"Life on earth is filled with many mysteries, but perhaps the most challenging of these is the nature of Intelligence."

– Prof. Terrence J. Sejnowski, Computational Neurobiologist

The main objective of this book is to create awareness about both the promises and the formidable challenges that the era of Data-Driven Decision-Making and Machine Learning are confronted with, and especially about how these new developments may influence the future of the financial industry.

The subject of Financial Machine Learning has attracted a lot of interest recently, specifically because it represents one of the most challenging problem spaces for the applicability of Machine Learning. The author has used a novel approach to introduce the reader to this topic:

The first half of the book is a readable and coherent introduction to two modern topics that are not generally considered together: the data-driven paradigm and Computational Intelligence.

The second half of the book illustrates a set of Case Studies that are contemporarily relevant to quantitative trading practitioners who are dealing with problems such as trade execution optimization, price dynamics forecast, portfolio management, market making, derivatives valuation, risk, and compliance.

The main purpose of this book is pedagogical in nature, and it is specifically aimed at defining an adequate level of engineering and scientific clarity when it comes to the usage of the term "Artificial Intelligence," especially as it relates to the financial industry.

The message conveyed by this book is one of confidence in the possibilities offered by this new era of Data-Intensive Computation. This message is not grounded on the current hype surrounding the latest technologies, but on a deep analysis of their effectiveness and also on the author's two decades of professional experience as a technologist, quant and academic.

“You never change things by fighting the existing reality. To change something, build a new model that makes the existing model obsolete.”

– Buckminster Fuller, inventor, system theorist

1.1 INFRASTRUCTURE-RELATED PARADIGMS IN TRADING

Since the beginning of human civilization, commerce has been the main engine of progress. The Cambridge dictionary defines commerce as “the business of buying and selling products and services.” The exchange of valuables has been the main driver of progress in any type of economy throughout history, and it was primarily accomplished through trading. The mechanism of trading is considered to have been the main instrument that linked different peoples and acted as the main channel of communication for cultural and intellectual exchange. The primal forms of trade appeared when prehistoric peoples started exchanging valuables for food, shelter, and clothing. The concept of exchange for sustenance became a reality in a physical space known as the marketplace. The concept of a marketplace as an area designated for the exchange of goods or services became associated with a set of rules to operate within it. As human civilization progressed and the sophistication of trading practices advanced, the need for more modern avenues to trade have become prevalent, and the world of financial instruments was created. Pioneering markets, like the Dojima Rice Market or the Amsterdam Stock Exchange, were the early promoters of modern trading, transacting products such as equities, futures contracts, and debt instruments.

The long history of trading (Spicer 2015) as the main vehicle to exchange valuables and information could be studied by considering the evolution of different trading paradigms. Since a paradigm is a conceptual representation for looking at, classifying, and organizing a specific human endeavor, one can look at trading paradigms from two different perspectives:

The infrastructure required to establish a marketplace, and

The methods required to support and generate trading decisions.

Since the dawn of the financial markets, trading was strongly associated with the technological progress of the time, by heavily employing the most recent breakthroughs. This section is meant to be a very brief history of the love affair between trading and technology.

1.1.1 Open Outcry Trading

In its earliest manifestation, trading took place in a setting called the open outcry system. This mechanism of transacting involved the matching of buyers and sellers through direct, face-to-face verbal communication, where the information exchanged consisted of bids and offer prices that were shouted out loud, thus the outcry designation. This primal system of trading developed out of the necessity for market participants to see and verbally communicate with one another. The technology-enabling direct communication had yet to be invented. Within this early paradigm of trading, the process of price discovery was initiated by an oral auction for a certain asset. As supply and demand forces interplayed, the debate over the value of the auctioned asset was settled. The access to this kind of marketplace was limited both by monopolistic associations and by capital requirements. However, over time the transactions taking place in the open outcry system became more securitized and the appetite to engage in speculative trading increased. In order to service the growing demand, the nascent trading industry had to consolidate into so-called exchanges, and it started using more and more of the technology available at the time. As the demand to access these markets increased, new marketplaces and financial products came into being. The creation of futures and forward contracts enabled extensive hedging practices for agricultural producers. The introduction of bonds serviced corporate and government debt and satisfied the desire of investors and speculators to grow their capital. From the mid-nineteenth century to the late-twentieth century, open outcry markets commenced trading on a large scale and became the backbone of the financial industry.

