The Earned Value Management Maturity Model® gives you the fundamental tools needed to build an effective Earned Value Management System (EVMS). This must-have resource makes earned value management easy by defining a maturity model and describing metrics to measure the health and efficiency of your EVMS. Discover valuable ways to improve your EVMS and achieve project success. Through point by point discussions, you will: • Gain fundamental knowledge of Earned Value Management (EVM) • Learn how EVM can be applied to a team, project, program, or organization • Understand how to define what your organization wants from its EVMS • Discover a five stage maturity model for EVMS implementation • Bring your EVMS in line with ANSI 748 guidelines • Review many real or imagined impediments to implementing EVM and how to overcome the real ones PLUS — You'll gain practical EVM experience through a comprehensive case study that follows a fictional company and newly hired project manager. By applying the EVM knowledge and skills covered in the book, the project manager illustrates the ease of implementing an effective EVMS!

Implementing any new process involves cultural change, emotional and financial investment, and acceptance of new ways of doing the familiar. So, why are more and more organizations opting to endure these difficult transitions to implement earned value management? Simply stated, over 30 years of experience demonstrate that earned value management is one of the most effective means available to monitor project cost and schedule performance.

Today’s projects operate in an environment of overcommitted resources, demanding stakeholders, and changing technologies. Corporate fiduciary responsibilities are increasing, and CEOs and CFOs must forecast earnings that may be dependent on both their internal projects and customers’ projects. The current status of projects, their likely completion date, and their final cost are crucial data items that CEOs and CFOs must possess. Earned value management provides a powerful tool for obtaining these data.

Earned value management is applied toward the end of the project planning effort and is dependent on good project plans. Because it is a way of instrumenting a project for monitoring cost and schedule during project execution and control, it quickly reveals poor project planning or the inability to execute a good plan. During project execution and control, earned value management provides insight into the project’s current cost and schedule status, helping the project manager balance the triple constraints of cost, schedule, and requirements.

Three metrics form the basis for earned value management (they are explained in more detail later in this chapter). At any point in the project, these three metrics reveal:

• The project work that should have been completed

• The work actually completed

• The cost of completing that work

It may appear that earned value management adds little to the traditional concepts of project monitoring. Any project manager should know what is to be delivered, what has been delivered, and how much has been spent delivering it. However, the power of earned value management is its ability to shift the point of view from deliverables planned, deliverables completed, and funds spent to the value of work planned, the value of work done, and the funds spent. This transformation to an all-economic basis allows analysis that is otherwise not possible.

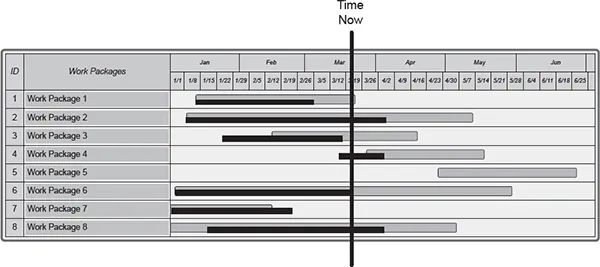

To understand the limitations of traditional project metrics, consider the common practice of monitoring projects using a schedule (or a list of met and unmet milestones) and a financial report. The schedule (Figure 1-1) reveals the activities started, completed, underway, early or late in starting, and early or late in being completed. The schedule provides a general sense of current project status by comparing where each activity stands relative to its planned status. However, the schedule does not differentiate between types of activities: some are small efforts and some are large efforts, some are on the critical path and some are not. The schedule may be able to provide a qualitative sense of the project being ahead or behind schedule, but quantifying the schedule condition is difficult or impossible.

Figure 1-1. Typical Gantt Char

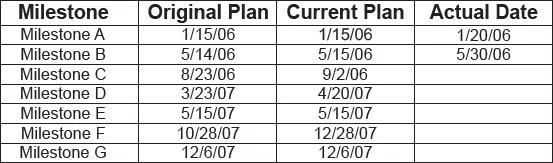

You might look at a list of milestones (Figure 1-2) or deliverables and compare the planned completion dates with the current status. Here you have even less information than you did when looking at the schedule. Some milestones were supposed to be met at this point and some milestones have been met. Some milestones may have actual dates different from the planned dates, other milestones may have a best guess completion date different from the planned completion date. Using a list of milestones, you might obtain some qualitative insight into the project’s progress, but you don’t have enough quantitative information for any depth of analysis.

