So what’s the real deal about real estate? What makes it such a hot topic and critical investment for everyone from the government honchos who manage the Canada Pension Plan down to the tech nerd from school who’s making oodles of money as a programmer? In this section, we check out the advantages of real estate and compare property relative to other kinds of investments you may consider as part of your portfolio.

Discovering the opportunities

Statistics from the Canadian Real Estate Association indicate that residential real estate has increased in value by an average of more than 5 percent a year over the past 30 years. Even though there have been some significant dips during that period, and not every property will make the same gains in every year or from city to city, the trend is unmistakable: The long-term potential for your real estate investment to appreciate is significant. Several reasons support our argument that an investment in real estate makes sense. We outline them here.

Leverage opportunities

Leverage is all about using a small amount of your own money and letting someone else’s cash do the rest of the work. Because real estate provides the loan’s security, a guarantee of repayment if you’re unable to pay off the loan, the risk is low. If you run into financial trouble and your creditors, the people who’ve loaned you cash, demand immediate repayment and call your loan, your property could be subject to proceedings that lead to its sale. Providing the property sells for more than the amount owing, you stand to emerge relatively unscathed. The nature of a forced sale of your property depends on the province and the mortgage documents you have signed. For example, in Ontario, the power-of-sale process doesn’t require court approval, whereas in some other provinces, the foreclosure and sale process requires the court to be involved throughout.

We discuss some of the basics of setting your limits as an investor so you can avoid the sale of your properties due to default of payment, in the section “Figuring Out if You’re Right for Real Estate Investing,” later in this chapter, and discuss financing at greater length in Chapter 6.

Equity opportunities

By paying down a mortgage, you’re paying the purchase value of the property and making its value your own over several years. Real estate is therefore unlike many other investments because it gives you a chance to build equity — your share of the property’s net worth at the time of sale — over the course of the investment rather than invest everything up front and hope for the best. Because the value of a property will change while you’re paying down the original value, you have two ways to build wealth, not just one.

Beware of negative equity! Although real estate is a convenient way to build equity (and that’s a good thing), a drop in the market can bring destruction and result in

negative equity, a situation in which the market value of a property is less than the mortgage it secures. This typically happens when an investment is financed with too much debt, a condition known as being overleveraged. This was a common scenario in the United States during the subprime mortgage crisis of 2006 when interest rates on some high-risk mortgages saddled buyers with payments they couldn’t afford. The financial crisis of 2008 brought further trouble, when some lenders called loans on borrowers suddenly considered to be poor risks.

To some investors, negative cash flow is a bigger concern than negative equity because negative cash flow leaves them short of cash to cover immediate expenses. However, negative equity is an unrealized loss that could turn into positive equity when the market improves. The key to successful investing in both cases is avoiding overleveraging, which means having more debt than you can handle. It implies excessive risk-taking, which most investors consider an imprudent investment strategy.

Return opportunities

When investors talk about returns, they’re talking about the money they’ll see – not the option to return their property for a refund! You’re quite right to ask for your money back when you invest in real estate, but the smart investor will get to keep the property, too. In fact, our calculations estimate that it’s not impossible to enjoy a net return of more than 75 percent annually on your investment. How do we figure that? Here’s the math.

If you buy a $300,000 property with a $30,000 down payment and the property increases in value by half over five years, the increase in equity is $150,000. That amounts to approximately $112,500 after the government taxes the appreciation in the property’s value, or capital gain (we discuss capital gains at greater length in Chapter 15). This would represent a return of 375 percent over five years, or at least 75 percent annually on your original investment of $30,000. Assuming the debt you incurred to buy the property decreased over the course of the five years, and the property generated rental income, you would enjoy an even greater return on your investment.

Tax opportunities

Real estate offers several tax advantages for you as an investor, especially if you’ve developed an investment strategy that accounts for taxes. Taxes erode the return you’ll see on investments yielding a fixed return, such as bank accounts, bonds, and guaranteed investment certificates (GICs), but not Tax-Free Savings Accounts (TFSAs). Stocks and other equities put your principal at risk. Real estate investments, however, frequently enjoy a reduced tax rate. Between tax-free capital gains on your principal residence to savings of up to 50 percent on taxes levied on capital gains from investment properties, there are many tax advantages to investing in real estate. You’re also able to deduct investment expenses and write off any depreciation in property values on your real estate purchases. We discuss taxes in greater detail in Chapter 15.

Hedge opportunities

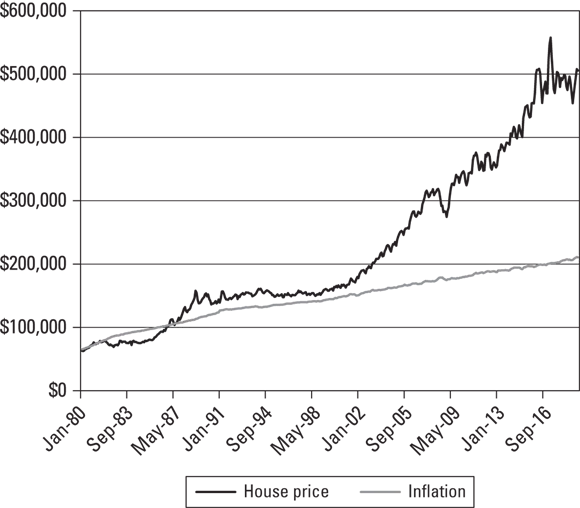

No, we’re not suggesting you hide from your creditors in a bush! The kind of hedging we’re talking about means taking shelter from the effects of inflation, which works to erode your buying power. The rate of inflation varies from month to month, year to year, and even country to country. But real estate typically appreciates at a rate 3 to 5 percentage points above the inflation rate. So if inflation is running at 3 percent, look for your investment in real estate to appreciate at 6 to 8 percent. If you choose wisely, your investment stands a good chance of increasing at a rate greater than that of inflation, as Figure 1-1 shows.

You’re paying off your mortgage in dollars that reflect inflation, also known as

real dollars. So, although the value of your mortgage will diminish over time, you’ll typically enjoy a higher income thanks to salary increases or rental revenue increases that will help make your mortgage more affordable to carry over the long term.

Flexibility opportunities

Real estate offers a variety of investment...