1.1.2 Advances in Communication Technology

As the vast majority of trading operations remained largely contained to the traditional open outcry marketplaces, the technological progress achieved during the nineteenth and twentieth centuries generated growth in market participation. Inventions like the telegraph, the ticker tape, and the telephone established the foundations for today's computerized trading systems. The invention of the telegraph by Samuel Morse in 1832 was quickly adopted by the trading industry. As a result, financial information was quickly disseminated to areas far away from the usual marketplaces. By the mid-1850s, broker-assisted financial transactions of exchange-based securities became a reality by using the telegraph.

The first stock ticker was implemented by the New York Stock Exchange in 1867. Edward Callahan invented the stock ticker by adapting the telegraph technology to transmit up-to-the-minute stock quotes originating at the NYSE nationwide. This new technology created a new service that facilitated the reception of streaming market data by remote traders. The invention of the telephone in 1876 augmented the potential of the telegraph by providing bi-directional means of communication between market participants. As such, the telephone became a fundamental component for the infrastructure of the financial industry as it developed into the industry's standard for interacting remotely with a marketplace.

The development of the Electronic Numerical Integrator and Computer (ENIAC) in 1946 marked the beginning of the computer age. This was also a major development in the history of the financial markets. The ENIAC was one of the first digital general-purpose computers that were able to solve a large class of numerical problems via reprogramming. The financial industry recognized immediately this event as a technological breakthrough that could be readily adapted to perform many market-related tasks. By the early 1960s, computer-based market data services started to replace the traditional ticker-tape quotation services.

The inventions of the telegraph, ticker tape, and telephone all contributed to the growth of marketplaces and exchanges in both the United States and Europe. When coupled with the computational power developed by the breakthroughs in information systems technology, the stage was set for the rapid evolution of computerized trading systems and electronic trading.

1.1.3 The Digital Revolution in the Financial Markets

With the development of the first computerized stock quote delivery system in the early 1960s, the financial markets began the transition toward full automation. The availability of streaming real-time market quotes made possible the democratization of the financial markets as the dissemination of market information in real-time was a far more efficient medium than using ticker tapes or the telephone.

Instinet was developed in 1969 as the first fully automated system to trade US securities, and this was done by leveraging the digital exchange-based streaming quote technology developed a decade earlier. By using the Instinet trading system, large institutional investors were able to trade pink sheet securities directly with one another in a purely electronic over-the-counter (OTC) manner. This event marked the birth of the electronic trading era and the departure from the ancient practice of open outcry. Many new competitors jumped into this very hot market where technology was the name of the game. All traditional brick-and-mortar exchanges started automating their trade processing in order to be able to compete in this brave new world where Electronic Communications Networks (ECNs) gained so much traction.