Figure 1-2. List of Milestones

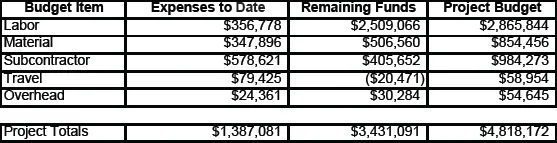

The project financial report (Figure 1-3) reveals how much of the total project budget has been spent. However, it cannot provide answers to such questions as: “Were the funds spent well?” or “Was any work completed?” Without such information it is impossible to know whether the project budget will ultimately be underrun or overrun. All that is known is that money has been spent on the project.

Earned value management quantifies project progress and compares actual progress to planned progress and funds spent. It does so using three metrics: Planned Value (value of work planned to be completed), Earned Value (value of work actually completed), and Actual Cost (funds spent). These parameters are determined for each project time period, and also cumulatively from project inception. While some suggest that earned value management is difficult, it really only adds one element to traditional project management—Earned Value.

Figure 1-3. Summary Financial Report

Earned value management provides information that is useful to all levels of management. The project manager can use earned value management data to help manage the project. Team leaders can use these data to help manage their teams. Program managers and project portfolio managers can use earned value management data collected across all their projects to help identify poor project performance, reallocate resources, reset priorities, and terminate efforts that are likely to fall short of return-on-investment expectations. Chief project officers and CFOs can forecast project expenditures and completion dates, allowing better predictions of corporate revenues, expenditures, and profits. The CFO can employ these forecasts to develop financial statements detailing next year’s projected corporate financial outlooks. Moreover, earned value management data can provide data for reports required under the Sarbanes-Oxley Act of 2002.1

Whether the industry is information technology, new product development, aerospace, pharmaceuticals, construction, or any other, earned value management provides valuable project insight for any project stakeholder, from the team leader to a corporate stockholder.

Earned Value Management

• Provides useful information for all levels of management

• Is applied to projects at the end of the planning cycle

• Requires good project planning

• Provides instrumentation for monitoring cost and schedule performance

• Helps balance the triple constraints of cost, schedule, and quality

• Provides the value of work completed

• Can estimate project completion date and final cost

• Assists in developing forecasts of corporate financials for project-based businesses

NOTE

1. The Sarbanes-Oxley Act of 2002 is a U.S. government regulation that increases the responsibility of corporate CEOs and CFOs to accurately report their companies’ financial condition and financial outlook. It requires that “financial statements and disclosures fairly present, in all material respects, the operations and financial condition of the issuer.” For a corporation whose primary revenue is from the completion of projects, earned value management data should be a key component in development of these forecasts.

CHAPTER 2

Basic Concepts of Earned Value Management

Percentage spent is not percentage done! Does this statement surprise you? Many projects exceed their budget yet still fail to deliver the promised outcome. If percentage spent was percentage complete, when 100% of the project budget is spent the project would be done and everyone would be happy. Most project managers know firsthand this is rarely the case. Percentage spent simply makes a statement about financial expenditures; it is not an indicator of project progress.

The same holds true for time. Spending time on a project does not mean the work is being accomplished at an appropriate pace, or even that the right work is getting done. It just means that the clock on the wall has moved forward.

Schedules can provide some insight as to progress, as can deliveries or completed milestones. But is the completed work worth what was spent to get it done?

Earned value management asks you to think about what has been accomplished without thinking about how much has been spent or how much schedule time has been consumed. Understanding this concept, and using it in estimating the work completed, is the major cultural impediment to using earned value management correctly.

