of Foreclosure

- Pre-Foreclosure: Owner is behind on his mortgage payments.

- Foreclosure: Property is auctioned off at public auction.

- REO: Property is not sold at auction, goes back to the bank (Real Estate Owned) and is usually listed with an REO broker.

In today’s real estate market, most homeowners who are in pre-foreclosure stage are upside down on their homes. This means they owe more for their mortgage than what their home is worth. But in California in 2002, market value was going up at a record pace. There were some areas of Riverside County, where I lived, where the values were increasing 4 to 6% per month. I knew that all I had to do was get a deal under contract, and the rapid appreciation in the market would handle the rest for me.

Searching the foreclosure website I paid a subscription to, I found a home near me on which the homeowners had a $60,000 balance owed for their mortgage. They had borrowed about $70,000 originally (payment of about $765/month) and had paid it down to $60,000. They were two months behind on payments, and there was a good chance they would lose the home in a couple more months. I drove by the home and could tell, from the exterior and from the neighborhood it was in, that it was worth over $100,000.

The next day I put together a letter similar to the one I outlined in Chapter 1. But instead of mailing the letter, I took it to the house. When I knocked on the door, a 6’2”, 300-pound Hispanic man answered. He did not look happy to see me. Drawing on my experience of the two years I spent in Venezuela as a missionary, I cleared my throat and said, “Hello, I am sorry to bother you . . . my name is Aaron Adams, and I wanted to come by and offer you $60,000 cash for this house.” Somewhat surprised, he stared at me for a good ten seconds and said (in broken English), “You are not selling nothing?” I immediately switched to Spanish and repeated my offer. Within five minutes I was invited into the house, seated, drinking a soda, and outlining my terms.

One of the first questions I was dying to ask was why they hadn’t just thrown the house on the market for $70k and listed it for a quick sale. They explained that even after losing their jobs, they believed they were going to get caught up on the mortgage. Furthermore, by the time they starting going through all the mail they had received from other investors like me, they were confused. Thinking they were going to be scammed, they decided to let the bank auction the property. This decision was reinforced by some friends from their church who had lost a home to foreclosure and had actually been sent a check after the auction, because the home had sold for even more than they owed for the payoff plus penalties plus fees. They figured it would be the least complicated way to get out of the whole situation.

Over the next week, I met with this family no less than ten times. Although they agreed to sell me the house for $65,000, they also hit me up for money to rent a U-Haul, to hire someone to help them load up the truck, an...