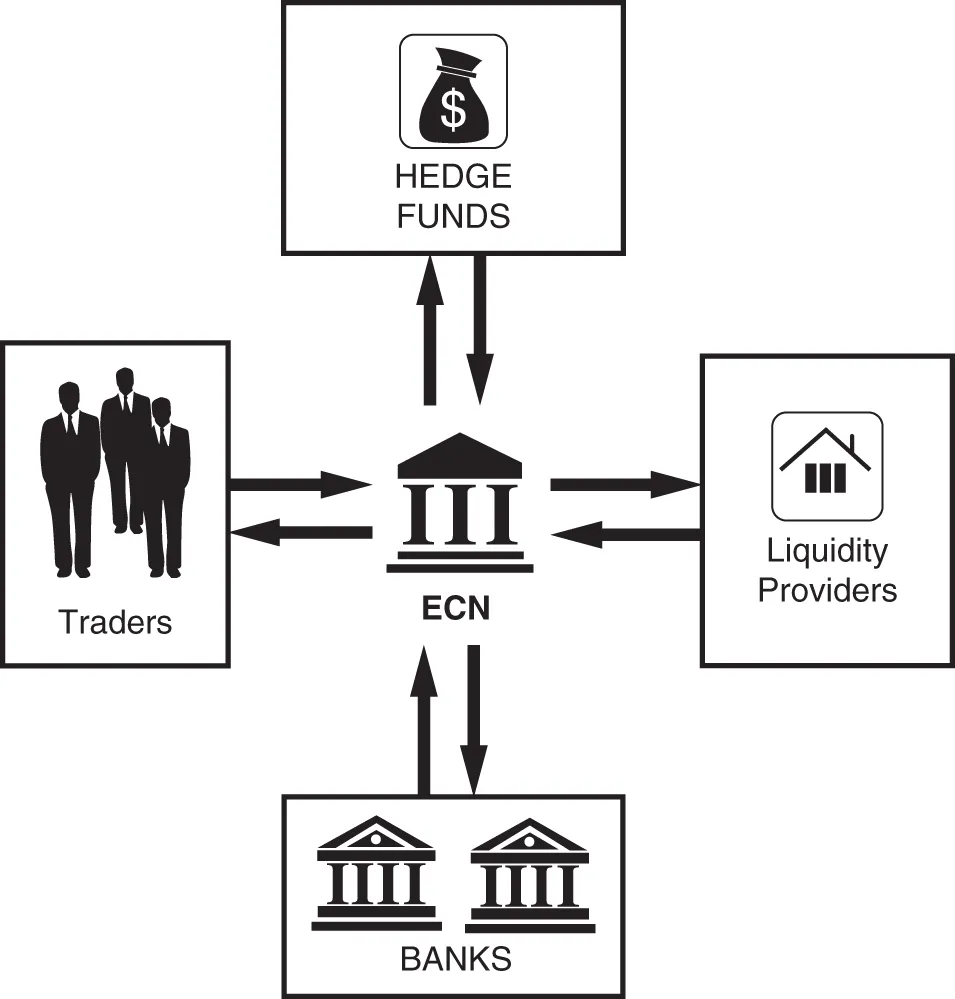

ECNs are digital networks that facilitate the trading of financial products outside traditional exchanges (see Figure 1.1). These digital systems disseminate orders originated by market makers to third parties and allow these orders to be executed against either partially or completely. ECNs are generally passive computer-driven networks that could internally match limit orders by charging a very small transaction fee, making them extremely competitive in the marketplace.

FIGURE 1.1 The ECN concept.

The year 1971 saw the birth of NASDAQ as a fully automated OTC trading system. As Instinet did a few years earlier, NASDAQ employed state-of-the-art information technology systems to create a 100% digital trading infrastructure. This innovative model was soon followed by NYSE, which in 1976 created the Designated Order Turnaround (DOT) system, allowing their member firms to connect electronically direct to the exchange. The SuperDOT system launched in 1984 marked a disruptive leap in equities trade execution in terms of both speed and volume. Ten years later, the SuperDOT system was capable of processing trading volumes of one billion shares per day, with a standard response time from floor to firm of 60 seconds or less.

With all the progress achieved in the digitization of the US equity markets, the open outcry remained the preferred way of trading in many futures and options markets until the turn of the twenty-first century. But as Internet connectivity technology evolved and personal computers became more powerful and affordable, the push toward market automation took over the last open outcry holdovers. During the last decade of the twentieth century, the digital revolution of the financial markets went on full gear driven by both institutional investors as well as individual retail traders.

The diminishing demand for open outcry trading in the United States coupled with the direct competition from the electronic trading markets in Germany and the United Kingdom provided the conditions for a global move toward the full automation of financial markets. Leading global exchanges like the Chicago Mercantile Exchange launched web-based trading applications (the Globex platform) that enabled clients to trade exclusively using online trading platforms. Just during the last decade of the twentieth century, one billion futures contracts have been traded electronically on the CME Globex platform. This electronic trading paradigm increased the overall efficiency of the marketplace in ways that were not foreseeable just a few decades before. As a result, greater liq...

Table of contents

Cover

Table of Contents

About the Author

Acknowledgments

About the Website

Introduction

CHAPTER 1: The Evolution of Trading Paradigms

CHAPTER 2: The Role of Data in Trading and Investing

CHAPTER 3: Artificial Intelligence – Between Myth and Reality

CHAPTER 4: Computational Intelligence – A Principled Approach for the Era of Data Exploration

CHAPTER 5: How to Apply the Principles of Computational Intelligence in Quantitative Finance

CHAPTER 6: Case Study 1: Optimizing Trade Execution

CHAPTER 7: Case Study 2: The Dynamics of the Limit Order Book

CHAPTER 8: Case Study 3: Applying Machine Learning to Portfolio Management

CHAPTER 9: Case Study 4: Applying Machine Learning to Market Making

CHAPTER 10: Case Study 5: Applications of Machine Learning to Derivatives Valuation

CHAPTER 11: Case Study 6: Using Machine Learning for Risk Management and Compliance

CHAPTER 12: Conclusions and Future Directions

Index

End User License Agreement

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access Applications of Computational Intelligence in Data-Driven Trading by Cris Doloc in PDF and/or ePUB format, as well as other popular books in Business & Trading. We have over 1.5 million books available in our catalogue for you to explore.