Chapter 1: Why Do We Invest?

1.1 Introduction. 1

1.2 Assumptions. 2

1.3 Annualized Return. 3

1.4 Average Return. 6

1.5 Expected Return. 8

1.6 Efficient Portfolio. 16

1.7 Minimum Variance Portfolio. 17

1.8 Market Portfolio. 18

1.9 Portfolio Optimization. 19

1.10 Summary and Conclusions. 20

1.1 Introduction

Consumers balance their current needs and wants of consumption – spending on food, housing, and other expenses – with their desires for future consumption, such as educational expenses, vacations, or buying a long-desired sports car at age 65. People save from their current income to invest in assets that will grow over time so that they can consume more in the future. The purpose of this book is to show readers how use SAS to enhance their wealth.

The total US household net wealth has grown from net wealth of $87 trillion at the end of 2016 to $100 trillion, as reported by the US government (Board of Governors of the Federal Reserve System (2018)), see Torry (2018). The stock market’s 20-plus percent return in 2017 is a significant contribution to this jump of wealth. Out of the $100 trillion, $28 trillion are earmarked as retirement assets, which have various tax-favored treatments. The Census report shows that at least 75 percent of households had at least $50,000 in net assets at the end of 2011. Those assets in a household’s portfolio might consist of cash, bond, stocks, real estate and so on. These different assets provide different return and risk characteristics. The Federal Reserve reported that the median financial asset value is $200,000 for people 40 years older.

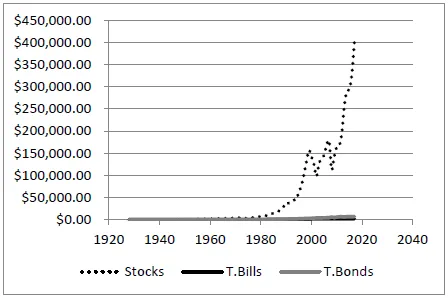

Everybody is a financial asset investor, either passively or actively. If you are the owner of a house, you are an investor in real-estate. It is often stated that your real estate investment is the largest investment a family will make. A recent examination of the Case-Shiller Housing Index reveals that the US housing market has reached an all-time high, as measured from 1970. If you have 401k accounts, you are likely a passive investor. If you have a brokerage account and trade a lot, you are active investor. Even the pension amount that you receive at retirement depends on the market performance. Figure 1.1 provides the cumulative wealth of an investor who invested $100 at beginning of 1928 in either cash, bond, or US stock market.

Figure 1.1: Cumulative Wealth of $100 Starting in 1928

As Figure 1.1 shows, stocks have outperformed bonds, and bonds have outperformed cash. One hundred US dollars at the beginni...