PLANNED VALUE: THE PLANNED VALUE OF WORK

The most fundamental concept of earned value is that work is worth the planned or negotiated value (budget) of the work. Depending on the industry, this value might be set by a formal contract, an annual budget, or a price to be paid for the end product. This concept flows down into the project as teams, subcontractors, and vendors agree to provide certain goods or services for a set budget or contract. Earned value uses the budget as the metric to answer the question “How much work do you have to do?” In earned value management terminology, scope is synonymous with budget.

A $10 million budget means that the sponsor (customer, stake-holder, resource provider, etc.) agrees that the project results are valued at $10 million. Otherwise, the two parties would have agreed on a different value. The value simultaneously represents two separate concepts: (1) the expectation of spending $10 million and (2) the work is worth $10 million. (The inclusion of contingency funds in earned value management will be discussed later.)

For example, consider building a custom home. You ask an architect to design a home worth $500,000. The architect looks at the local housing market and develops blueprints for a home worth $500,000. You select a contractor to build the home and upon completion you receive a bill for $600,000. You pay the bill, reluctantly, consoling yourself with the thought that you now own a $600,000 home. It comes as a surprise when the local real estate broker exclaims, “You have a nice half-million dollar home.” The value of the work is not what you pay for it; it is what you agreed it’s worth at the start.

Planned Value is the earned value management term for the value of work. The Planned Value is the value of all project activities. While it might sound like the project budget, it really is the sum of each activity’s time-phased budget, created by associating the applicable budget to each detailed work activity and the work schedule. Thus, each piece of work has two attributes: its value (allocated budget) and its planned completion date (allocated time, or schedule). The sum of the Planned Value for all project activities should equal the total project budget, less any funds set aside for risk management or not yet allocated to a specific activity. Today’s powerful scheduling tools, resource pools, and planning make it easy to determine the Planned Value. It is simply the cost of resources to be applied to activities over their time frame.

For example if an activity is planned for four months, and is expected to use one person in month one and t...

Table of contents

Cover

Title Page

Copyright Page

Dedication

Contents

Preface

Foreword

Part I: Earned Value Management Basics

Part II: Implementing Earned Value Management via the Earned Value Management Maturity Model

Appendices

Index

Trusted by 375,005 students

Access to over 1.5 million titles for a fair monthly price.

Study more efficiently using our study tools.

Frequently asked questions

Yes, you can cancel anytime from the Subscription tab in your account settings on the Perlego website. Your subscription will stay active until the end of your current billing period. Learn how to cancel your subscription

No, books cannot be downloaded as external files, such as PDFs, for use outside of Perlego. However, you can download books within the Perlego app for offline reading on mobile or tablet. Learn how to download books offline

Perlego offers two plans: Essential and Complete

Essential is ideal for learners and professionals who enjoy exploring a wide range of subjects. Access the Essential Library with 800,000+ trusted titles and best-sellers across business, personal growth, and the humanities. Includes unlimited reading time and Standard Read Aloud voice.

Complete: Perfect for advanced learners and researchers needing full, unrestricted access. Unlock 1.5M+ books across hundreds of subjects, including academic and specialized titles. The Complete Plan also includes advanced features like Premium Read Aloud and Research Assistant.

Both plans are available with monthly, semester, or annual billing cycles.

We are an online textbook subscription service, where you can get access to an entire online library for less than the price of a single book per month. With over 1.5 million books across 990+ topics, we’ve got you covered! Learn about our mission

Look out for the read-aloud symbol on your next book to see if you can listen to it. The read-aloud tool reads text aloud for you, highlighting the text as it is being read. You can pause it, speed it up and slow it down. Learn more about Read Aloud

Yes! You can use the Perlego app on both iOS and Android devices to read anytime, anywhere — even offline. Perfect for commutes or when you’re on the go. Please note we cannot support devices running on iOS 13 and Android 7 or earlier. Learn more about using the app

Yes, you can access The Earned Value Management Maturity Model by Ray W. Stratton PMP, EVP in PDF and/or ePUB format, as well as other popular books in Business & Forecasting. We have over 1.5 million books available in our catalogue for you to explore.